Verizon May Now Have A Dividend Problem (Rating Downgrade) (NYSE:VZ)

NurPhoto/NurPhoto via Getty Images![]()

Telecommunications giant Verizon Communications Inc. (NYSE:VZ) submitted its earnings sheet for the fourth quarter on Tuesday, and the company met expectations regarding earnings and beat expectations on the top line. Verizon also saw accelerating momentum in its broadband business where it signed on a record number of new subscribers in Q4’22, but there were negatives as well: Verizon’s free cash flow (“FCF”) did not cover the fourth quarter dividend payout and Verizon issued a very light forecast for its adjusted EBITDA. For those reasons, I am downgrading my rating on Verizon from strong buy to hold!

Verizon’s Q4 vs. expectations

Verizon reported Q4 2022 adjusted earnings of $1.19 per-share, which met average EPS expectations. Verizon, however, beat top line expectations by about $108M and reported revenues of $35.3B.

Source: Seeking Alpha

Broadband business remains Verizon’s bright spot

I highlighted Verizon’s broadband momentum as a top reason to buy the stock in the past and the broadband business remained a bright spot for the telecommunications company. Verizon added a record 416 thousand new customers to its broadband business in Q4’22 — including 379 thousand Fixed Wireless Access additions — which showed an acceleration over Verizon’s Q3’22 net-add of 377 thousand. My expectation was for 420-430 thousand new subscribers which was slightly above the reported net-add figure. Nonetheless, Verizon showed strong execution in its broadband business and added a total of 1.29M new subscribers in its broadband segment due to an aggressive broadband roll-out effort, reflecting an increase in total net-adds of 215% compared to FY 2021.

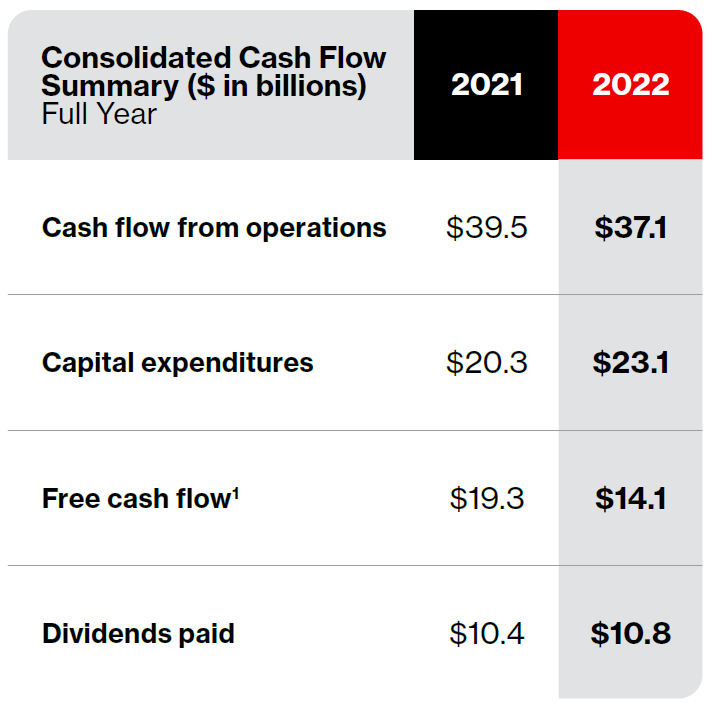

Disappointing free cash flow, deteriorating dividend coverage

Verizon reported free cash flow of $1.7B in the fourth quarter which was not enough to cover the $2.7B quarterly dividend payment… it fell a full billion short of the company’s dividend commitment. On a full-year basis, Verizon had free cash flow of $14.1B, showing a decline of 27% year over year. The cumulative dividend payout of $10.8B was covered by free cash flow, but the FCF payout ratio has worsened considerably in FY 2022.

In FY 2021, Verizon had a payout ratio of 54% which increased to 77% in FY 2022. The deteriorating dividend coverage puts the dividend at risk and I believe weaker free cash flow prospects make Verizon much less attractive as a dividend play.

Source: Verizon

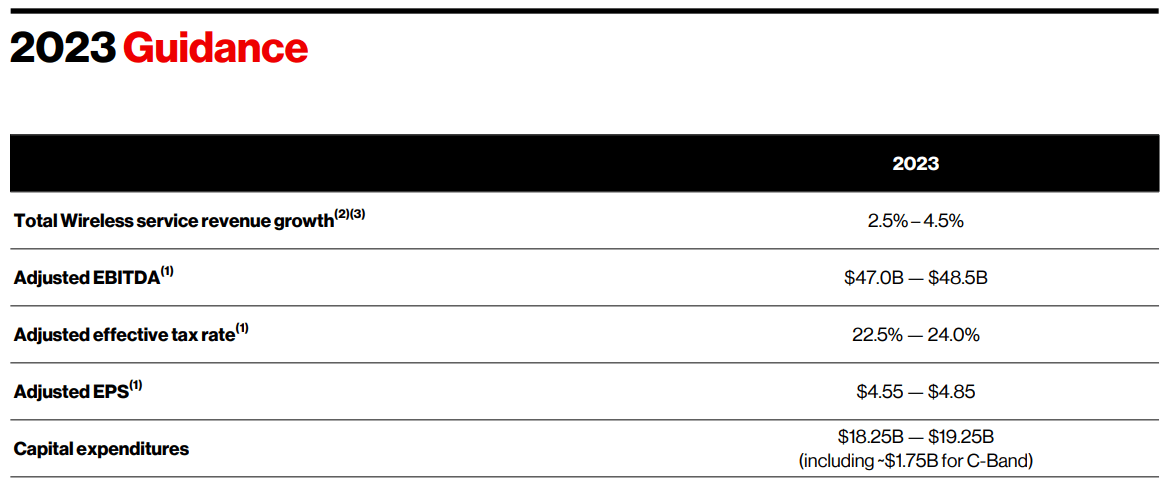

Disappointing outlook for FY 2023

The outlook for FY 2023 is not great either. Verizon projects just $47.0-48.5B in adjusted EBITDA which implies a year over year growth rate of (0.3)% so the telecommunications company expects virtually no growth at all in one of its most important performance metrics. The decline in adjusted EBITDA is driven by declining total wireless service revenue growth (consumer and business) which is expected to decelerate from more than 8% in FY 2022 to 2.5-4.5% in FY 2023.

Verizon’s adjusted EPS is expected to be $4.55-4.85 which implies a 9.3% year over year drop due to slowing wireless service growth and moderating economic growth.

Source: Verizon

Verizon’s valuation

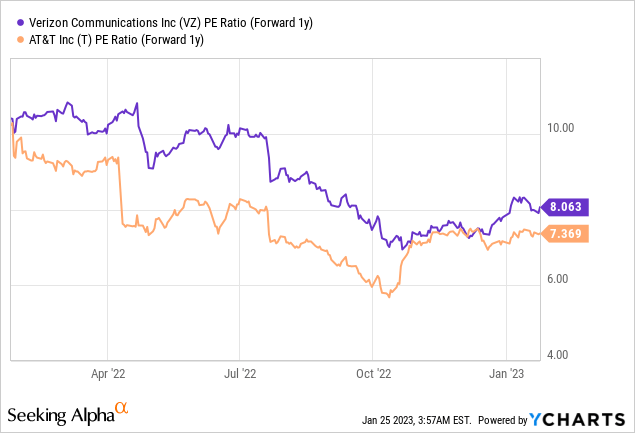

Verizon generated just $14.1B in free cash flow in FY 2022 and considering the disappointing adjusted EBITDA forecast for FY 2023, the company is not going to see much higher free cash flow growth this year either. With zero growth in free cash flow in FY 2023, Verizon is valued at a P/FCF ratio of 12.0 X which is no longer bargain territory. AT&T (T) has not released its free cash flow for FY 2022 (at the time of writing), so I would assume that AT&T has seen a similar drop in free cash flow in the fourth quarter

Based off of earnings, Verizon is valued at a P/E ratio of 8.1 X compared to AT&T’s P/E ratio of 7.4 X. I like AT&T more than Verizon because AT&T also benefits from strong momentum in the broadband segment and is more attractive from a valuation point of view than Verizon.

Risks with Verizon

Risks for Verizon, especially regarding the dividend, have definitely increased after the telecommunications company submitted its earnings sheet for the fourth quarter. Deteriorating dividend coverage, based off of free cash flow, is clearly a (growing) risk for Verizon going forward and it is the key reason behind me down-grading my rating from strong buy to hold. The light outlook for adjusted EBITDA, despite Q4’22 momentum in broadband subscribers, is also a net-negative for the stock and it may weigh on Verizon’s shares in the near future.

Final thoughts

Verizon Communications Inc.’s outlook for FY 2023, which calls for zero growth in adjusted EBITDA, is a problem, and so is the steep year-over-year increase in the dividend payout ratio. While I don’t believe that the Verizon Communications Inc. dividend is at immediate risk of getting eliminated, it may have to get cut in order to align it with Verizon’s lower free cash flow. Since Verizon’s wireless services revenue growth is also expected to moderate this year, the firm’s dividend is now more risky than in FY 2022. Verizon’s stock is still attractively valued based off of earnings, but the telecommunications company clearly lost in attractiveness as a dividend play!