Week On Wall Street – A Banking Event Changes The Scene (NYSEARCA:SPY)

RomoloTavani/iStock via Getty Images

“Bank failures are caused by depositors who don’t deposit enough money to cover losses due to mismanagement.” – Dan Quayle.

Narrative shift, after narrative shift – that is the road ahead. When we start to look back we realize inflation wasn’t transitory, it’s not going to drop off a cliff and be at 2% by the middle of 2023, and the Fed funds rate won’t peak at 3.5%-4%.

What investors are living with today is “stickier” inflation that remains at elevated levels. The Fed funds rate is now at 4.5%-5% and expectations go as high as 6%. That is the reality that investors have to deal with today, and there could be another change to the “narrative” on the way.

The underlying economy is currently bifurcated. Depending on who you want to listen to, it’s either very strong and resilient OR very weak and about to get weaker. The arguments that support a strong economy are buoyed to the employment scene. The economists that make the case for weakness in the economy are looking at every other economic data point that is forecasting a recession. So that makes it difficult to gauge what this economy means for corporate earnings going forward.

Big tech is cutting thousands of jobs and many business owners continue to highlight their inability to find quality workers. Initial claims rose to their highest level since December—suggesting some cooling in the labor market. Another example of how confusing the scene is. Overall this tight jobs market may keep employers at a disadvantage for a while longer, putting pressure on inflation at a time when the Fed is fighting to bring it down by raising interest rates.

It is for that and other reasons, I have stayed with the view that higher inflation is going to remain stickier than many believe and so will higher rates. Eventually, higher rates will have their intended effect and drag down the economy. However, the recent Silicon Valley Bank failure is going to have more ramifications on the economy and investment scene than some realize.

Inflation and Recession

Some economists believed it was going to be a reason for the Fed to pause their rate hiking program and allow the dust to settle. That bank failure came 24 hours after Chair Powell opened the door to a 50 basis point rate increase, based on what he was eyeing in the data. We’ve lived through plenty of uncertainty in the last 2 years and this latest event takes this economic backdrop to a whole different level.

We have reached a point in the cycle where some folks are trying to attract attention (and ratings, etc.) by whipping up fears about the consequences of the Fed going a bit too far on the upside. Now investors have gone from chattering about 6% Fed Funds to the discussion of rate cuts this year. The forecasts are all over the map and we can expect equity prices to follow along and continue to be very volatile.

However, it isn’t so simple as that. The last CPI report shows inflation is still hovering around the 5% range, which is far away from the 2% target. Ironically, the SVB bank debacle is likely deflationary, and over some time can change the backdrop for the Fed. We will now see a wild overreaction to this event. Banks will be under more scrutiny, and they are likely to tighten lending standards and rein in lending. On the one hand that is positive and might start to make me adjust my view that inflation stays at elevated levels for a LONG time. This event can help the Fed’s crusade against inflation, but that could also take a long time to play out.

On the other hand, it reinforces my view that a recession is coming, and it may not be so mild. When banks rein in lending it’s a drag on growth which raises the recession probabilities. Not to mention it will take Bank earnings down a notch, and that leads right into the notion of an upcoming earnings recession. All of this won’t happen overnight. I will take time to ripple through the economy slowly, and we’ll have to stay vigilant and look for that change. The other factor that may also help the Fed with inflation is the fear of recession that has brought on a decline in Energy prices. If current prices stay at or below present levels for a while that is also a huge positive in the inflation fight. This remains a fluid situation that also suggests investors remain extra vigilant.

Consumers

The analysts that are banking on the consumer to remain resilient and keep spending have plenty of precedents to draw from. Based on history I won’t bet against the consumer either. When they are employed and making money consumers will spend. If they start to run out of money, history also tells us they have no qualms about using credit to supplement their spending habits.

So those tailwinds may be able to prop up the economy enough to prevent a DEEP recession in the near-to-intermediate term. However, despite the strong jobs market, the data shows that real retail sales have been flat for around two years now. At the same time, the personal savings rate is at its lowest point since the Financial Crisis and credit card debt (and credit card interest rates) are at all-time highs. Eventually, that debt load will likely matter and take the economy down, particularly if the slowdown implied by other economic metrics is already implying recession.

I have noted before that the leading economic indicators are not painting a pretty picture. The Conference Board’s Leading Economic Index has declined for ten consecutive months. The yield curve is inverted, at one point more so than at any time in at least a couple of generations, and yet there are still plenty of economists calling for a soft landing. Well, unless this time is different and we have an immaculate overnight recovery, these warning signs will eventually result in a recession, and eventually, that will be the catalyst for rate cuts. I’m not inclined to follow the analysts/economists that are calling for rate cuts this year.

A Fed Pivot

However, despite what some are wishing for or want to believe, a Fed pivot isn’t necessarily going to mark the bottom for stocks. History says it takes a long time for the stock market to bottom out after the central bank enacted the first rate cut of an easing cycle. Consider these BEAR market scenes;

- Less than a year into the dot-com bubble bursting, on Jan. 3, 2001, the Fed began an easing cycle that would see the federal funds rate move from 6.5% to 1.75% in about 11 months. However, it took until Oct. 9, 2002, before the stock market reached its nadir. That’s a 645-calendar-day wait from the initial decrease to the actual bottom.

- As the financial crisis began to take shape, the nation’s central bank reduced the federal funds rate from 5.25% to an eventual range of 0%-0.25%. Though this rate-cutting began on Sept. 18, 2007, the stock market didn’t bottom out until March 9, 2009, or 538 calendar days later.

- The Fed, once again, began cutting its federal funds target rate on July 31, 2019, with this easing cycle taking rates from a range of 2%-2.25% back to 0%-0.25%. With the coronavirus crash hitting its bottom on March 23, 2020, we’re talking about a 236-calendar-day difference between the initial rate cut and the actual market bottom.

While this isn’t a foolproof indicator, we better take note that the initial rate cut doesn’t give anyone an all-clear signal. If the current federal funds rate forecast holds and history repeats itself, a stock market bottom may not be in the cards until late 2024 or well into 2025.

So it is just a question of timing and how long this all takes to play out, and I will repeat, I do not see the Fed cutting rates anytime soon.

Macro Strategy

The investment scene is bifurcated and so is the investor base, and that leads to two different strategies. We can expect volatility to persist in the short term, but those investors that have the wherewithal to look past this valley should not lose focus in the long term. A lot of these market fluctuations are noise for the long-term investor. Those investors should be the drawdown periods as opportunities to accumulate favored areas within a long-term perspective.

Everyone else needs to heed the primary BEAR trend in place. I’ve discussed how it is important to proceed by taking this BEAR market in stages. Last weekend I embarked on the next stage. Let’s be realistic. As rates rise and TINA (“there is no alternative”) turns to TIAA (“there IS an alternative”), at some point, one has to wonder how many investors decide a 4.5% -5% guaranteed risk-free return looks pretty good compared to the volatility experienced with stocks. That by itself keeps the avalanche of money needed to propel stocks to new highs diverted away from the equity markets.

The S&P 500 has now made no progress since April 2021 and remains down around 18% since its early 2022 high. That’s a lot of volatility to sit through for no gains. There are many downside risks present right now, not just in a select few banks. The banks are a symptom of much larger problems as rates rise while the economy weakens. It’s a combination that has caused us to tread more carefully for well over a year now. At the beginning of last year, I said I thought we had entered a “new environment.” I believe we remain in that environment where capital preservation should be the primary goal for most and the downside risks are greater. We can and probably will still see nice bounces. We are seeing that occur now, yet, I want to reiterate that no one should be blindly assuming that all dips are for buying anymore.

The next few weeks will likely be pivotal for the markets, confirming whether this recent banking shock is a “one-off” (my opinion) or if will there be more “Silicon Valley Bank episodes.” So, if we do see this entire liquidity situation contained (my belief) any revival in economic activity is unlikely to be the start of a new robust uptrend. Therein lies the problem. A weaker economy and the most aggressive Fed hiking cycle in history just starting to affect the scene. Therefore, I expect the economy and the U.S. stock market to be VERY challenged in the months ahead.

Global Scene

China Recovery Update: Consumers Showing More Stability, But Don’t Expect Major Government Stimulus

The big picture takeaway is that the consumer recovery is happening, and it is strong but should continue all year in more of a gradual recovery than a severe spike. CGS-CIMB believes government stimulus will be reasonably limited given the existing stimulus of the re-opening of the economy and the desire to keep property prices or inflation from climbing too high.

I would also note that China ended up with a lot of channel inventory of just about everything in 2022, so for products and commodities, demand is a bit lagged from the re-opening as channel inventory is worked down in China.

The Euro STOXX 600 is approaching a very important test. 2000, 2007, and 2015 highs were taken out recently and the index is testing that breakout level. A move below this range would warrant a change in strategy regarding the region. The Euro situation presents another very confusing picture. The breakout in the Eurozone stock markets is telegraphing that there is little to no concern of a global recession anytime soon. In the meantime, Crude Oil and other commodity prices have cratered indicating that the global economy is in trouble.

If the action in the Eurozone is signaling no recession, Energy and commodities become a strong buy here.

The Week On Wall Street

The S&P went back to a rally and started “Fed week” on a positive note. Rallies on both Monday and Tuesday pushed all of the major indices higher with the S&P gaining 2.1% in the first two sessions. All of the gains were wiped out on “Fed day” as this nervous market is still trying to figure out the investment backdrop.

More confusion and uncertainty caused the stock market to chop around the flatline on Thursday and Friday with the S&P finishing the week with a modest 42-point gain. The NASDAQ remained the strongest index with a 1.3% rally making it two straight weeks of gains.

The Fed

There were no real surprises in the Fed announcement this week. A 25 basis point increase. The vote was unanimous.

The Federal Reserve’s statement (emphasis added):

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 4-3/4 to 5 percent. The Committee will closely monitor incoming information and assess the implications for monetary policy. The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective… The projected Federal funds rate for the end of 2023 is now 5.1%-5.6%, up from the prior forecast of 5.1%-5.4%.”

As I have believed for some time, this confirms my view that the Fed isn’t looking to cut rates anytime soon. And the recent banking event isn’t going to change their fight against inflation. NOTHING HAS CHANGED.

The Economy

Housing

Existing home sales jumped 14.5% to 4.58 million in February, that’s much stronger than expected and the biggest pop since July 2020. It follows the 0.7% slide to 4.0 million in January. This breaks a string of 12 consecutive monthly declines to a 2-year low in January. The median sales price declined to $363,000 after sliding to $361,200. This is the lowest price since January 2022 and compares to the record high of $413,800 set in June. Prices fell to a 0.2% y/y pace, the first time in contraction in 131 months.

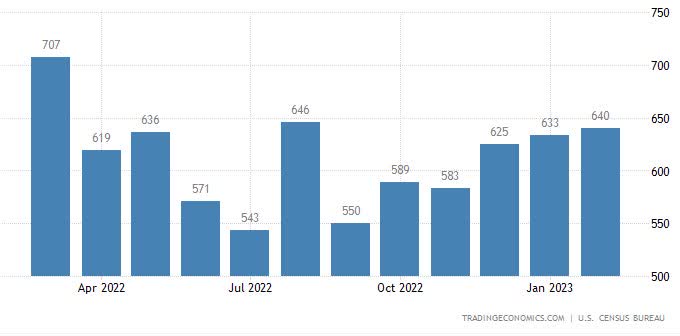

New home sales undershot assumptions with a 1.1% February bounce to an expected 640k after big downward revisions of 41k that sharply trimmed the January figure to 633k from 670k. Sales are nevertheless oscillating well above the 6-year low rate of 543k in July of 2022. New home sales have proven resilient to headwinds from high prices and elevated mortgage rates that have disqualified many buyers.

New Home Sales (www.tradingeconomics.com)

Manufacturing

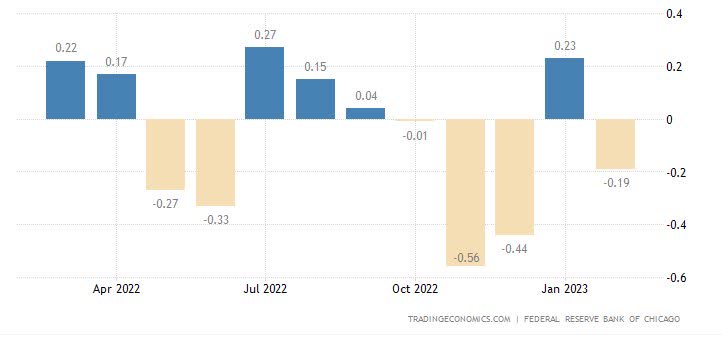

The Chicago Fed National Activity Index declined to -0.19 in February 2023 from +0.23 in January. All four broad categories of indicators used to construct the index made negative contributions, and three categories deteriorated from January.

CFNAI (www.tradingeconomics.com)

US PMI results continue to show improvement and are back to pre-pandemic levels

PMI Composite Output Index at 53.3 (February: 50.1). 10-month high. Services Business Activity Index at 53.8 (February: 50.6). 11-month high. Manufacturing Output Index at 51.0 (February: 47.4). 10-month high. Manufacturing PMI at 49.3 (February: 47.3). 5-month high.

The Global Scene

No sign of inflation slowing in the UK. CPI Rose to 10.4% year over year, making it the sixth straight month of double-digit readings.

PMI reports released on Friday show,

The recovery in the UK has stalled

PMI Composite Output Index at 52.2 (Feb: 53.1). 2-month low.

Services PMI Business Activity Index at 52.8 (Feb: 53.5). 2-month low.

Manufacturing Output Index at 49.0 (Feb: 50.9). 2-month low.

Manufacturing PMI at 48.0 (Feb: 49.3). 2-month low.

Mixed results in the Eurozone

PMI Composite Output Index at 54.1 (Feb: 52.0). 10-month high.

Services PMI Activity Index at 55.6 (Feb: 52.7). 10-month high.

Manufacturing Output Index at 49.9 (Feb: 50.1). 2-month low.

Manufacturing PMI at 47.1 (Feb: 48.5). 4-month low.

Japan remains steady

Composite Output Index, March: 51.9 (February Final: 51.1)

Services Business Activity Index, March: 54.2 (February Final: 54.0)

Manufacturing Output Index, March: 47.4 (February Final: 45.3)

Food For Thought

ESG Will Continue

President Joe Biden issued his first veto on Monday, rejecting a bipartisan bill that would have reversed his Labor Department rule allowing left-wing environmental, social, and governance ((ESG)) policies to be considered in retirement investing.

My views on ESG remain the same. It is a costly endeavor that adds more regulation to an already overregulated corporate America. It also ignores the fiduciary responsibility that is embedded in money management.

Energy

The macroeconomic demand-side risks have become front-and-center for the oil market, as the worries of a global recession have been raised recently. Today, though, I want to address a particular aspect of the supply side of the equation. The complaints and critics of the oil industry keep asking the same question. Why, at a time of healthy oil prices (even after the oil market’s recent selloff), are oil and gas companies drilling so much less than they did during the commodity boom of 2012-2014?

Capital spending surveys of 50 top oil and gas companies around the world show that spending in 2022 was at approximately $360 billion, down 40% from the all-time high of $608 billion set in 2013. The primary explanation is that having been burned by two oil crashes within a decade, management teams have looked at the anti-fossil fuel mindset and decided to employ a strategy of greater capital discipline.

That point applies to every part of the globe, except Saudi Arabia, and other nations that are dependent on oil for survival. A second factor — one that is now embedded here in the US but is even more prevalent in Europe — is that ESG and all that goes with it is pressuring companies to “leave it in the ground”, i.e. produce less and therefore drill less. However, there is another factor that is more below the radar. The fact of the matter is that the industry has lost people, including some of the most highly skilled ones. Even if companies wanted to get back to the levels of capital spending a decade ago, it would be practically impossible due to insufficient labor. The industry has not been immune to what the rest of Corporate America has experienced. Yet no one is acknowledging that fact. Worker availability represents a constraint for many job functions in the industry. The oil industry is no exception. Case in point: petroleum engineers.

These down cycles will affect how management teams think about the business. That’s called prudent management. Widespread headcount reductions thinned the ranks of oil and gas workers — a combination of outright layoffs and early retirements — many of whom have no interest in coming back. To state the obvious, the pandemic wreaked havoc on labor markets in just about every sector of the economy, but oil and gas took a disproportionate hit.

The percentage of Society of Professional Engineers members who are 60-plus currently stands at 22%, up from 14% in 2010. This means that approximately one-quarter of petroleum engineers are on the cusp of retirement within the next few years. This is the textbook manifestation of the “graying” issue. The oil and gas industry’s human capital problem extends beyond professional positions. The vast majority of oil and gas jobs have lower skill levels but despite comparable salaries and enticing signing bonuses, the industry is lacking the number of workers to even consider expanding operations.

So while the focus has been on demand, we should also keep in mind that supply won’t be ratcheting higher anytime soon. It is the reason why some oil analysts continue to say that even with a recession, crude oil prices can remain resilient.

The Daily chart of the S&P 500 (SP500)

Two steps up, one big step back, then a pause. That matched the angst over the latest event that is bothering the stock market.

S&P 500 (www.freestockcharts.com)

The S&P sits squarely in the middle of its recent trading range and offers no clues as to where it wants to go next.

Investment Backdrop

The rangebound market in the last few months has been way more complex, than the severe declines of last year. I’m always looking for a trend (short, intermediate, or long) to profit from, so I just want the market to pick a direction and go there. When we get all of these false breakouts and false breakdowns it becomes a lot more confusing and challenging. But this type of market can continue indefinitely, which is why I have said that most should not be doing too much right now other than trying not to lose money.

Last week we noted that despite the disturbing financial headlines, the major averages are holding in there relatively well all considered. That had me wondering if the market was banking on a change in Fed policy. Coming into this week, the S&P 500 has not made a lower low in a week, while the more tech-heavy NASDAQ 100 hit its highest point since February 15 on March 17th. However, conflicting signals remain.

When I take a close look at the NAZ 100, the gain is concentrated in a few of the large-cap mega Tech stocks. Looking at the general market, I will note that breadth has not been nearly as good there as well. There have been no 80% upside days the way that I measure them, while there have been one actual 90% downside day and two 80% downside days that just missed being 90% downside days (including one last Friday).

That infers distribution under the surface of the market. Meanwhile, the S&P 500 broke thru the initial resistance zone, and up until investors realized there was no change coming in Fed policy looked poised for a longer rally. As it turns out this week was important. It ONCE AGIN clarified the Fed stance and squashed the “Hope” that rate cuts were coming.

Bottom line: The market did not overcome this Fed meeting and see the S&P 500 break out and hold above ~3970, it is going to be a huge step in the right direction to possibly getting that move up toward ~4100-4200 which was one of the upside targets all along. If we turn around and take out Friday’s lows around 3900, though, it’s going to support that we remain in a downtrend and we have to assume it continues until provided with enough evidence otherwise.

Growth Vs. Value

“Growth” has rebounded sharply and is trouncing “Value” lately. We’ve seen how the flight to safety has cratered near-term interest rates. That is a short-term tailwind for technology and is catalyzing the rebound in a sector that was decimated last year. On the other side “value” has been the clear winner in this BEAR market. Of course, one leg of the value stool (Financials) has just been taken out handily with the debacle in the banks. That left last year’s big winner, Energy holding the baton. However, nothing goes up forever, and so far this year what we may be witnessing is a reversion to the mean for energy, combined with an overdue, oversold bounce for technology.

We’ll soon find out how far these new trends go, but I’m not ready to make any significant changes to strategy just yet. As always we will have to keep an OPEN mind and see where the “technical” evidence leads us. This recent action also tells us how diversity must be a part of any strategy. While we can overweight or underweight in a particular area of the market we should not abandon it completely. The fact that we’ve maintained CORE technology holdings has allowed the portfolio to reap some of the rewards from this bounce.

Sectors

Energy

It’s no secret that Oil and Oil stocks have been arguably my favorite areas of the market over the past couple of years. That has worked out very well, but even Oil and Oil Service stocks have not been immune to the recent fear and selling. As long as the broad market doesn’t collapse here (which is still a possibility), something like the VanEck Vectors Oil Services ETF (OIH), and the Dow Jones Oil Services ETF (IEZ) are at decent entry levels.

The Energy ETF (XLE) teetered at support last week and the BULLS stepped up and defended the support range.

Financials

The recent events in the banking system have now swallowed three U.S. institutions — Silvergate, Silicon Valley Bank, and Signature Bank — and threatened First Republic Bank. There was a legitimate fear that other regional banks could have similar difficulties. In today’s world, any fear – warranted or not – can go viral in minutes and threaten an otherwise healthy financial institution. The same can be said for the underlying shares of these banks.

Never lose sight of the fact that investors sell first, and ask questions later. It’s always, Fire, Ready, Aim. The charts of the Financial ETF (XLF) and the Regional Bank ETF (KRE) are now completely broken down. I think that this banking debacle is not systemic. Perhaps I’m showing a bit of naivety, but I simply can’t believe that there are that many mismanaged financial institutions operating today. One good piece of evidence that banks are not a systemic issue now is the fact that credit markets are still reasonably well-behaved. In addition, we did NOT experience a general stock market crash while this was playing out.

One might take that as an endorsement to load up on bank stocks, but that isn’t the case. First, we can see that emotion is in charge, and that means anything can happen in the short term. Secondly and most important these stocks are buried in BEAR market trends. Other than dabbling with a call writing position or trying to build a longer-term portfolio, it’s best to let this situation stabilize. One name I did pick up in this debacle was Charles Schwab (SCHW). They should not be mentioned in the same paragraph never mind the same sentence as SVB. SCHW is a primarily fee-based quality franchise.

While the liability side of bank balance sheets has been the source of enormous drama this past week, the asset side of bank balance sheets remains in very good shape. As a percentage of total loans, noncurrent loan balances held by banks are among the lowest in history; that number can deteriorate a fair bit without a major impact on bank capital. Also, keep in mind that more than half of the total value of all bank deposits in the US are insured.

With all the turmoil in the financial sector, it is worth checking in on banking sector delinquency rates. Headed into this year, the aggregate delinquency rate of all loans and leases at commercial banks was sitting at a record low of 1.19% as of data from the Fed through Q4 2022 released late last month.

The Bottom Line: This isn’t another financial crisis in the making. The laser should be squarely focused on the mismanagement of bank officials at these institutions and the dereliction of duty on the part of the Federal regulators in charge of oversight.

Healthcare

The group (XLV) did find some support this week and attempted a weak bounce with a 1.5% gain. The sector has been a laggard this year and until the group shows it can get back into a BULL trend, selectivity is the key. While XLV is down 7% this year, my healthcare stock for the year – Lantheus Holdings (LNTH) is up 58% YTD.

Biotech

The Biotech ETF (XBI) entered the trading week a whisker away from breaking the BEAR to BULL reversal pattern that began last June. Weak price action remained in place and it appears the group could be headed back to the June ’22 breakout level. The group is being shunned as investor interest has turned to companies that will not need to visit the capital markets to raise cash.

Gold and Silver

The quick reversals in fortune have not been isolated to the stock market. Both of these precious metals have rallied strongly after they appeared to be broken down earlier in the month. Longer-term investors are now being rewarded for their patience.

Uranium

The one metal that should have a tailwind behind it has fallen off a cliff. Uranium is back down to the lower end of the trading range. If you are a believer that at some point nuclear energy will eventually be the answer to a successful “green transition,” then here is an opportunity. I continue to HOLD my Uranium position.

Technology

The NASDAQ Composite has rallied 13% in 2023. The NASDAQ 100 has tacked on 17+% Year to date and is attempting to break out into a BULL market trend. It’s all about interest rates as investors are flocking to the group with the belief rates will remain at these levels, thus removing the strong headwinds.

Market participants are also seeking what they believe is a refuge in solid balance sheets of companies that do not need to head to the capital markets anytime soon. While these are near-term technical signals that can’t be dismissed, the longer-term trend in both indices is decidedly BEARISH. I’ll keep an open mind, but until proven otherwise this is nothing more than a BEAR market rally. So, I am willing to sit this one out until the longer-term trends show significant improvement.

Semiconductors Sub-Sector

Uncertainty? confusion? conflicting signals? — All of the above.

There may be a crisis out there roiling the US and global banking sector, but you wouldn’t know it looking at the chart of the semiconductors. Year to date, the Philadelphia Semiconductor Index (SOX) is still up 23%, and through Friday’s close is challenging the February 2nd high.

More importantly, SOX is on the cusp of breaking the 20-month moving average trendline and that would be the first step in establishing a new BULL market for the group. It is a signal that IF triggered should not be ignored. The group’s relative strength has easily eclipsed the S&P this year, and in the past, we have used that as a sign of overall market strength. We’ll know soon enough if this is a false breakout OR a sign the entire market is about to get a lift.

Bespoke Investment Group;

Of further note; following every prior period where the relative strength of semis first hit a 52-week high, the S&P 500 was higher six and twelve months later every time.

Final Thoughts

This isn’t 2008, and the recent banking event isn’t “systemic.” Today’s challenges have to do with how banks have chosen to manage their deposit liabilities in an environment of rising global interest rates. In essence, there were horrific financial management decisions made, and we now are aware of a Fed reserve regulatory body in California that has shown to be incompetent as well.

Under the scope of the Treasury Secretary, the FDIC’s action to make all depositors whole, the Fed’s announcement of a Bank Term Funding Program to provide liquidity, and the $30 billion cash injection for the First Republic by a group of the country’s largest banks, stabilized the situation. After consideration, Secretary Yellen walked back her initial comments on a universal bailout. Finally, some common sense entered the scene and perhaps this administration realized they can’t “promise” that bailout without Congressional approval.

That proposal is a slippery slope in many ways and it is also inflationary. It would have caused major ramifications for the financial system and the economy in the future. The bailout of SVB is quite controversial and may have already set a dangerous precedent. I’ll have a detailed analysis of that event next week. Suffice it to say a universal bailout would have been the largest policy mistake to date, and we’ve seen many gaffes since 2021 which sent inflation to 40-year highs.

The entire BEAR market has been filled with uncertainty. After all, that is what BEARS feed on. I believe we are at a point in time where we have to start using degrees of uncertainty to describe the near-term scene. Now that we have added angst over the banking scene to the list of concerns regarding the Fed, inflation, rising interest rates, geopolitical tensions, etc., last weekend I told members of my service the UNCERTAINTY level had moved to Defcon 3.

It’s always a given that the stock market will march to a different tune to confuse investors, and the BULLS want to note that this is a very strong seasonal pattern for stocks that can last well into April. Perhaps that is the reason stocks held up reasonably well in the face of these unsettling headlines. While the gains have been modest the S&P has posted back-to-back weekly gains. There will be periods that will produce strong moves and countermoves. Lately, this market loves to tease, then hurt both BEARS and BULLS.

We can add this to the uncertainty of the near-term scene as well. This is a market backdrop that will take out the amateurs as well as seasoned investors.

THANKS to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!