Zoom: Emulating Microsoft’s Offerings – Still Not A Buy Here (NASDAQ:ZM)

ibreakstock/iStock via Getty Images

Investment Thesis

Zoom Video Communications, Inc. (NASDAQ:ZM) has been working hard to shed its pandemic teleconference image. We think this is attributed to the aggressive Selling General/ Admin expenses of $1.95B (+31.7% sequentially) and Research/ Development expenses of $629.8M (+211.1% sequentially) over the last twelve months [LTM].

Therefore, it is unsurprising that ZM has also released over 1.5K product enhancements at the same time, illustrating its ambition to be an all-in-one communication platform through Zoom One. This includes expanding meeting resources to enhance its core offerings, on top of launching additional capabilities such as Chat, Mail, Calendar, and an Application Marketplace with a revenue share model, akin to Alphabet’s (GOOG) (GOOGL) Google Play.

These recent developments are interesting indeed. ZM seems keen on emulating Microsoft’s (MSFT) core enterprise model, with the latter also offering a 365 Office and a cloud segment, Azure, amongst others. Moreover, seeing ChatGPT’s success thus far, we may also see the former achieve expanded consumer onboarding through its AI-Powered Chatbot for the Zoom Virtual Agent for the online call-center and Zoom IQ Virtual Coach for the sales end-market.

The Expansion Of ZM’s Total Addressable Market

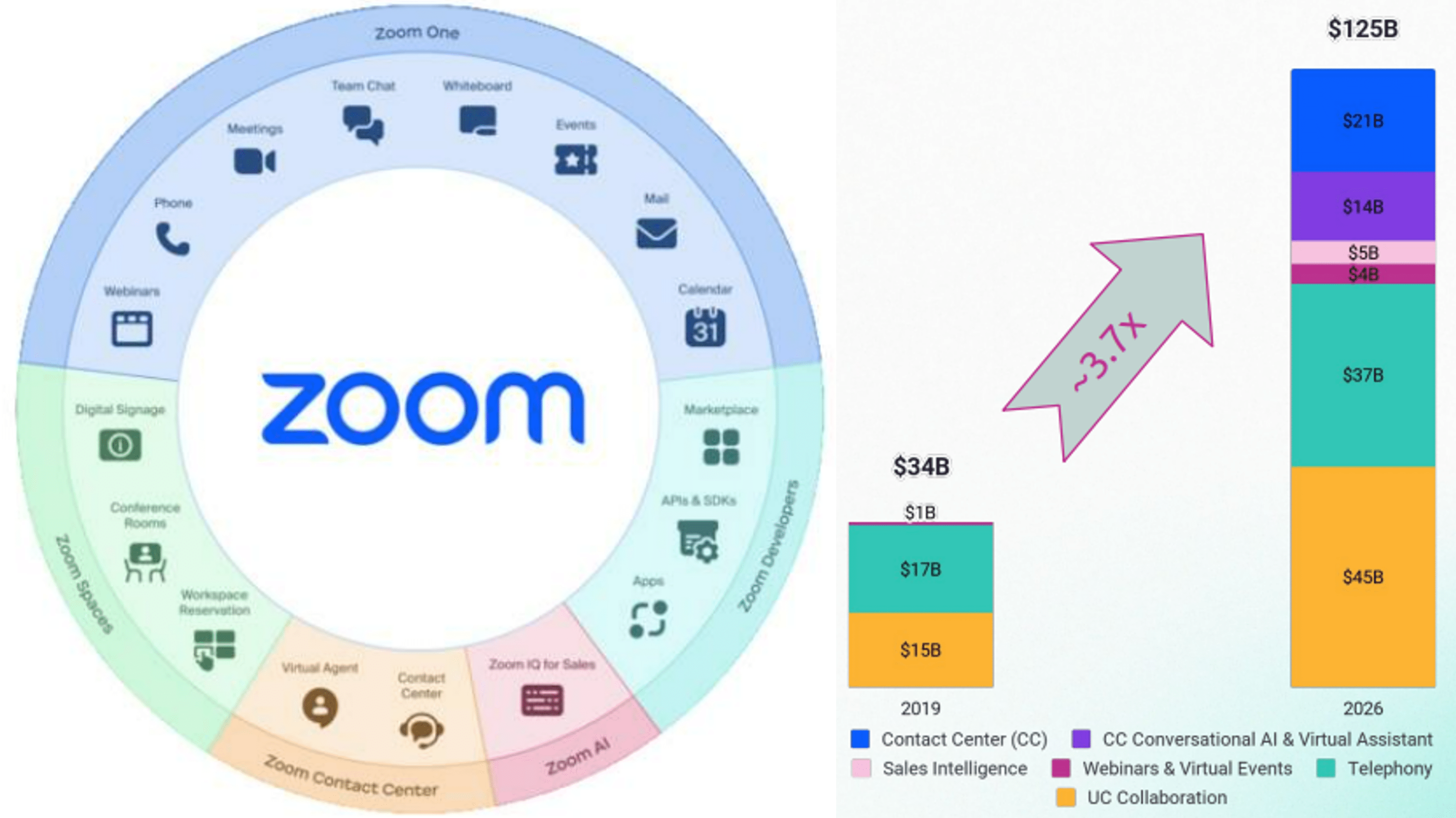

Zoom

Now, why does this matter? ZM expects these efforts to eventually be top and bottom-line accretive due to the 367.6% expansion in its Total Addressable Market from $34B in 2019 to $125B by 2026. As of October 2022, ZM commanded a leading market share of 55.54% in the global videoconferencing softwares, reporting an excellent market penetration of 65% during the post-reopening-cadence.

At the same time, through these vertical integrations, ZM increased its consumer onboarding across different offerings, with approximately 10% of its enterprise consumers using 3 or more products thus far. Notably, this group also grew by 45% YoY, while similarly generating up to 50% of the company’s Annual Recurring Revenue by the latest quarter. These numbers are impressive indeed.

This could be why ZM’s enterprise customers have also grown to 54% of its revenues by FQ3’23, compared to 42% in FQ2’21, with more signing up for annual contracts at 70% against 49% at the same time. Notably, its average contract lengths have also expanded to 15 months by the latest quarter, against 11 months in FQ2’21, potentially attributed to increased consumer stickiness and net dollar expansions across different offerings.

Therefore, while ZM’s top-line growth may be decelerating, attributed to the normalization of hyper-pandemic levels, its enterprise demand seems to have remained healthy thus far. This is especially made sweeter by the management’s strategic choice to innovatively expand its product offerings at a time when remote work is increasingly embraced globally.

Assuming continued onboarding success moving forward, we think we may see ZM stock recover moderately, once the market sentiments lift and macroeconomics improve, likely by the end of 2023 in our view. However, we remain skeptical of Cathie Wood’s call for the stock’s appreciation to $1.5K by 2026, since it suggests an overly ambitious twelve-fold growth in its EPS based on P/E valuations of 30x.

So, Is ZM Stock A Buy After A -55.39% Decline In The Past Year?

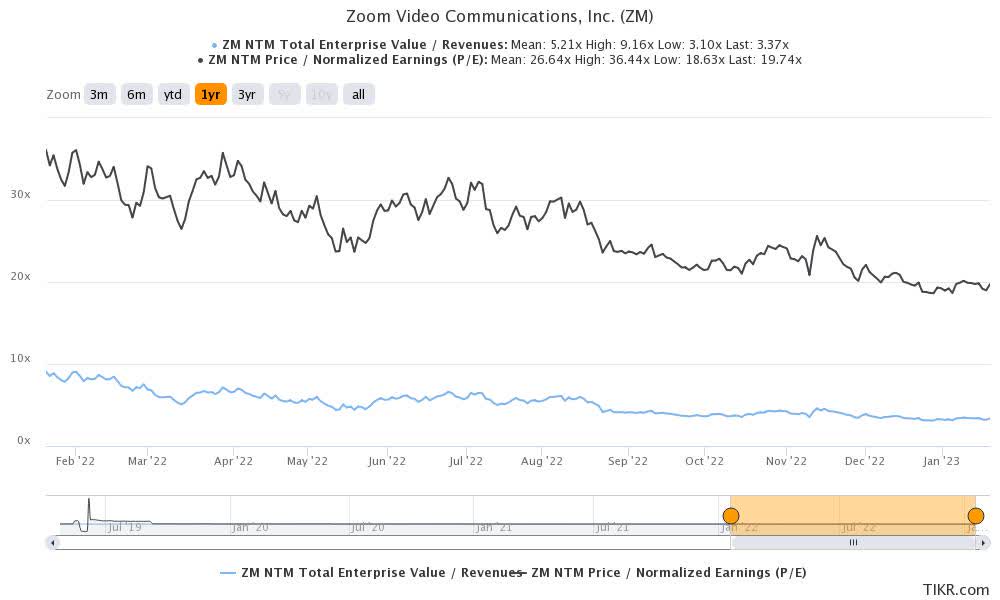

ZM 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

ZM is currently trading at an EV/NTM Revenue of 3.37x and NTM P/E of 19.74x, lower than its 3Y mean of 21.96x and 111.49x, respectively. Otherwise, it is still lower than its 1Y mean of 5.21x and 26.64x, respectively.

It is apparent that market analysts remain bullish about ZM’s prospects, attributed to their price target of $86.67, suggesting a 24.71% upside potential from current levels.

ZM 1Y Trading Levels

S&P Capital IQ

However, we prefer to err on the side of caution, since the Feds are still due to hike interest rates through 2023, with a pivot only likely from 2024 onwards. The pessimistic sentiments are also unlikely to lift in the short term, due to the peak recessionary fears.

This is exemplified by the ZM stock’s continuous slide over the past year. While the stock has bounced by 6.2% from the December bottom, it remains to be seen how things will play out over the next few months, with it trading nearer to its 52 weeks low at the same time.

As a result, we posit that ZM’s valuations may further retrace moderately, especially due to the deceleration of its enterprise growth thus far. By FQ3’23, the company reported a YoY expansion of 13.9% in the number of its Enterprise customers, compared to FQ2’23 levels of 17.9% and FQ1’23 levels of 24.1%.

Most importantly, the number of ZM’s customers contributing more than $100K in the LTM revenue has also decelerated to 31.2% YoY, against 37% and 46.2%, respectively. Its LTM net dollar expansion rate for enterprise customers experienced a similar decline at 117%, when compared to previous rates of 120% and 123%, respectively.

While ZM’s enterprise demand remains more than healthy, these numbers do not imply high growth, but the upcoming FQ4’23 earnings call should further reveal its most recent performance.

On the other hand, there are many positive aspects to ZM’s execution thus far. By the latest quarter, it reports practically zero debt with a stellar $5.16B of cash/investments on the balance sheet. With highly controlled Capex through strategic partnerships with public cloud vendors, the company should remain asset-light for the foreseeable future, suggesting expanded liquidity ahead.

While we are concerned about ZM’s elevated Stock-Based Compensation [SBC] of $929.07M over the LTM, its Free Cash Flow [FCF] generation remains excellent at $1.19B at the same time. Moreover, its share dilution has also notably moderated, attributed to the $990.77M of shares repurchased over the past three quarters. These suggest improved liquidity over the next few quarters of product innovation, despite the potential deceleration in enterprise demand.

Comparatively, MSFT reports a similarly elevated NTM P/E of 24.41x and SBC expenses of $7.99B over the LTM, despite the excellent FCF generation of $63.33B over this period. As the practice becomes increasingly common in the high-growth tech industry, we think investors should not be overly critical of SBC expenses for now. This is especially true since it is primarily attributed to the management’s efforts to attract talent and drive tech innovation.

Lastly, ZM still reports an excellent Remaining Performance Obligation [RPO] of $3.24B in the latest quarter, despite the slowing growth of 0.9% QoQ and 32.2% YoY, against FQ2’23 levels of 7.3%/37.1% and FQ1’23 levels of 13.2%/44.4%, respectively. With 59% of its RPO expected to be recognized as revenue over the next twelve months, its intermediate prospects remain somewhat decent.

Therefore, investors with higher risk tolerance and a long-term investing trajectory may consider nibbling on ZM shares at the low $60s for an improved margin of safety. Nonetheless, we prefer to continue rating the stock as a Hold for now, due to the potential volatility ahead. In the face of decelerating corporate spending, there may be more attractive entry points by mid-2023, since there appears to be no clear support level yet in our view.