Workday (WDAY) Stock: Buy While It’s Quietly Hitting Targets

Sakorn Sukkasemsakorn

Every long-term oriented investor should have their shopping lists ready right now: the best stocks to buy, in my view, are high-quality tech names that have seen significant reductions in share price despite minimal disruption to fundamental performance this year. Many sturdy brands in the software sector, in particular, are now trading at multi-year valuation lows that should be snapped up.

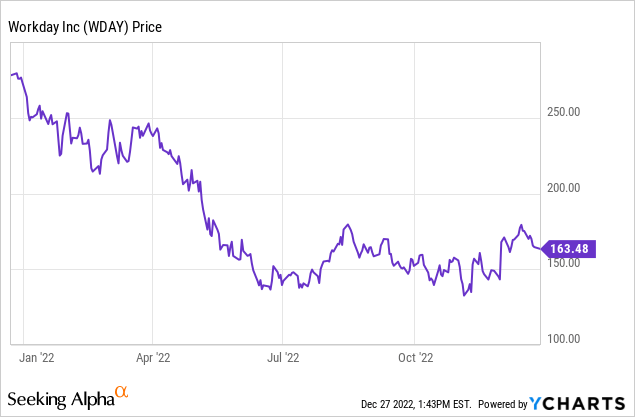

Workday (NASDAQ:WDAY), in particular, bears watching. The reigning cloud software leader in HCM and one of the most prominent names in financial software as well, Workday has shed about 40% of its market value this year despite steady financial results:

I remain solidly bullish on Workday and am more than comfortable holding this stock through 2023. Recent leadership shakeups (the company announced that its COO Carl Eschenbach to the co-CEO position, replacing outgoing co-CEO Chano Fernandez) should have minimal long-term impact to the company, especially as the company is replacing one sales-oriented leader with another. In addition, a renewed $500 million buyback program should help to instill new confidence in the stock.

Here, in my view, is the long-term bull case for Workday:

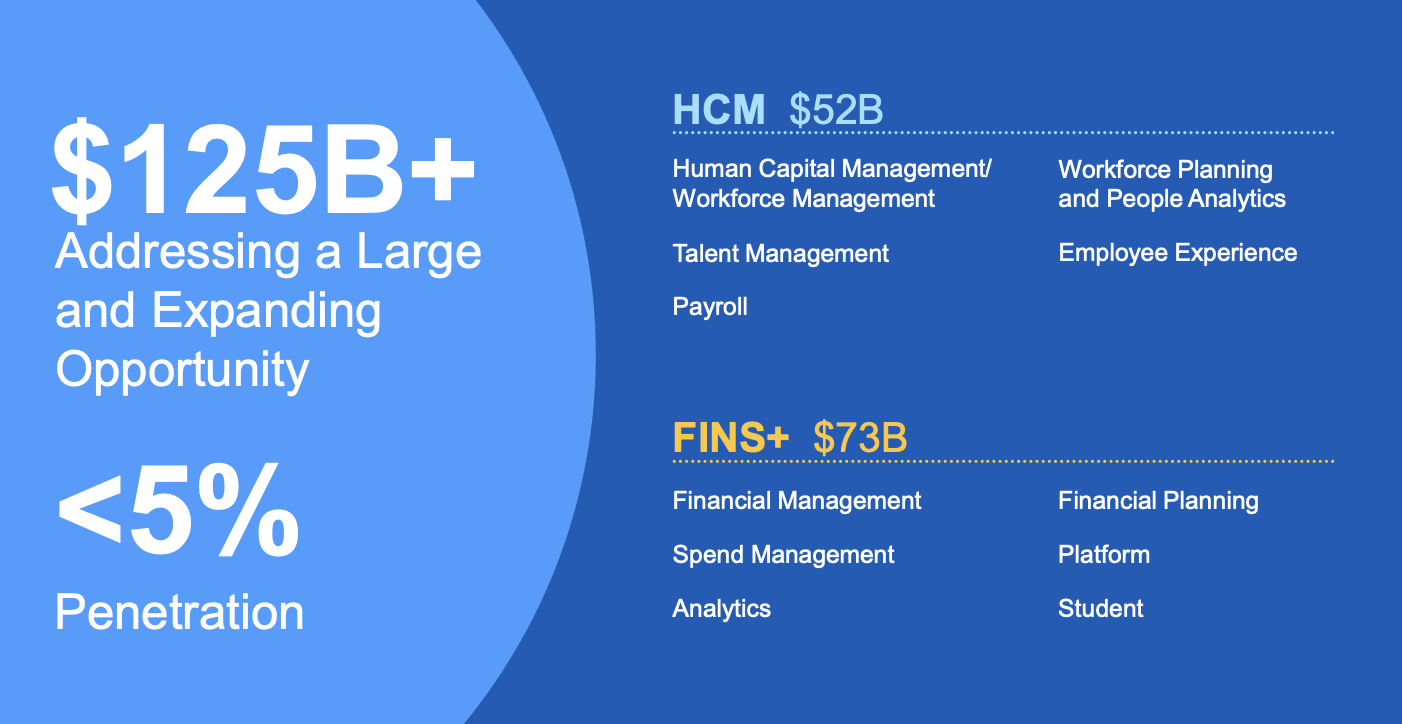

- Category leadership in two very large markets in enterprise software. For investors who don’t have the history, Workday was born out of ex-Oracle employees who eventually turned Workday into a premier cloud software solution for HR. The company has now extended that dominance into financial/ERP software, and together between these two markets Workday now sits on a massive $125+ billion market opportunity.

- Cloud-based, recurring revenue software. Workday has always been one of the “original” large-cap software companies, alongside Salesforce.com. Its revenue base is almost purely driving from subscriptions, giving Workday a powerful recurring revenue stream from which to grow.

- Ample resources and cash. Workday has more than $5 billion of cash on its balance sheet, giving it plenty of financial firepower to pursue both organic and inorganic growth.

- Growth/profitability balance. Workday is a “Rule of 40” software stock, which is a goal many fellow enterprise software companies strive to achieve and fail to do. With 20%+ revenue growth on top of 20%+ pro forma operating margins, Workday has achieved a level of growth/profitability balance that should give investors some comfort in a choppy stock market.

See below all the categories in which Workday software operates:

Workday TAM (Workday Q3 earnings deck)

Workday’s valuation also remains quite modest. At current share prices near $163, Workday trades at a market cap of $41.94 billion. After we net off the $5.49 billion of cash and $2.97 billion of debt on the company’s most recent balance sheet, Workday’s resulting enterprise value is $39.42 billion.

Meanwhile, for FY24 (the year for Workday ending in January 2024), Wall Street consensus pegs Workday’s revenue at $7.27 billion, representing 17% y/y growth. This puts Workday’s valuation at just 5.4x EV/FY24 revenue – which is still modest considering high teens/low 20s revenue growth amid consistent operating margin expansion.

The bottom line here: to me, there is quite a bit of runway for Workday to rebound in 2023. Take advantage of current low share prices to build up a position here.

Q3 download

Earnings beats, especially in the tech sector, have become much rarer in the second half of 2022. Workday’s results, released in the tail end of November, showcase a company that remains quite resilient in the face of sharp macro headwinds:

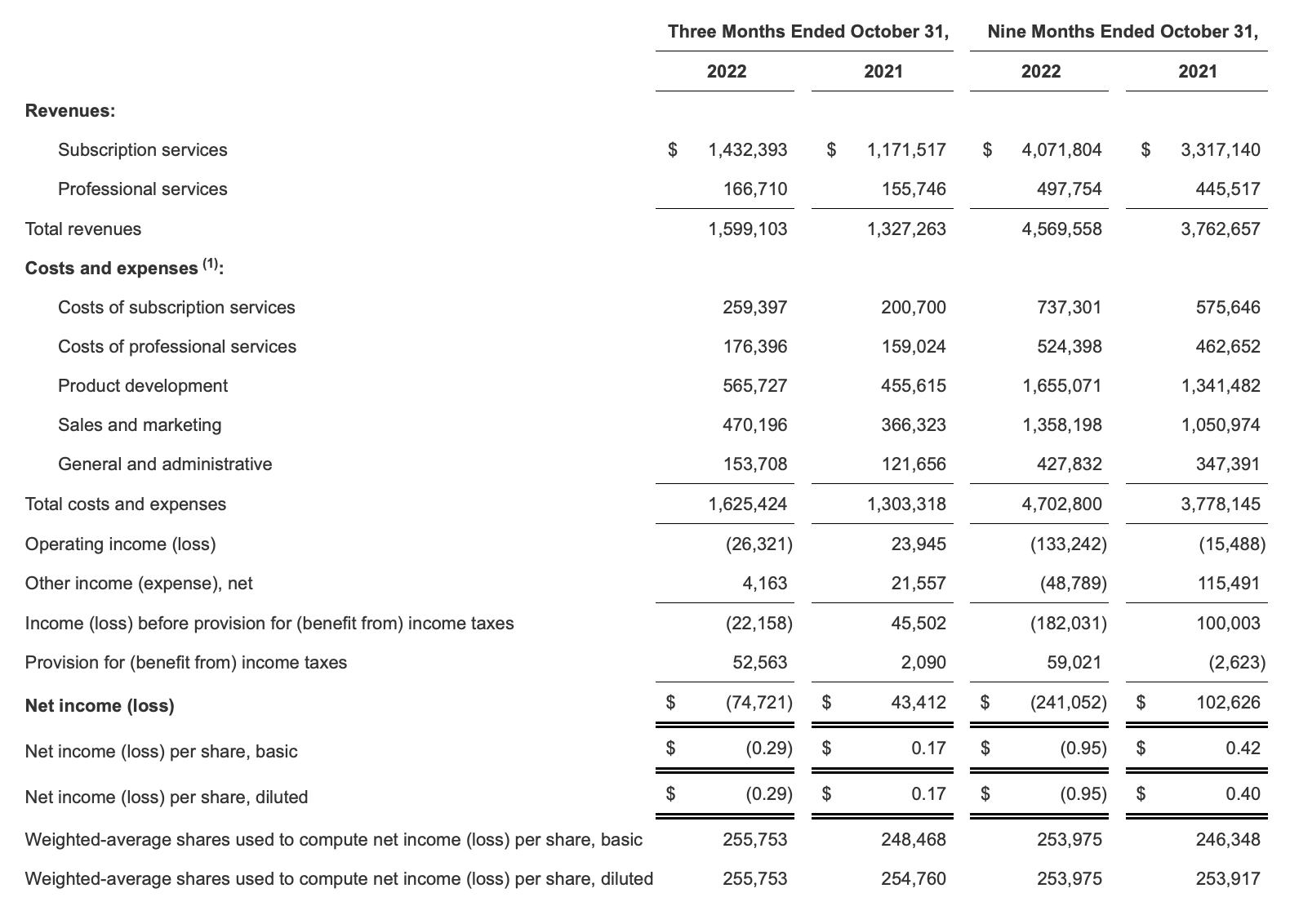

Workday Q3 results (Workday Q3 earnings release)

Workday’s revenue grew 20% y/y to $1.60 billion in the quarter, beating Wall Street’s expectations of $1.59 billion. The company’s growth kept pace with 21% y/y growth in Q2, despite steeper FX headwinds.

The company is starting to indicate that macro uncertainties and enterprises’ slowdown in spend is having the effect of prolonging deal cycles. That being said, through Q3 the company delivered strong renewals and upsells. Per outgoing co-CEO Chano Fernandez’s remarks on the Q3 earnings call:

Our customer base sales team once again saw outstanding growth, a direct reflection of the trust that customers are placing in us and a validation of our strategy. We drove very strong renewal rates in Q3, and we closed a number of strategic expansions at companies such as Accenture, University of Maryland, the state of Nebraska, Pick n Pay, Puma and VF Corporation […]

As we move into our fourth quarter, the environment remains uncertain, which has led to increased scrutiny and the lengthening of certain sales cycles, particularly with the net new opportunities. While we aren’t immune to these and see signs that it will persist into next year, we are confident in our diverse pipeline and are focused on executing in Q4 and laying a strong foundation for FY 2024 and beyond.”

The company also noted robust 24-month backlog of $8.62 billion, which grew 21% y/y, and net revenue retention rates “above 100%.” Total subscription backlog of $14.1 billion, meanwhile, grew 29% y/y.

Pro forma operating margins in Q3 clocked in at 20%, representing five points of margin contraction versus 25% in the year-ago Q3. This is primarily chalked up to recent hires, particularly in the go-to-market teams (which are essential to drive continued growth).

Workday’s CFO, however, noted that the company is planning to instill a “strong moderation of hiring as we move into Q4,” while noting that the company still plans on adding talent to its sales and technology development teams. The company also provided a prelim view of FY24 that expects pro forma operating margins to expand by 150-200bps.

Note as well that Workday’s pro forma EPS of $0.99 beat Wall Street’s expectations of $0.84 with 18% upside.

Key takeaways

Workday, in my view, remains a solid software company that is quietly continuing to grow to fill a massive $100+ billion TAM while also steadily improving its bottom line. Stay long here and use this opportunity to buy Workday at a discount.