Zoom Stock Undervalued; Solid Enterprise Platform Growth (NASDAQ:ZM)

Sergeeva

Zoom (NASDAQ:ZM) is a technology titan which has created one of the world’s most popular video conferencing platforms, with over 13 million monthly active users. Video conferencing was first showcased back in 1968 and commercially developed in 1982. The technology has been around for decades, but shoddy internet connections and the cultural mindset meant it was rarely adopted. However, 2020 was a perfect storm for video conferencing platforms, and Zoom exploded in popularity, as employees were informed to work from home. Zoom was a classic “lockdown stock” and its brand name became synonymous with video calls. However, since mid-2021 its revenue growth rate has slowed down substantially, as fierce competition from the likes of Google Meet and Microsoft Teams, aggressively took market share. A positive for Zoom is management, has been proactive and started to execute its “platform” strategy approach and gained significant traction with enterprises. In this post, I’m going to break down its business model, financials, and valuation, let’s dive in.

Business Model Evolution

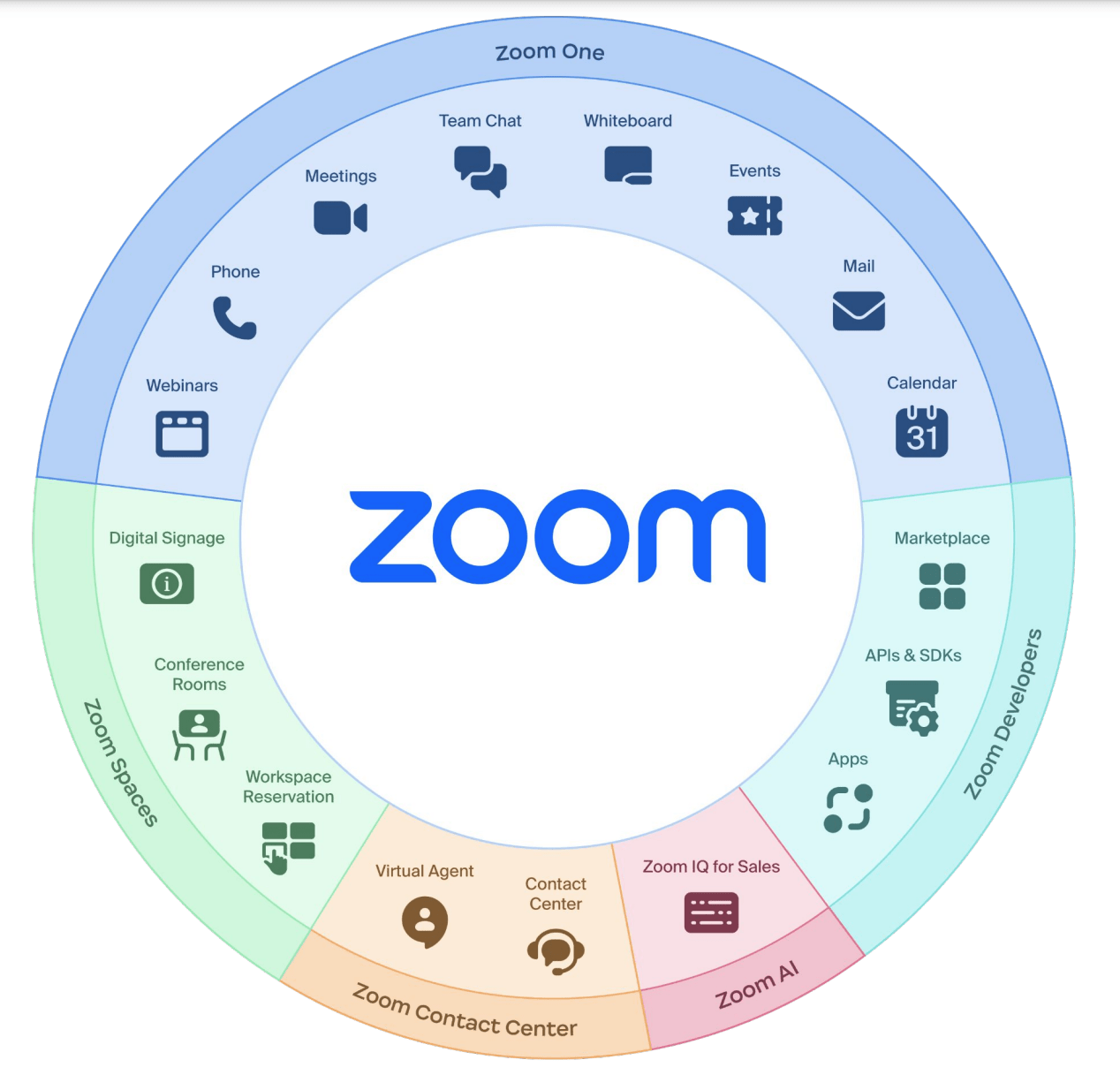

As mentioned prior Zoom has scaled its video conferencing product to create more of a platform. Its “Zoom One” platform now includes webinars, events, team chat, an online whiteboard etc. Its “Spaces” competes with Microsoft Team Rooms, with the sale of hardware to kit out conference rooms with a variety of displays, microphones, and systems for meetings.

Zoom One Platform (Q3,FY23)

Zoom also offers a cloud contact center platform, which enables the replacement of a traditional call center with a more flexible, cost-effective solution. In addition, the company offers an AI tool, called Zoom IQ for Sales. This tool uses “Conversational AI“, to analyze sales calls for “filler words”, “talk to listen” ratio, and much more. The tool can also offer automated chat responses and transcriptions, similar to that found in the popular viral platform ChatGPT. Similar to Salesforce, Zoom has created a development environment where bespoke applications and Apps can be built on top. This is great as it effectively means the company has an army of developers innovating on the product, but not on the company payroll. This series of Innovations means Zoom is Gartner magic quadrant leader in “Unified Communications”. The expansion of its product solution gives Zoom a great number of cross-selling opportunities. For example, with its vast number of existing customers who have signed up for the video conferences service, Zoom can upsell a virtual events package and even its contact center solution. In enterprise strategy, this approach is called “land and expand” and is a strategy Zoom has adopted.

Zoom Products (Zoom Website)

Mixed Financials

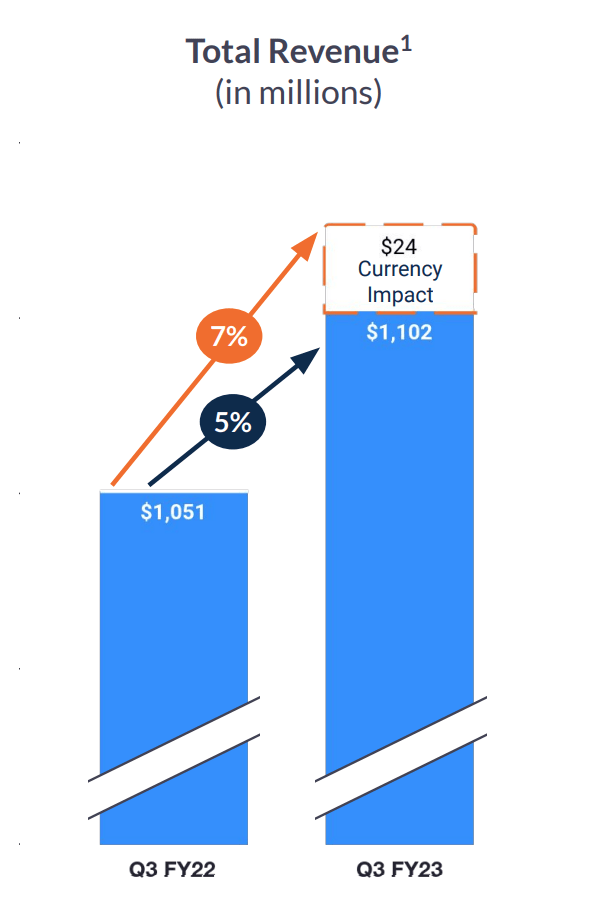

Zoom reported mixed financial results for the third quarter of fiscal year 2023. Revenue was $1.1 billion, which increased by 5% year over year and missed analyst estimates by $359.24k. The revenue miss, looks to have been mainly driven by a $24 million currency impact, related to a strong U.S dollar, which impacted international revenue. On a constant currency basis, revenue growth was slightly faster at 7% year over year. This is a much slower growth rate than prior years. For example, Zoom achieved a 35.2% growth rate in the comparable quarter last year. Prior to this, Zoom grew its revenue at above 50%, with 53.95% YoY growth in Q2,FY22. In 2020, during the lockdown the company had outstanding growth of 325.81% year over year. Now, of course I am not expecting 2020 growth rates, but I believe ~20% growth rate should be reasonable for a “growth” company. Whereas the current growth rate is more aligned with a mature incumbent, I suspect this is due to large market penetration, coupled with intense competition, which I will discuss in the “Risks” section.

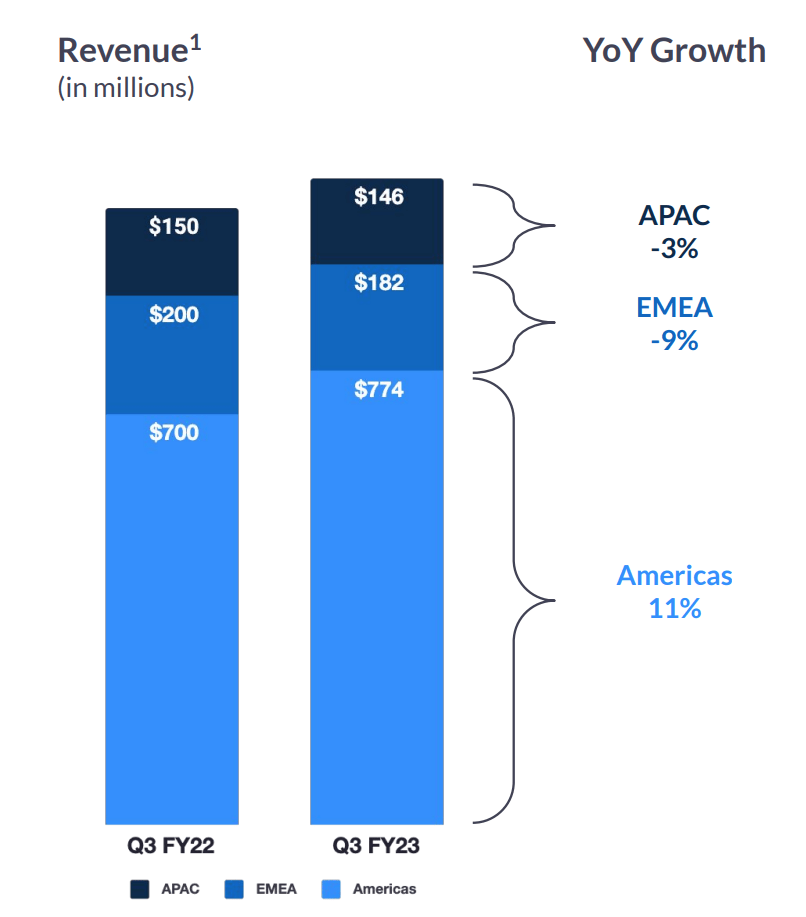

Revenue (Q3,FY23 report)

Breaking the revenue down by region, Zoom’s largest segment the Americas reported the strongest growth, as it increased revenue by 11% year over year, which was positive. However, the EMEA region reported a substantial decline of 9% year over year, followed by APAC at 3% year over year. Again, I believe foreign currency impact played a huge part in the negative growth.

Revenue by Region (Q3,FY23 report)

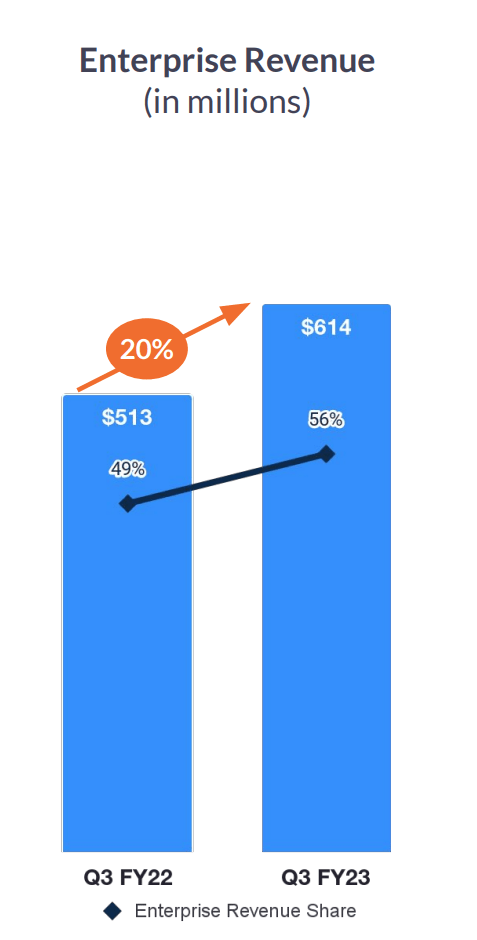

A positive for Zoom, is it has continued to “grow upmarket” and expand into enterprises. Its number of enterprise customers reached a staggering 209,300, which increased by 14% year over year. This drove strong enterprise revenue $614 million, which increased by 20% year over year.

Enterprise revenue (Q3,FY23 report)

As of the third quarter FY23, Enterprises contribute 56% of total revenue which is a positive sign. These large businesses tend to have much higher upsell opportunities and a greater retention profile. In this case, Zoom’s online churn has declined from 3.7% in Q3, FY22 to 3.1% by Q3, FY23. Whiles its enterprise Net dollar retention rate was a healthy 117% in Q3,FY23, which means its customers are staying with the platform and spending more.

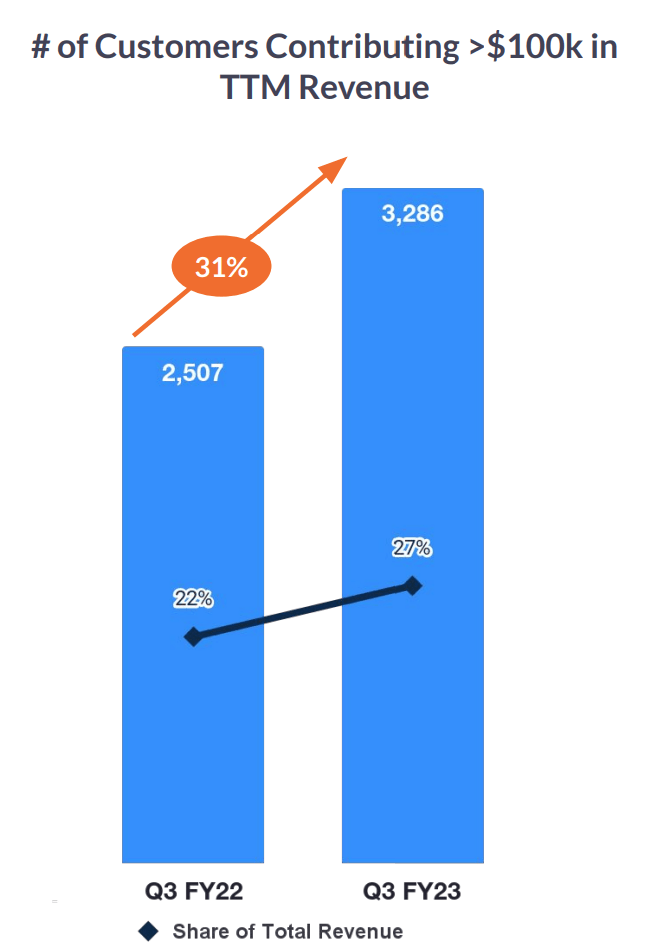

Zoom’s largest customers which contribute over $100,000 in trailing 12 month revenue, has also increased by a rapid 31% to 3,286, which is positive.

Large customers (Q3,Fy23)

Profitability and Expenses

On a “Non-GAAP” basis Zoom reported a gross margin of 79.5% in Q3, which improved over the 76% in the prior year. This improvement was driven by optimization across its cloud and data centers, which helps to improve infrastructure usage patterns.

On a GAAP basis, Zoom has struggled with its operating profitability since the start of 2022, its operating margin has been squeezed. In the first quarter of the calendar year 2022, its Operating margin was a healthy 23.5%, which is the average of the software industry. However, by the third quarter of 2022 this had plummeted to just 6.04%.

This was mainly driven by an increase in expenses across the board. Its R&D expenses increased by 59% year over year to $108 million. This was driven by aggressive investments in expanding the company’s product portfolio. Therefore I believe these were necessary expenses, and I think R&D investments are generally valuable, assuming ROI is obtained long-term.

Sales and Marketing expenses also increased by a rapid 27% year over year to $301 million. This is as the company aggressively invests in its channel partner expansion model. Its General & Administrative expenses increased by 6% year over year to $87 million.

A positive is on a “Non GAAP” basis earnings per share was $1.07 in the third quarter of FY23, which was $0.23 higher than management estimates.

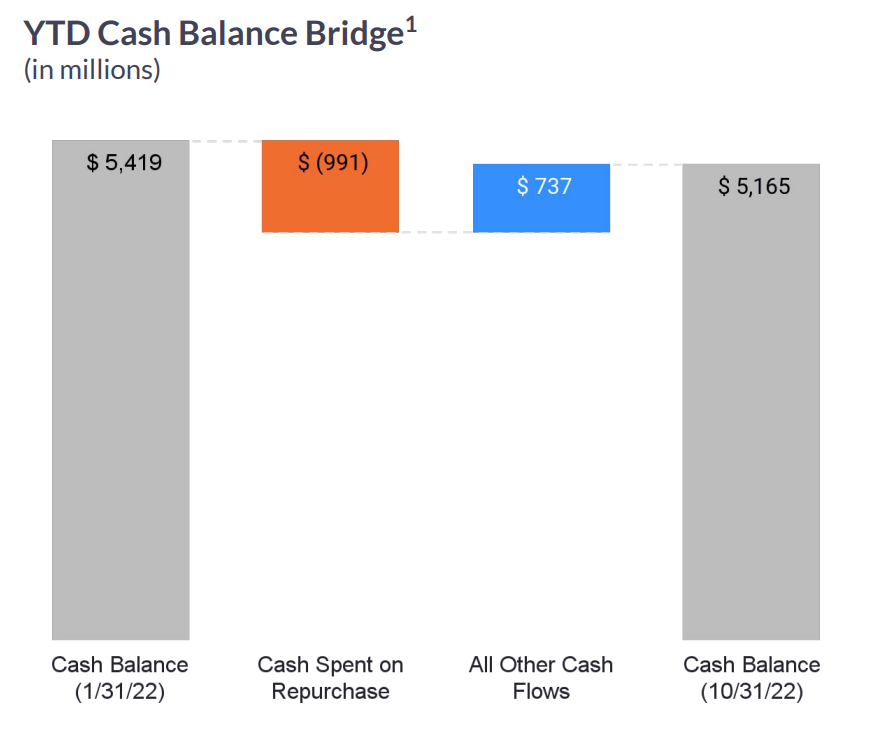

The company has a fortress balance sheet with $5.2 billion in cash, cash equivalents, and short term investments. In addition to just $99.9 million in total debt. In Q3, FY23, the company bought back 11 million shares, with an estimated value of $991 million.

Balance Sheet (Q3,FY23)

For the full year of FY 2023, management is guiding for revenue between $4.37 billion to $4.38 billion, which would represent growth of 7% year-over-year growth or 8.5% on an FX-neutral basis. This is $15 million lower than prior guidance, which is mainly driven by continual FX-neutral pressure.

Management’s strategy of enterprise growth is a solid strategy given the aforementioned reasons such as retention and upsell opportunities. Many other software companies such as CrowdStrike (CRWD), have followed a similar strategy. This has generated strong growth despite being in a very different industry. Management is guiding for its enterprise segment to grow in the low to mid-20s in the year, but its “Online business” is forecasting a decline of 8% for the year. The company also aims to continually expand its partner ecosystem, which is a solid strategy given the recessionary environment. As paid advertisements are generally less cost-effective during depressed market conditions.

Advanced Valuation

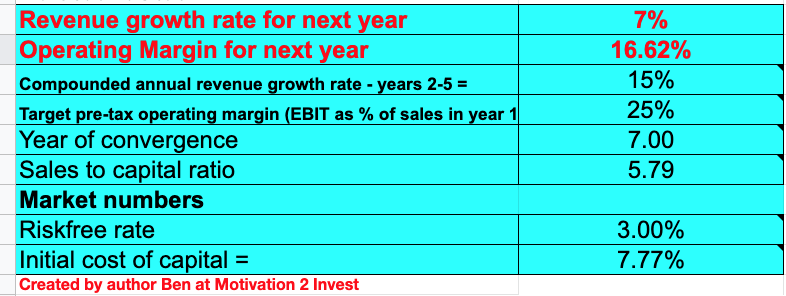

In order to value Zoom, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow method of valuation. I have forecasted 7% revenue growth for next year, which is conservative and aligned with 2022 figures. However, in years 2 to 5, I have forecasted its revenue to increase by a better 15% per year. I expect this to be driven by the continued adoption of its unified platform for enterprises.

Zoom stock valuation 1 (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation, I have capitalized R&D expenses which has lifted net income. In addition, I have forecasted its operating margin to grow to 25%, by year 7 which would be a return to levels seen pre-2022. I expect this to be driven by a return on its product investments and upsells to its products such as “Events” and the cloud contact center platform.

Zoom stock valuation 2 (Created by author at Motivation 2 invest)

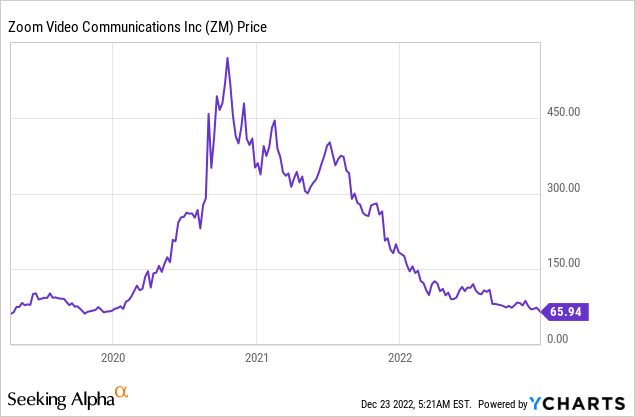

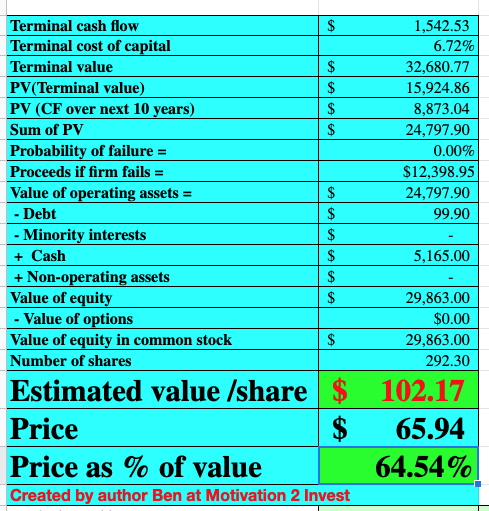

Given these factors, I get a fair value of $102.17 per share. The stock is trading at ~$65/share at the time of writing and thus is ~46% undervalued.

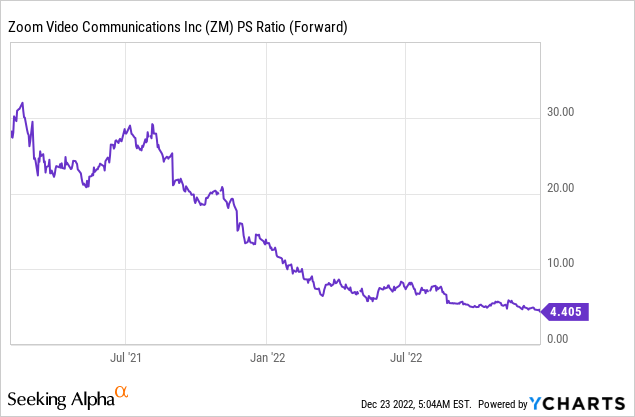

As an extra datapoint, Zoom trades at a price-to-sales ratio = 4.5, which is 86.4% cheaper than its 5-year average.

Risks

Competition

Zoom has a massive amount of competition on all fronts. From Microsoft Teams, which is deeply embedded into many enterprises to Google Meet, which offers a free package. Reliable video conferencing has become a commodity which is bad news for the return on capital for companies in the industry. The good news is Zoom has diversified into a more “unified” platform which now competes with companies such as 8×8 (EGHT) and Five9 (FIVN). This is a solid strategic move and offers huge cross-selling potential.

Final Thoughts

Zoom has continued to innovate its solution and now offers a range of products across multiple areas. The company has a much larger addressable market currently, but so far this hasn’t translated into higher growth rates. The good news is its stock is undervalued intrinsically and relative to historic multiples and the company has a growing enterprise customer base. Therefore thus this could be a great long-term investment, especially as economic conditions improve.