T. Rowe Price (TROW): High-Yield And Strong Dividend Growth

Darren415

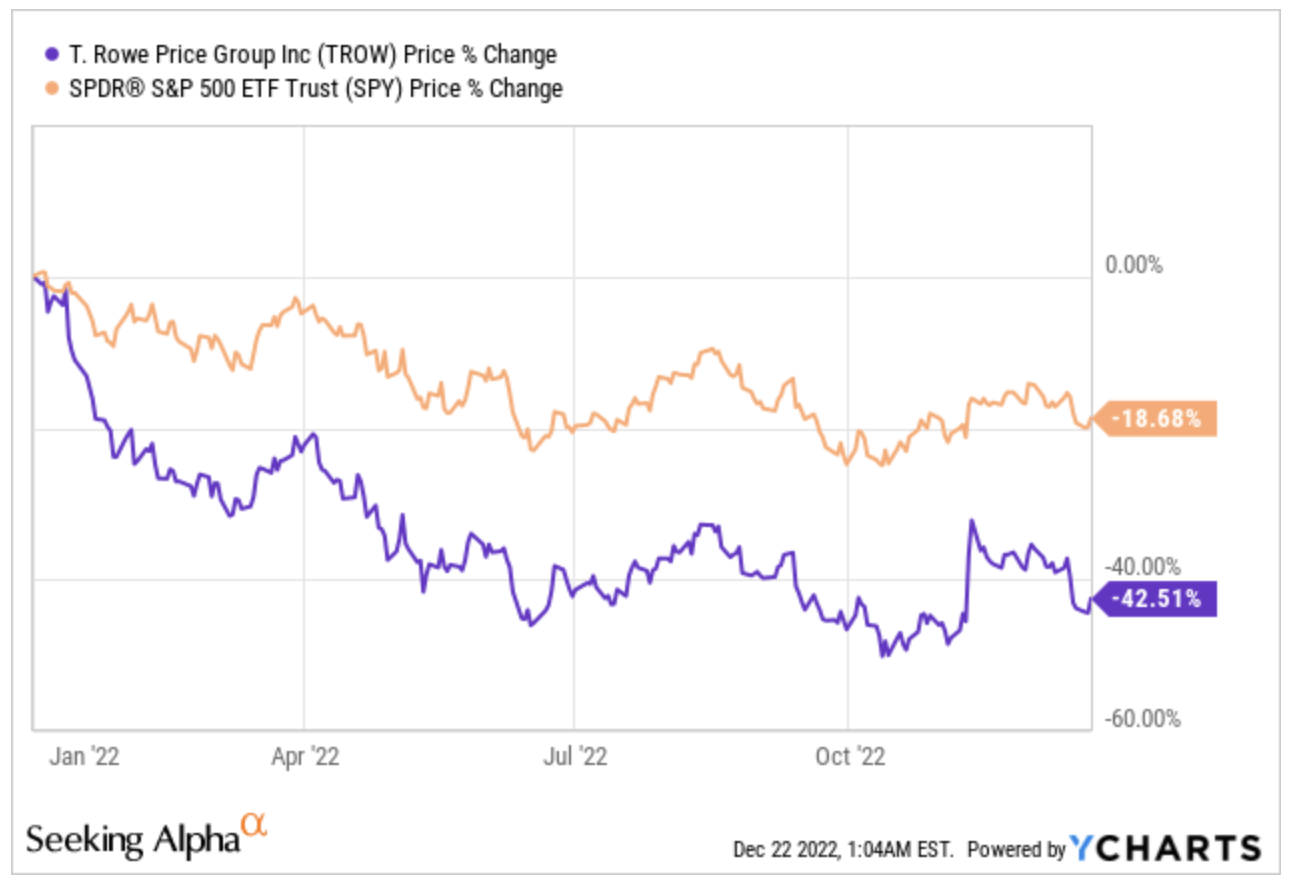

Shares of asset manager T. Rowe Price (NASDAQ:TROW) failed to find any footing in 2022 as the markets entered a bear market. Shares of TROW are down 42% on the year, far underperforming the S&P 500 (SPY), which is down 19% on the year.

YCharts

Given the strong pullback, shares of TROW look quite intriguing at current levels from a valuation and a dividend standpoint.

Being an asset manager with strong ties to the stock market, it is no surprise that the stock is down given what we have seen in the US stock market this year.

After all, the company makes the majority of its revenues through investment advisory fees. As the stock market has fallen, so have the portfolio values of their customers, thus lower fees to collect, as they tend to be a fixed percentage based on the portfolio value.

Another issue the company has run into, also related to the greater stock market performance, has been customers pulling their money from the platform entirely. The company ended Q3 ’22 with $1.23 billion in assets under management, or AUM. This is a 23.7% decrease from the same period a year ago and a 6.1% decrease from three months earlier.

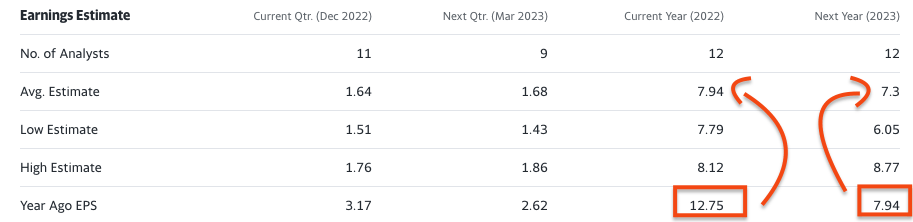

Unfortunately, many are predicting a recession in the first half of 2023, assuming we are not already in one, which will likely lead to further earnings estimates being revised. Being an asset manager, earnings estimates have already been cut.

Looking at this chart here, you can see how drastically those estimates have come down from the past year.

Yahoo Finance

Economists believe the ’23 recession will likely be mild, but let’s go back to the Great Recession to see how things played out in the event the next recession is more severe than anticipated. From 2007 to 2008, T. Rowe’s AUM fell from $400 million to $276 million, plummeting 31%. However, within the next 12 months, the AUM has almost entirely recovered. Given that, with AUM down 24% year over year, we are nearing the bottom.

Remember, the stock market is forward-thinking and stocks will recover far earlier than the greater economy, usually six to nine months earlier on average. Knowing that, I am on the lookout for high-quality businesses trading at a nice discount.

Before we look at the dividend and valuation, let’s take a closer look at some financial metrics. The company has $2.4 billion of cash on hand and no debt.

Free cash flow through the first nine months of the year was $2.3 billion, down 20% from $2.9 billion over the same period a year ago. This is expected given the drop in revenues we have seen.

Nonetheless, the company has a very strong balance sheet that they are able to lean on when times are tough. In addition, cash flow, although is down, it is still robust and able to pay a growing dividend.

Speaking of the dividend, TROW has paid a growing dividend for 36 consecutive years and counting, making them a Dividend Aristocrat.

Over the past five years, the company has increased the dividend at an average annual clip of 16%. Not only are they increasing their dividend, but they are doing it at a fast pace, which is great for investors. The dividend is also well covered with a 49% payout ratio.

The increasing dividend, combined with the drop in share price, has given shares of TROW a dividend yield of 4.4%, which is quite intriguing. To put this in perspective, shares of TROW have a 5-year average dividend yield of 2.6%.

Seeking Alpha

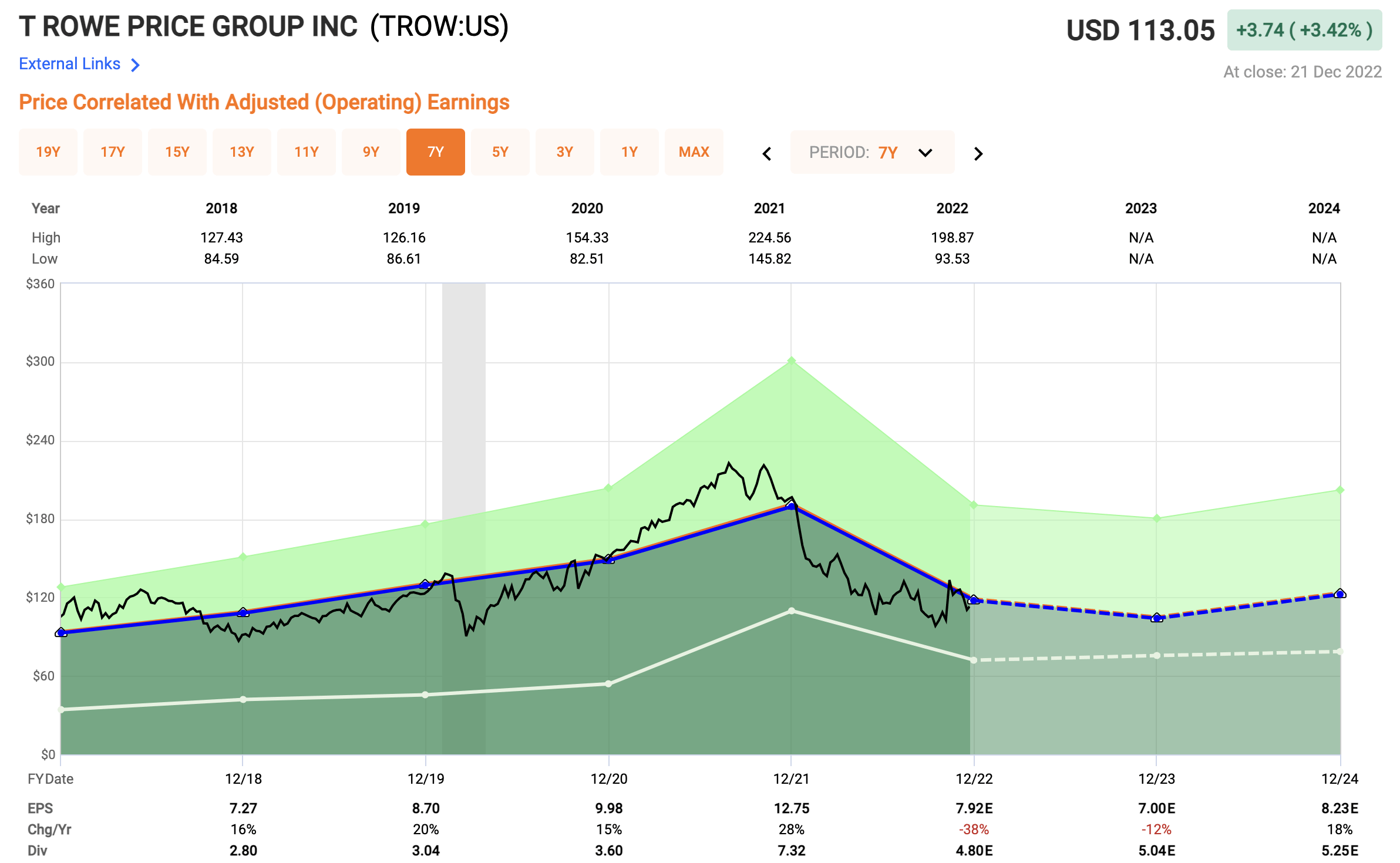

The dividend alone looks great, but now let me tell you about the valuation. Shares of TROW currently trade at an earnings multiple of 14x, which is slightly below the company’s five-year average. 2023 could provide more sideways results before returning to growth in 2024. Looking out to 2024, analysts expect EPS of $8.23, meaning shares trade at a forward earnings multiple of just 13.7x.

FAST Graphs

Investor Takeaway

T. Rowe Price has proven to be a tremendous stock to own over the years for dividend investors. However, 2022 has proven to be a different story and the stock has been punished hard.

Not much is expected out of 2023 in terms of economic growth, but as I pointed out, the stock market is forward-thinking, so if you believe we could see only a mild recession, then layering into a position of TROW near current levels could prove to be plentiful in the long term.

I have no problem with investors adding TROW here, but for me, already having a position, I would like to grab some more below a 13x multiple like we saw back in October.

TROW is a proven business that will bounce back in a big way when the market turns, similar to how it did back in 2008/2009. The company is backed by a very strong balance sheet and even with lower AUM and revenues, they still generate strong free cash flows to support the business and the growing dividend.