QQQ: Buyers Show The Way (NASDAQ:QQQ)

bunhill

The Invesco QQQ ETF (NASDAQ:QQQ) has continued its outperformance against the S&P 500 (SPX) (SPY) through its recent February highs, defying the “bubble” calls by QQQ bears.

We highlighted in our early December article arguing why outperformance could be “around the corner.” We added in our January update suggesting why QQQ’s recovery wasn’t over yet.

With the surge since QQQ’s lows in late December, a period of consolidation and profit-taking should be expected. Accordingly, the QQQ was up more than 20% from its late December bottom through its February highs.

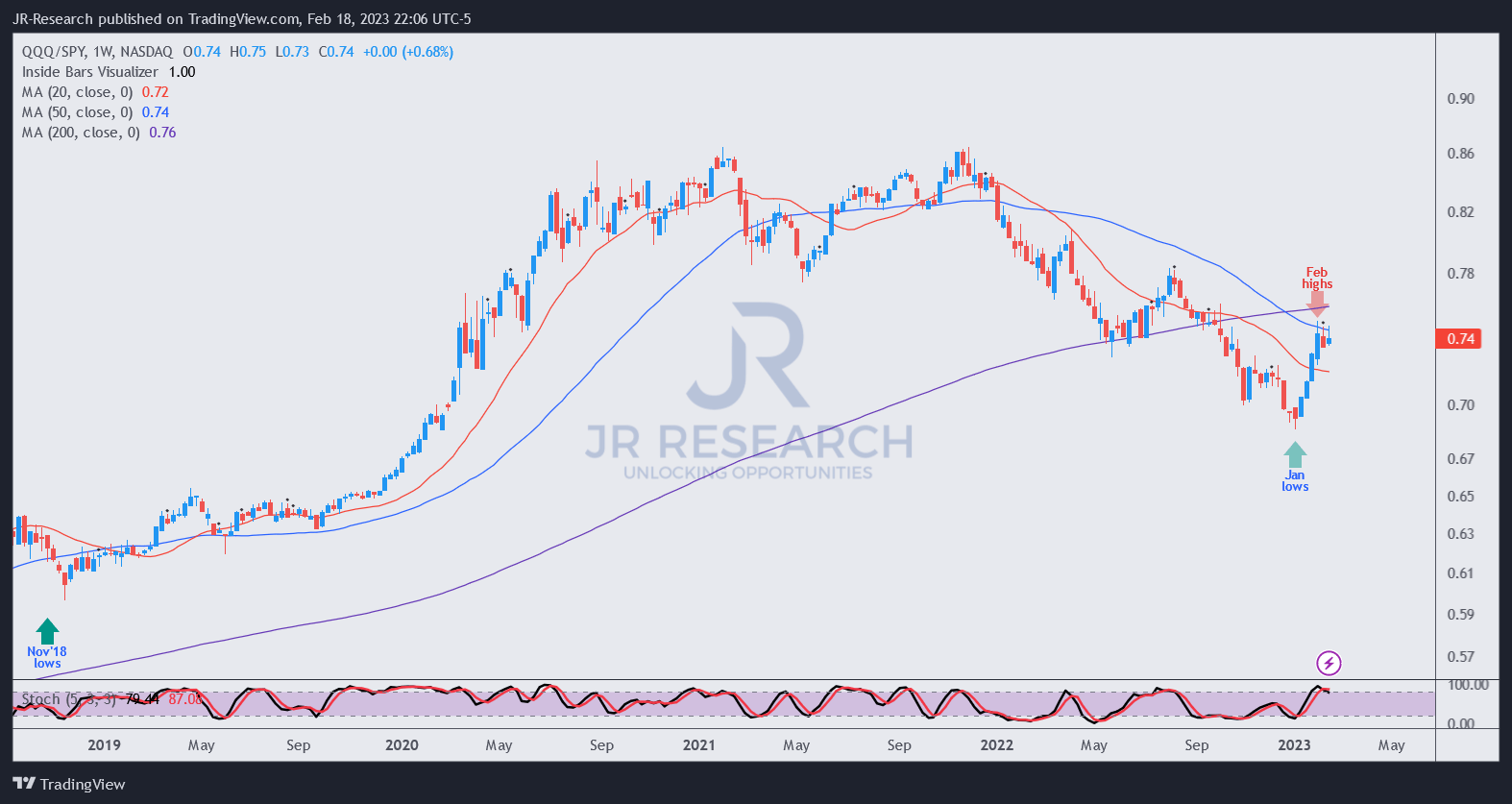

QQQ/SPY price chart (weekly) (TradingView)

As seen above, the QQQ/SPY re-tested a critical resistance level based on its 50-week moving average (blue line) or MA after a rapid surge. Hence, buyers joining the recent buying frenzy must be cautious about bottom-fishers looking to cut exposure.

Does it make sense? Our analysis suggests that the QQQ likely formed its long-term bottom in October 2022, further corroborated by the robustness of its late December lows. Hence, the bearish case seems to be weakening, but it doesn’t mean the QQQ will recover in a straight line.

Investors contemplating adding exposure now need to consider several factors that could impact the bullish case, causing weak buyers to bail out and expecting further downside risks.

The Fed could be prodded to tune up its hawkish tone, as the recent CPI and PPI print showed that the Fed’s inflation fight is far from over. Commentators also suggested that the path toward its 2% price stability goal will be highly challenging and filled with bumps. We also noted commentaries arguing why the Fed could be compelled to lift its inflation target toward the 3% to 4% range.

However, that seems unlikely, as it could cause significant damage to the Fed’s credibility over the long term. Hence, the need to stay consistent with its messaging could lead Fed policymakers to consider a 50 bps hike if it intends to move faster toward its inflation target.

Hence, the critical question is whether the market has priced in a more hawkish Fed?

Accordingly, interest rate futures have already moved upward, reflecting a “57.5% probability of a peak [rate] of at least 5.25% to 5.50% in June.”

Therefore, to say that investors have not taken note and reflect a more hawkish Fed is not appropriate.

Also, retail traders have not gone into FOMO mode. Instead, recent data suggests that retail traders are still pessimistic. Accordingly, “the jump in activity can be due to many factors, most of which have nothing to do with speculation.”

Notably, the retail-only-buy-to-open or ROBO Put/Call ratio “is above where it was at every single major peak in the S&P over the past 23 years.” As such, calls suggesting that retail investors/traders have engaged in highly speculative activity recently don’t align with data-driven insights.

Also, it’s critical to note that money managers had already shifted away from a highly pessimistic positioning at the end of 2022 toward a more neutral stance. Therefore, money managers are likely not expecting October lows to be broken down further, even as a healthy consolidation phase could follow.

The tech sector is important, which accounts for nearly 50% of the QQQ’s weighting. Hence, tech’s continued recovery will be pivotal toward QQQ’s retaking its uptrend bias subsequently.

Investors need to note that tech’s (XLK) outperformance against the SPX in the early stages of a new bull market is not surprising. Accordingly, “technology typically outperforms in the early stages of a new cyclical advance.” Moreover, if investors have a high conviction of the QQQ’s October lows, they should not be concerned with an impending pullback, as the 10Y Treasury yield is on an uptrend continuation pattern. As such, near-term downside volatility should be expected, offering investors on the sidelines another opportunity to pounce on weakness.

Backtesting data suggests that the NASDAQ (NDX) is back on a risk-on environment but doesn’t coincide with excessive speculation, as discussed earlier. Hence, it corroborates our price action thesis that we are still in the early stages of a sustained market recovery.

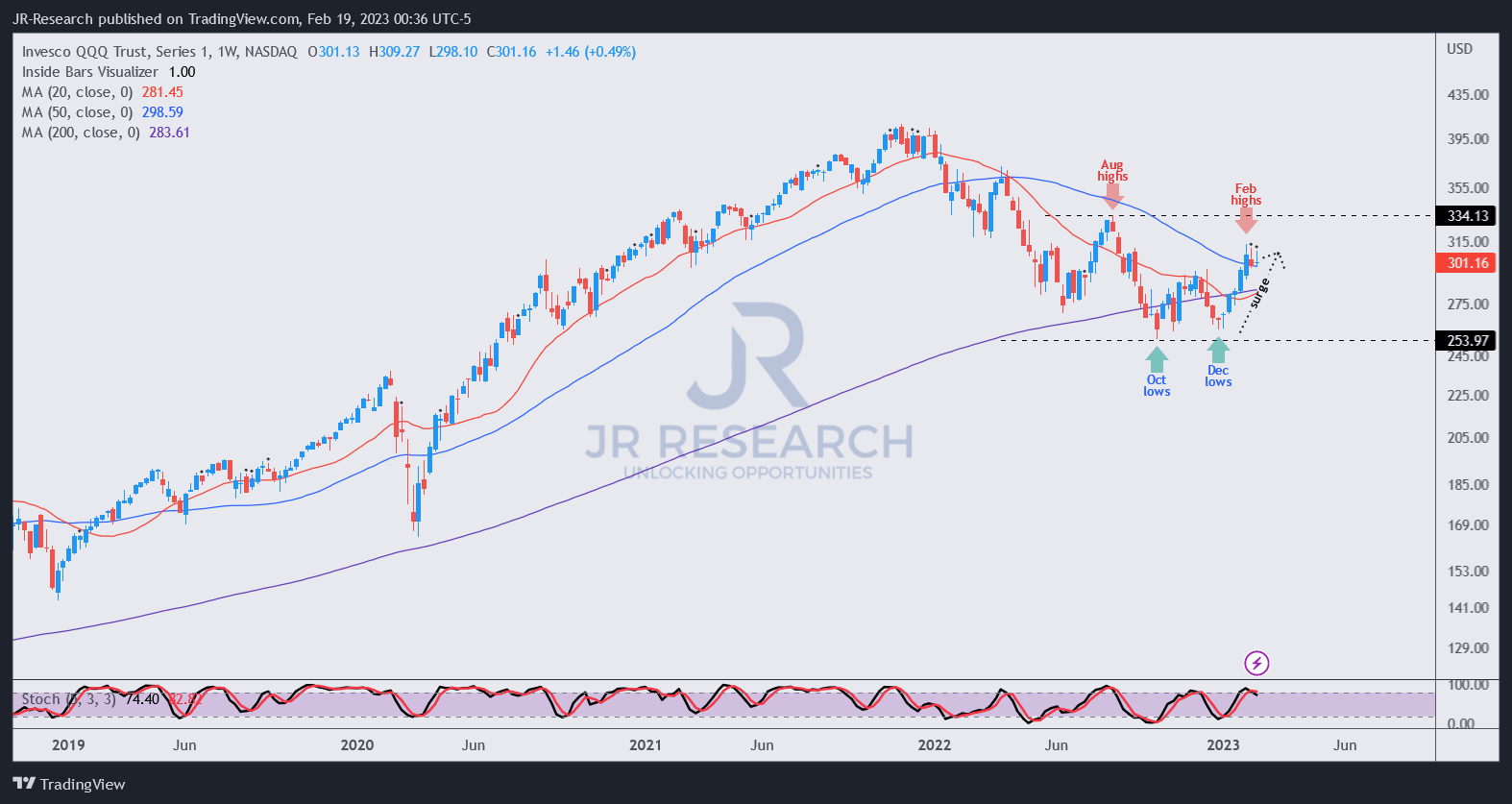

QQQ price chart (weekly) (TradingView)

Breakout traders/investors need to be cautious about anticipating a firm upside breakout, as we think a pullback from the current levels looks more likely.

Coupled with overbought momentum, corroborated by the surge in the 10Y yields, a pullback will also help to shake out some weak buyers who chased the recent momentum, which stalled in early February.

As the QQQ ETF remains in a medium-term downtrend, trend-following investors are likely still on the sidelines, waiting for the “golden cross” before emerging from their hiding to participate in the recovery. We believe it also explains why the media remains pessimistic over the recent broad market recovery, as the Fed is still expected to be hawkish.

However, investors must always remember that the market is forward-looking. With interest rate futures already pricing in a more hawkish Fed, the next pullback will likely provide more clarity on the subsequent buy levels to add exposure.

But we don’t expect October lows to be breached, so we encourage investors to buy confidently on its next retracement.

Rating: Hold (Revise from Buy).