The Bears Are Getting Frustrated

Freder

Confidence in the global banking system improved over the weekend with the UBS acquisition of Credit Suisse, and investors in the US are starting to move back into risk assets as the tail risks from the liquidity squeeze are gradually being reduced. Yesterday’s one exception was First Republic Bank (FRC), which plunged another 47% to a record low, despite efforts by the largest banks to strengthen its balance sheet with a $30 billion liquidity infusion. The difference yesterday was that the financial sector of the S&P 500 and the SPDR S&P Regional Banking ETF (KRE) both finished the session up more than 1%. That tells me the existing issues of both confidence and liquidity are isolated and not systemic. The markets seem to agree. The major market averages posted impressive gains that look to continue into today’s trading session.

Finviz

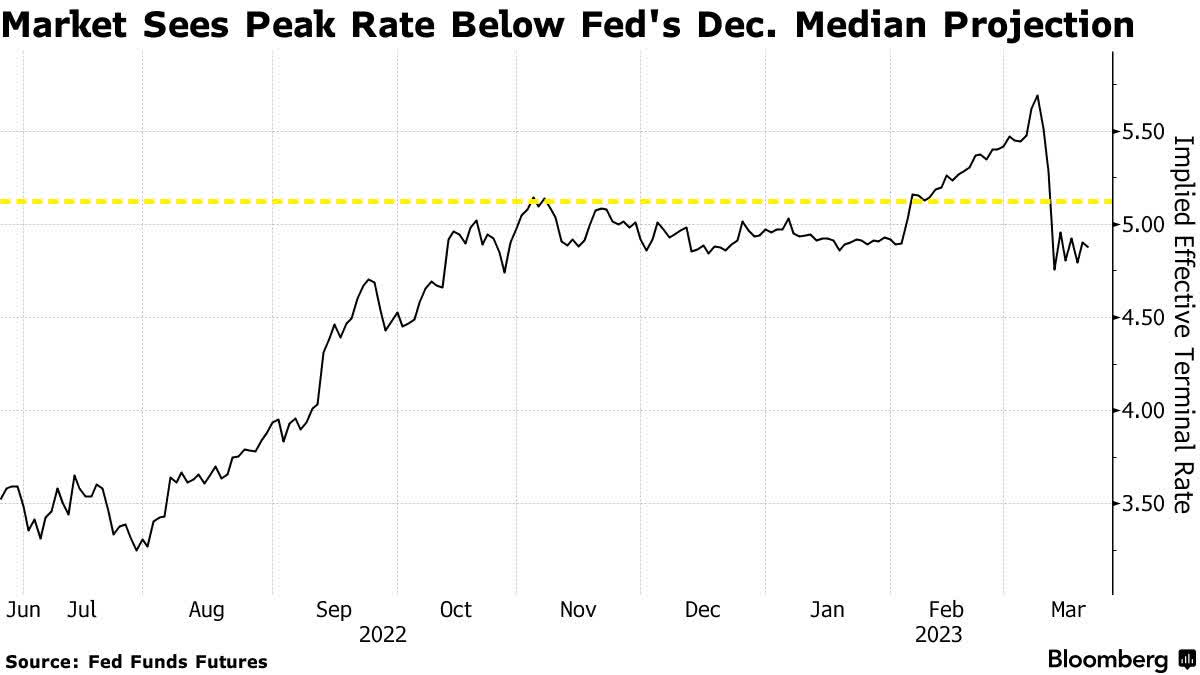

The upside of recent banking turmoil is that it has alerted the Fed to the fact that its rate-hike campaign is having its intended impact, and that it needs to pause and monitor the economy before pursuing a more aggressive policy. That is the market’s message, as expectations for a terminal rate as high as 6% two weeks ago have plunged below 5%. I think that is ideal because it will give Fed officials more time to see that disinflation is firmly entrenched, and that we are on track to meet the Fed’s goal of a 2% rate of inflation in late 2023 or early 2024. Again, this is why risk assets are rebounding to the dismay of disgruntled bears who were hoping for a retest of the October lows.

Bloomberg

Morgan Stanley’s chief market strategist, who has come to be known as the biggest bear on Wall Street, is doubling down on his frustration, as the S&P 500 is not cooperating with his doom and gloom forecast. Riding on the tailcoats of recent turmoil in the banking sector, he asserts that this will start the beginning of a “vicious” end to the bear market, as “falling credit availability squeezes growth out of the economy,” and investors finally recognize that profit forecasts are too high, considering the pending downturn in economic activity.

Bloomberg

The problem with his forecast is that credit availability is not yet an issue. In fact, the lenders who are most important to Main Street are seeing virtually no impact at all from recent events other than an increase in deposits. There are approximately 4,750 community banks across the country that hold about $5 trillion in deposits and account for about 60% of all small business loans. Small businesses employ half the workforce. These banks are the tip of the spear in terms of financial stress, and they don’t see what Wilson is selling yet.

Community bank leaders not only see deposits on the rise, but they indicate they are not tightening lending standards. Therefore, its business as usual. The percentage of insured deposits at community banks stands at well above 60%, and they appear to be far more trustworthy than their larger counterparts. If this has been a crisis of confidence, as I have contended, the community banking system is not a part of it.

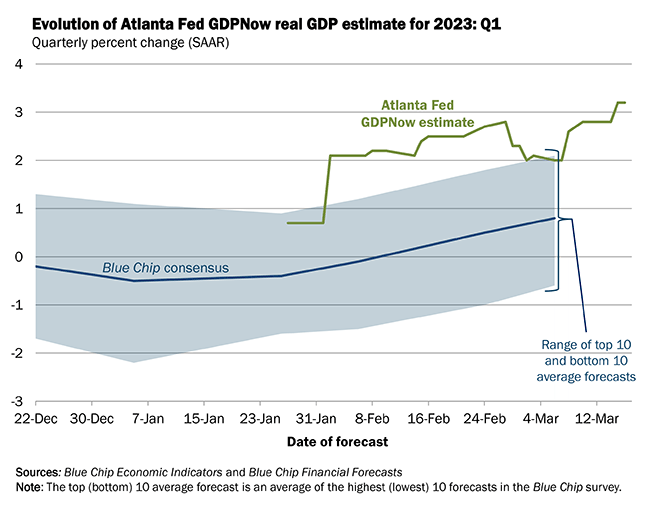

As for the pending downturn in economic growth, it isn’t on the horizon yet. The Atlanta Fed’s GDPNow estimate has been increasing over the past two weeks from 2% to 3.2%. The consensus on Wall Street has also reversed from an expected contraction to growth of nearly 1%.

Atlanta Fed

The rate of economic growth is sustaining, while wage growth and inflation slowly recede. That combination spells soft landing. It may not suggest that the S&P 500 rallies to all-time highs this year or next, but it strongly advocates for an end to the bear market as of last October, and the beginning of a new bull once the index surpasses 4,300, which would be a 20% gain off the October low.