Super Micro Computer: On The Leading Edge (NASDAQ:SMCI)

mesh cube

Super Micro Computer (NASDAQ:SMCI) is an IT solutions company that offers server solutions that are optimized for high-performance computing (“HPC”) and artificial intelligence (“AI”). Within the semiconductor/computing ecosystem, you can think of SMCI as an infrastructure company. There are numerous players across the ecosystem, like ASML (ASML) in lithography machinery, TSMC (TSM) in chip manufacturing, and Nvidia (NVDA) in chip design. Then there exist REITs that own the properties that host servers. Finally, there are companies that build computers and servers themselves, and this is exactly what SMCI is. As we continue navigating the age of AI, quickly incorporating innovations will be increasingly important, which is where SMCI has a distinct competitive advantage.

Demand Drivers for SMCI Products

SMCI’s specialization in HPC and AI computing applications has positioned them well in the middle of two rapidly growing industry trends.

Cloud computing has been all the rage in recent years. A ‘cloud computer’ is just a powerful server that is owned by a specific company. When you are connected to the cloud, you are just sending data from your local device storage to the servers on the cloud for storage. Big tech companies like Google (GOOG), Amazon (AMZN), and Microsoft (MSFT) then rent out or sell storage space on these supercomputers, which are dubbed as ‘cloud computers’. A somewhat recent cloud innovation is ‘cloud clusters’ which refers to hosting multiple cloud computers across different regions. Each region has a ‘cluster’ of computers that serve as local expressways for information similar to the more generalized characterization of the internet as the ‘information highway’. Each of these clusters is synchronized, so if any one specific cluster is down the information held on that cluster is readily available on all other clusters. This innovation in cloud computing provided benefits for data security and computing speeds for end users but drastically increases the requirements for high-level servers capable of storing and processing immense amounts of data. This serves SMCI well within its cloud computing/high-performance computing segments.

AI has taken the world by storm the past few months, with what many are now beginning to call a ‘baby bubble’. Nvidia, one of the foremost benefactors of widespread AI adoption, is trading well above 100x earnings because of the exuberance this technology has caused. From a technical perspective, AI requires huge amounts of computations on data using matrix multiplication. GPUs, or Graphics Processing Units, are specialized for this type of computation. Since Nvidia is far and away the market leader in GPU technology, they have been the subject of a ridiculous frenzy recently, with shares running up over 100% YTD. The biggest issue with AI is that it uses truly huge amounts of power to run current models, which are only becoming more data and energy intensive. One thing is certain in AI: the demand for high-level computational capabilities will continue to increase over time. Again, this space is one in which SMCI is really well-positioned. AI depends both on a really sophisticated chip design and on the leading nanometer wafer fabrication capabilities. Once new innovations in chip design and fab come out, it’s then on companies like SMCI to build computers and servers that incorporate the latest technology and bring this tech to market in a consumable, cost-efficient way.

SMCI offers “Server Building Block Solutions”, which allows them to “quickly assemble a broad portfolio of solutions by leveraging common building blocks across product lines” according to the 2022 Annual Report. SMCI has a simple strategy: to always be the first-to-market with IT solutions that incorporate the newest innovations in the field of microprocessors and chips. This, combined with in-house design and build of servers, allows them to stay positioned on the leading edge of current computing capabilities. SMCI works closely with leading chip design companies to ensure they are aligned with product release cycles and can quickly build new products incorporating these products.

Further, Super Micro offers some of the best energy efficiency within their computing systems mostly because they incorporate the newest chips which seek to both increase computing power and enhance energy efficiency. This makes them a great option for data centers that will be built into the future which will need to meet increasingly strict environmental regulations.

Super Micro also offers products as ‘Rack Scale Plug & Play‘, which allows customers to purchase a fully customizable server rack that is delivered pre-built and just needs to be plugged in upon delivery.

Finally, Super Micro has an impressive amount of published research available on their company site, showing that they are not just a dependent partner of leading chip designers, but are partners in designing some of the leading computers and servers available on the market today.

Valuation

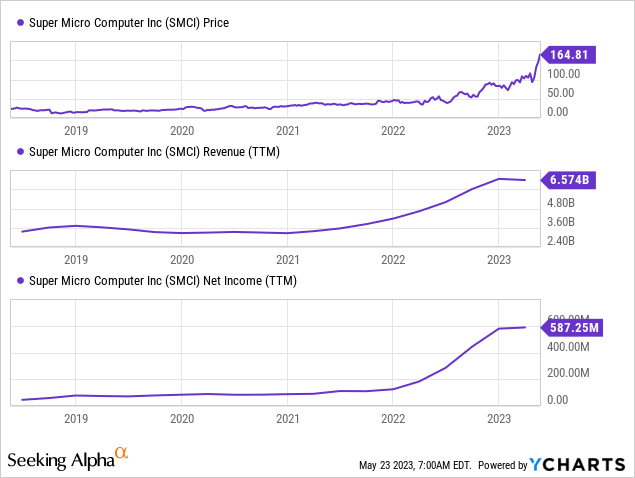

These secular demand tailwinds along with SMCI’s unique position driven by their business model have led to huge growth in revenue and earnings recently and contributed to the massive rally in shares over the past year:

Further, the CEO and founder of SMCI has ambitious growth goals for the future. He is pushing the company along every day to continue executing this strategy and it seems like he truly believes this is the breakthrough moment for his company. In an interview with AMD CEO Lisa Su, the interviewer commented on SMCI’s impressive 50% growth, and Charles Liang responds “Only 50%!”.

SMCI is run by its founder who loves this business and continues to have ambitious growth goals for the foreseeable future.

For my valuation I used a discounted cashflow model using the 2022 reported net income of $578m. My estimated growth is far below management’s estimates, I used 15% earnings growth for the next 3 years, then 3 years of 7% growth, followed by 4 years of 5% earnings growth. With a 15% discount rate and a P/E of 5, I estimate the value of SMCI to be about $278. Using an even more conservative 10% figure for the next three years yields an estimated value of about $244. This rounds out my intrinsic value estimate of $244-$278 for SMCI. At the current level of ~$166, SMCI looks significantly undervalued and could still have more room to run. Although SMCI has been greatly assisted by the AI hype which has driven many AI-related stocks up like rockets, the hype looks real for SMCI. AI applications are garnering mass adoption and many companies are looking to start utilizing AI solutions for their own businesses. This secular uptrend will continue to benefit SMCI well into the future.

Conclusion

Investors usually get spooked by huge price moves in either direction. Seeing a 200%+ rise in a year leaves many potential buyers on the sidelines because they just can’t foresee the price continuing to increase much more than it has already. However, I’m initiating my coverage on Super Micro Computer stock with a strong buy because it has really sound fundamentals and looks like a business that will continue generating really solid value for shareholders over the long term. Further, despite the major run-up in shares in the past year, I believe that consumer sentiment has shifted in a way that majorly benefits SMCI, which should be able to continue growing for years to come.