We Are Learning: QE And QT Are Still New To Us

Mark Wilson

We are learning.

What we are learning about is how the Federal Reserve’s monetary programs of quantitative easing (QE) and quantitative tightening (QT) affect the banking system.

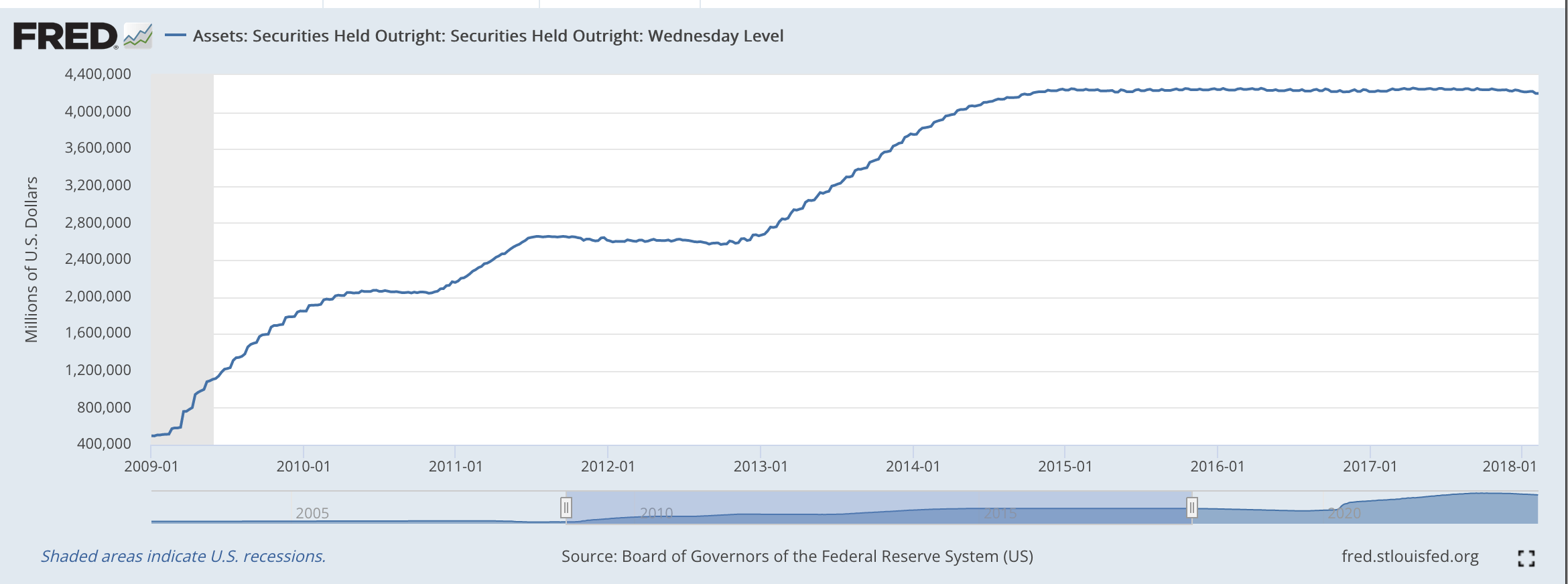

Quantitative easing came into the world in the 2010s as Ben Bernanke, chairman of the Board of Governors of the Federal Reserve System, constructed a monetary policy program that he believed would help the U.S. economy recover from the Great Recession of 2007-2009 and then proceed into a sustainable period of economic growth.

Quantitative easing occurs when the Federal Reserve buys a consistent amount of securities for its portfolio on a monthly basis for an extended period of time.

Mr. Bernanke oversaw two rounds of quantitative easing on his watch, Q1 and Q2.

Securities Held Outright (Federal Reserve)

Mr. Bernanke was Fed chair from February 1, 2006, to January 31, 2014.

Q1 began before the Great Recession ended, and Q2 began early in 2013.

Janet Yellen became the chair of the Board of Governors on February 3, 2014.

No rounds of quantitative easing took place during Ms. Yellen’s tenure at the Fed.

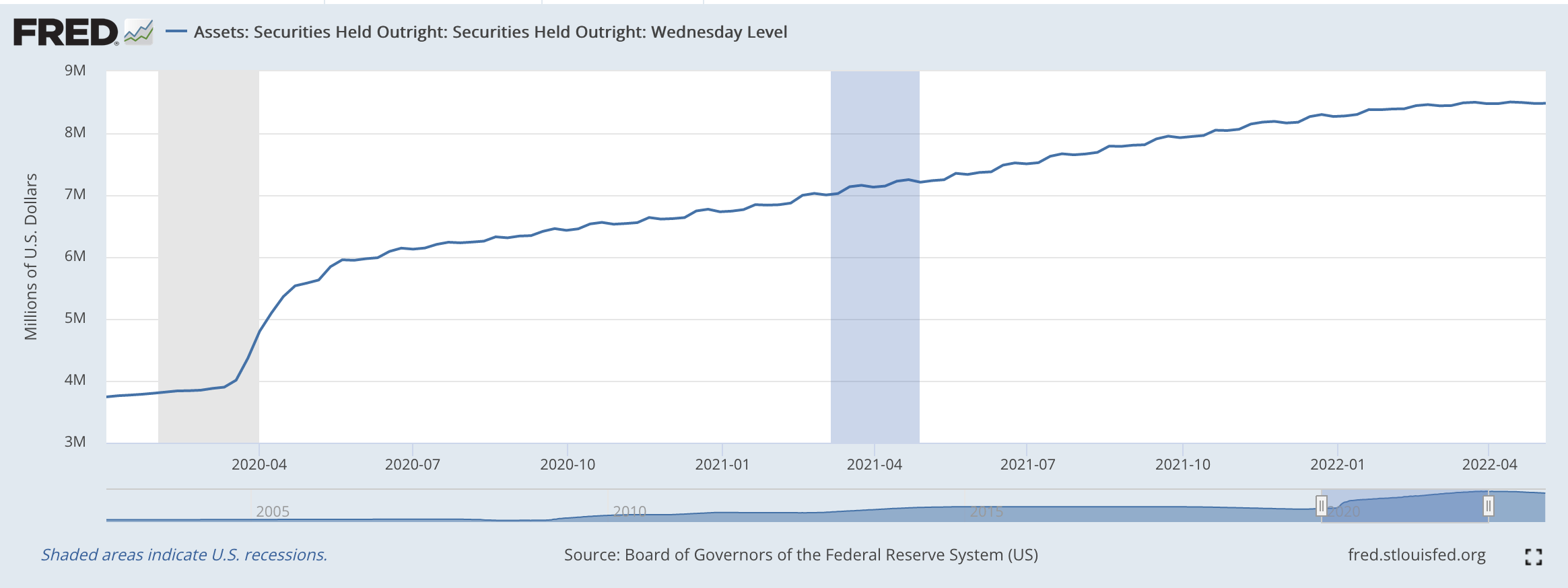

Q3 came about during the time of Jerome Powell, who became Chairman of the Board of Governors on February 5, 2018.

Securities Held Outright (Federal Reserve)

Q3 began before the end of the brief recession resulting from the spread of the Covid-19 pandemic and continued on into early 2022.

The Fed’s securities portfolio “peaked out” on May 13, 2022.

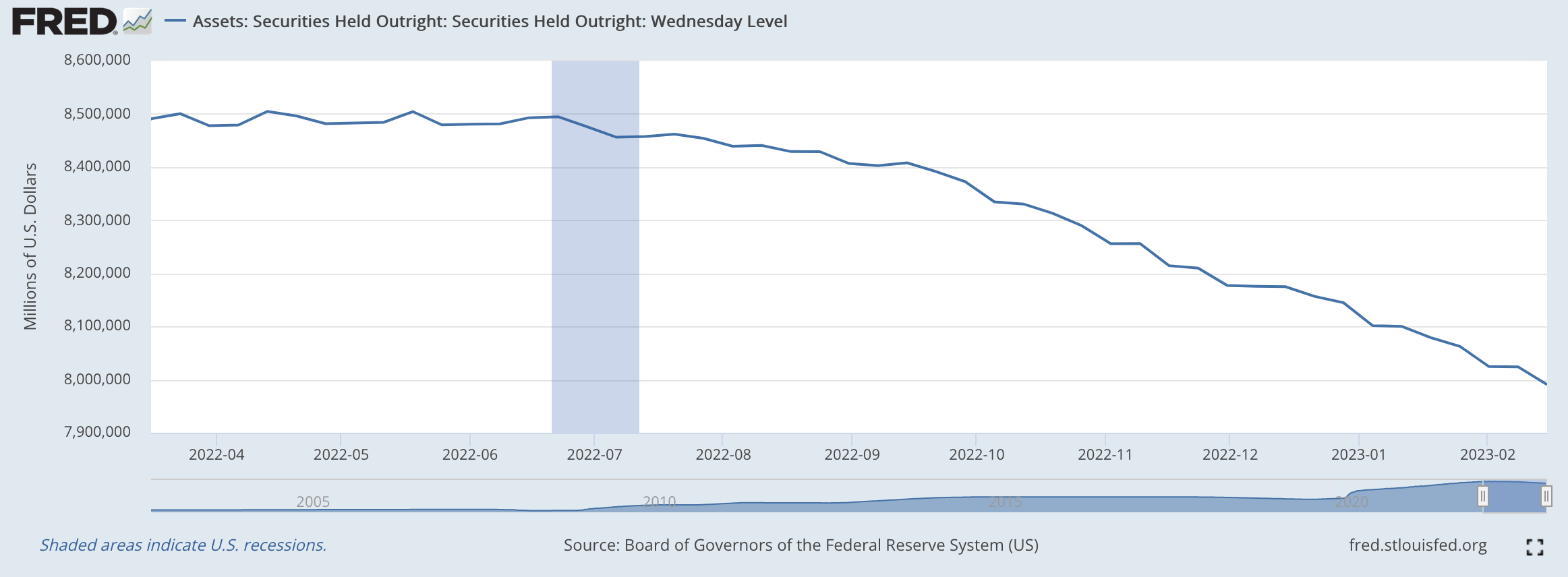

Quantitative Tightening

Quantitative tightening began in the middle of March 2022.

Securities Held Outright (Federal Reserve)

As can be seen, the securities portfolio totaled right around $8.5 trillion on March 16, 2022.

The decline in the portfolio since that date has been steady and continuous.

On Wednesday, February 15, the securities portfolio totaled just below $8.0 trillion.

The plan is for quantitative tightening to go on for some time yet, perhaps even heading into 2024. How long QT1 goes on is, of course, a big question mark. Whether it will just be phased out or terminated because of a market collapse is not known at this time.

But, quantitative tightening has now been underway for just about one year.

What Now?

So, the question is “what happens now?”

Megan Greene, writing in the Financial Times has tried to give us a better picture of the situation.

Ms. Greene also refers to a recent paper written by Raghuram Rajan, of the University of Chicago, and others, digging into the whole picture. Mr. Rajan was also the governor of the Reserve Bank of India.

First, there are a lot of unknowns in the current situation.

The Federal Reserve has never conducted a policy of quantitative tightening before.

Sure, it went through three rounds of quantitative easing earlier, but quantitative tightening is not quantitative easing.

As Ms. Greene states,

“QT isn’t just QE in reverse.”

Ms. Greene presents the argument that banks act differently in QT than they do in QE.

“Rajan argues (that) commercial banks change their behavior when the central bank expands its balance sheet, but do not change it back again when the balance sheet shrinks.”

When the Fed shrinks its securities portfolio:

“banks substitute lost reserves with other assets that are eligible collateral in repo transactions, to remain confident of getting enough cash if they need it.”

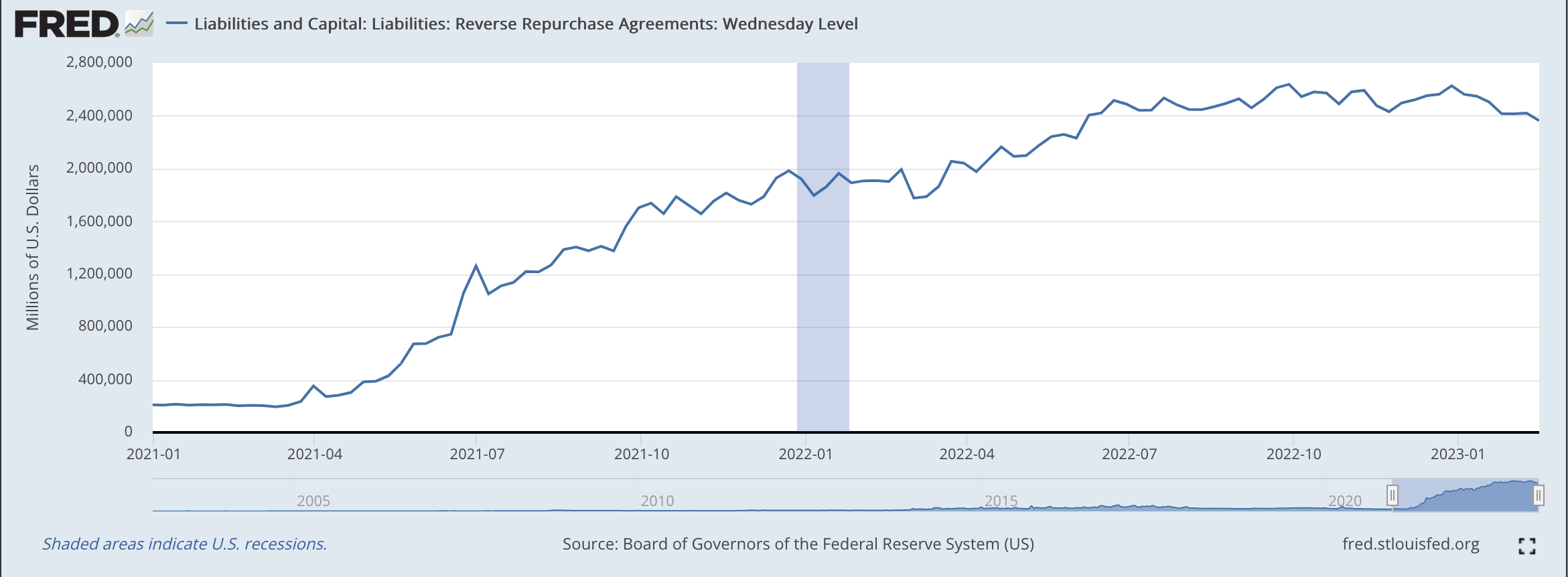

Notice what has happened to the Fed’s Reverse Repo account since the beginning of the current financial struggles up through the period of QT.

Reverse Repurchase Agreements (Federal Reserve)

The Federal Reserve has left this option open to the commercial banks so that they can “manage” their reserve positions more comfortably in the face of the Fed, regularly, moving up its policy rate of interest.

Reverse repos are the “tool” the banks use to keep markets calm.

“Banks make greater claims on the system’s liquidity during QT….”

But, this outlet is necessary to continue with QT and achieve the Fed’s goal of reducing the Fed’s security portfolio.

The dilemma the Fed faces is that when it is tightening up, liquidity in the banking system falls and a financial crisis can take place.

The Fed reduces this possibility by providing an “escape hatch,” a tool that can let the banks themselves relieve the liquidity pressures they face given the tightening the Federal Reserve is doing.

The Federal Reserve can always step in and buy bonds again to “paper over” a liquidity crisis. The problem with this is that it just “rachets up banks’ demands for liquidity still further–and makes QT even harder to pull off down the line.”

Thus, the Fed faces a different situation when it is tightening up on its monetary policy than when it is easing.

And, since this is the first time through this particular exercise of QT, the uncertainty of how the banks will react is huge.

Ms. Greene concludes her essay by saying that “the best way to get out of QE may be not to start it in the first place. You don’t have to check out if you’ve never checked in.”

Here We Are

But, here we are.

The Federal Reserve has been using QT for just about one year.

The commercial banking system has protected its position by using the Fed’s reverse repo window, up to the tune of about $2.5 trillion.

And, we are still not near a resolution to the inflation situation.

Most of all, since this is the first time through this exercise with QT, we really don’t know how the Federal Reserve will react going forward.

Ms. Greene suggests the usual solution to this kind of problem in the banking system…increase the capital the commercial banks must carry so that they can assume more losses.

But, that is not going to happen.

Quantitative easing worked very well. A financial collapse was avoided; asset prices rose quite a bit (increasing income/wealth division); consumer price inflation remained relatively modest (until the Covid-19 pandemic hit); the economy grew modestly; and financial risk seemed to be minimized.

The results of quantitative tightening are unknown at this point.

Investors seem to be at the point where they believe that there will be a market drop or that, to avoid a market drop, the Fed will “pivot” and begin to “pump up” its securities once again.

At this point there seem to be few optimists talking about a Federal Reserve that maintains its cool, that carries the financial markets through the period of QT, and who then works to underwrite a further recovery into the new world of digital currencies and electronic networks.

We are all learning as we proceed through these difficult times.