Oxford Industries Stock: Added To Our Buy List (NYSE:OXM)

JP Yim/Getty Images Entertainment

Oxford Industries (NYSE:OXM) is a name we have followed for some time. Looking back over the last few years, the one reason we have not become owners is because the stock has performed, on a relative basis, better than peers when we deployed money – essentially the pullbacks in peers have been greater than Oxford during times we were deploying capital. Just because we have not owned the stock during this time does not mean that we have not been fans of the business and brands. The truth of the matter is that we are fans of both and believe that the company’s management team is doing a good job of building out a stable of brands that could someday have 1-2 brands generating $1 billion+ dollars in revenue and 2-3 brands that generate around $500 million each.

That is further down the road, but the company’s most recent quarterly results, which included the 4th quarter and full year, disappointed the market. The operating results we thought were quite strong in Q4 (and for the FY2022), and the guidance going forward seemed decent considering the economic backdrop and macro challenges many companies are discussing as headwinds in 2023. It seems that the market was spooked by the fact that the company has labeled 2023 a year of investment and will be spending heavily to bolster their DTC offerings, IT infrastructure and fulfillment capabilities while also investing in their teams to bolster capabilities within the entity. The company will also continue to open new retail stores and should see three new Tommy Bahama Marlin Bar restaurants open.

The Dividend

So first, let’s talk about the good news. The company announced that they would be increasing the dividend by just over 18%; with the new quarterly rate up to $0.65/share from the previous $0.55/share rate. While the yield is now nearly 2.60%, we do think that this Board and management team will look to continue raising the dividend in years to come as there is a strong track record of not only paying a consistent dividend but also returning capital to shareholders (via dividends and share buybacks).

With all of the talk about further investment being required for 2023, we think the company will focus on those initiatives while also deleveraging the balance sheet and building cash back up during this year. However, we would not be surprised to see the company purchase additional shares under the older share repurchase program in 2023’s Q4 or in 2024 if growth remains and the economy does not cool too much. There is $50 million still available under that program.

Oxford Industries still has a $50 million share repurchase plan in place. (Oxford Industries Form 8-K)

Inventory Levels

Management discussed the rising inventory levels on the conference call and explained that a portion of the increase can be explained by two main drivers. First, the company purchased Johnny Was which saw $20 million in inventory get booked with the acquisition. Also, there was $25 million in inventory increases due to the early receipt of inventory for Johnny Was. So about half of the inventory increase can be explained due to the acquisition.

Management also feels comfortable with the other half of the increase in inventory because the quality of the inventory is good in their eyes due to it being core inventory and not fashion-specific inventory. Scott Grassmyer, Oxford’s CFO and COO, stated on the conference call that, “we feel good about our inventory, the composition of it and the levels and we think we’re set up well to capture demand in ’23.”

The Business Moving Forward

We look at Oxford Industries as an incubator of brands. While the Tommy Bahama brand currently makes up the majority of the business, we believe that the other brands that the company owns can deliver outsized growth in the years ahead. Lilly Pulitzer has a niche that extends very well into Oxford’s “lifestyle brand” initiative, and we believe that there are a few brand extensions that could drive growth and enhance the consumer experience. One of those extensions is already being acted upon – enhanced home product (think hostess gifts, etc.).

Within the Emerging Brands operating group, we think that Southern Tide and Duck Head offer compelling growth stories and should start to drive strong organic growth now that Oxford has defined strategies for both. With The Beaufort Bonnet Company also getting attention via physical stores, Oxford now has two of their brands from the Emerging Brands segment now offering physical locations and customer experiences and interaction.

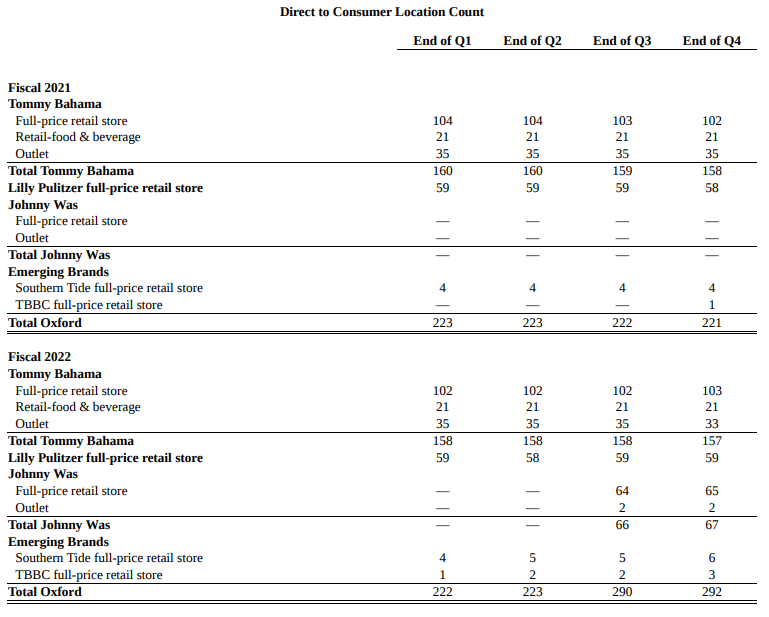

In FY 2022, Southern Tide saw its physical store count increase 50%, from 4 stores to 6 stores. The Beaufort Bonnet Company opened its first store in Q4 2021 and then opened another 2 locations in 2022.

Breakdown of Oxford Industries’ company-owned stores by brand over 2021 and 2022. (Oxford Industries Form 8-K)

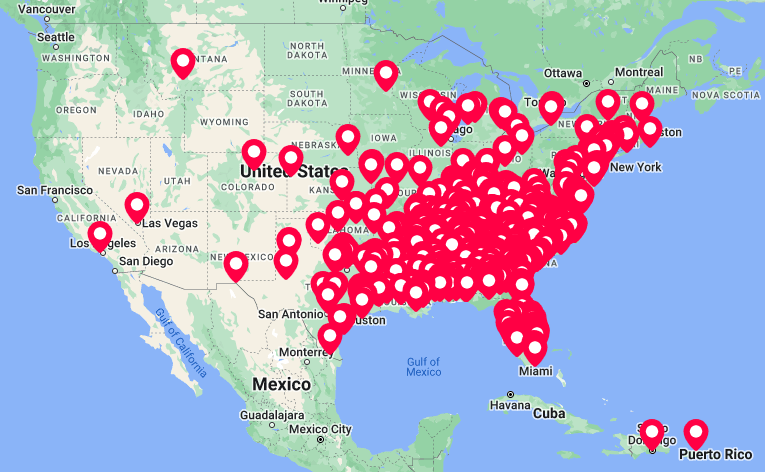

We suspect that Oxford could have one hundred locations for the Southern Tide brand over the next decade by simply focusing on cities with large colleges and cities with decent tourism. The Beaufort Bonnet Company (or TBBC) could easily support 25 stores across the Southeast in the next five years, but much of this growth would depend on Oxford’s willingness to compete against boutiques that currently sell TBBC (and other Oxford brands).

Many of the boutiques that offer The Beaufort Bonnet Company’s apparel are in the Southeast, but that should not impede Oxford in opening company-owned stores. (thebeaufortbonnetcompany.com)

While there is plenty of room to fill in the map in the Southeast by opening company-owned stores, Oxford might have to manage growth in order to avoid angering boutiques that currently sell TBBC’s clothing, which are shown on the map above. There are definitely some opportunities in large cities in the Southeast, namely Charlotte and Atlanta, as well as some cities as you get into the Mid-Atlantic and Midwest, such as Indianapolis and Charlottesville, VA. Some of those areas are outside of the target market, but are compelling markets based off of their size and demographics.

Final Thoughts

We like the story here and the opportunity for growth through multiple brands and multiple channels. With the recent pullback in shares we are adding Oxford Industries back to our buy-list and will look to purchase shares under $100/share. Yes, based off of the projected P/E and the yield, this is an attractive entry point, but we want to hedge potential economic headwinds by getting an entry point a little lower than current levels.

With the DTC channels already established and the company beginning to curate stores for the Emerging Brands segment, we think that the next 5-10 years could see Oxford Industries’ shares rise sharply as revenues grow and the company is able to increase dividends and share buybacks with additional cash flows and profits.