Rates Spark: Sticking To Their Knitting

Douglas Rissing

By Padhraic Garvey, CFA, Antoine Bouvet, Benjamin Schroeder

US 10yr auction today is a key barometer for direction in the coming weeks

It will be intriguing to see how the US 10yr auction goes today. The 3yr auction yesterday saw stellar demand, but that is to be expected, as that’s a value part of the curve given the extreme inversion. The 10yr is a different proposition. It requires investors to believe that market rates are set to fall, else why not buy shorter dates at a higher running yield?

We also think that the run of cash into money market funds over the past number of weeks, and continuing in the first weeks of 2023, is not indicative of a marketplace that has a big demand to take down duration. Quite the opposite, in fact; it’s a marketplace that prefers the higher running yield offered by the front end, and the shorter on the curve the better.

In fact, if you go short enough on the curve, that’s where there is minimal price risk, and it comes with maximum running yield. The 10yr auction today will be a great test of appetite at current levels. The concession built yesterday should help to rescue demand, but it’s an open question as to whether that will be enough.

In fact, the backup in yields makes the test even sterner – any hiccup at today’s auction bodes very poorly for Treasuries in the coming weeks. Let’s see…

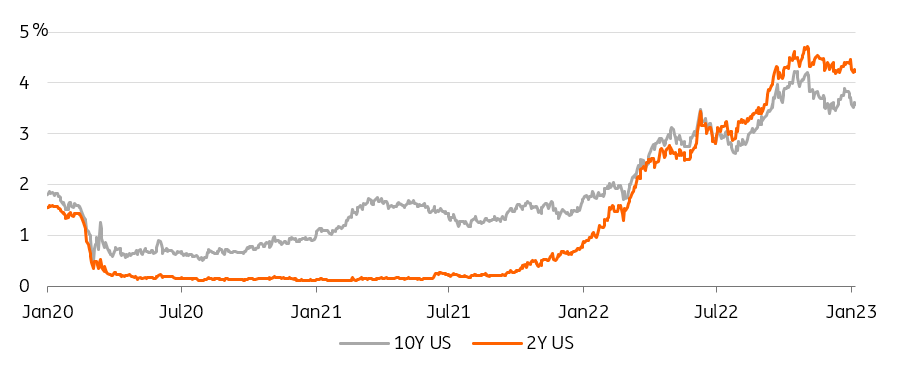

Higher Yield And Lower Risk: Short-End Debt Is Increasingly Popular (Refinitiv, ING)

Supply, not central banks, is what’s keeping bonds up at night

Contrary to our (misguided) expectations, the Riksbank symposium did produce prepared speeches by its participants. These, however, contained little, if anything, by way of relevant policy hints. It was interesting to contrast Fed Chair Jerome Powell and European Central Bank Bank (ECB) executive board member Isabel Schnabel’s take on the role of central banks in the green transition. The former presented a short exposé explaining why it lays squarely outside of the Fed’s responsibilities. The latter favours a much more activist approach at the ECB. Luckily, it turns out the best the ECB can do to support the green transition is promote price stability. The upshot in both cases is that markets didn’t have much to worry about coming from this event.

Today’s central bank speakers list (see events section) is heavily skewed towards ECB speakers. The tone has been overwhelmingly hawkish of late, so officials stand a better chance to move the market in case of dovish comments, in our opinion.

No euro sovereign deal today in Europe to push rates higher

It seems that after days of blissful ignorance, bonds noticed the wall of supply about to hit primary markets. The difference with previous days was two large euro sovereign deals (10Y from Belgium, 20Y green from Italy), presumably without swap hedges to dent the duration impact. This theory comes with two caveats. First, dollar-denominated bonds actually sold off more than their euro peers despite sovereign supply occuring later in the week, namely today and tomorrow. Second, Italy outperformed other euro sovereign despite seeing the largest deal in duration terms. No euro sovereign has mandated banks yesterday, so we assume the lack of deals today mean a more constructive session for bonds.

Only sterling bonds escaped the generalised wave of selling, thanks to strong demand at the Bank of England sale. The Bank sold £5.3 billion of the long-dated gilts it bought in September/October for financial stability reasons. Gilts still face BoE sale operations today (unwind of financial stability portfolio) and tomorrow (sale of quantitative easing portfolio).

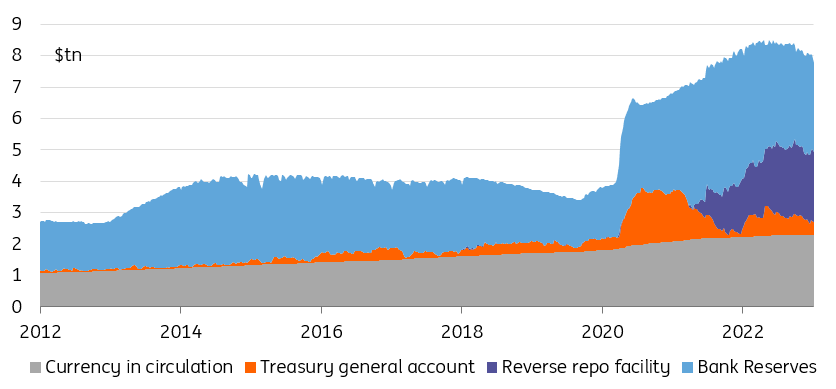

A Reduction In The Treasury General Account Would Offset The QT Liquidity Drain (Refinitiv, ING)

US liquidity neutral for Treasuries until the debt ceiling is lifted

The US Treasury upsizing its T-bill auctions means the federal government is one stop closer to the $31.4 trillion debt ceiling – $69 billion close, to be precise – according to Bloomberg. The Treasury reducing net issuance until the ceiling is lifted, something that could take some time if the vote for House speaker is any guide, means it will soon have to run down the Treasury General Account (TGA). The resulting injection in liquidity in the system, all else being equal, could go some way toward dampening the liquidity draining impact of quantitative tightening. This, in turn, would be another supportive development for Treasuries.

Today’s events and market view

There is a long list of ECB speakers today, including hawks such as Robert Holzmann and Francois Villeroy, and historical doves such as Olli Rehn and Luis De Cos. It is usually dovish comments from hawks or hawkish comments from doves that have the most market-moving potential. We came out of the December ECB meeting with the strong impression that the hawkish shift in policy was widely supported. Any comments contradicting this would be most surprising to markets, especially if emanating from hawks.

Economic releases are few and far between. They consist of Italian retail sales and US mortgage applications.

Germany will launch a new 10Y benchmark for €5 billion. The US Treasury will auction 10Y T-notes.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.