PSLV: The Perfect Storm Is Brewing

Bet_Noire

Silver made the top headlines in the beginning of 2021 in relation to the short squeeze attempt triggered by users of a certain financial forum. Since then, the metal has been hovering around the US$20/oz mark with no signs for a major breakout. Meanwhile, on the physical market for silver, a perfect storm is brewing on the back of rapid demand recovery and supply challenges. In such an environment, an exchange-traded fund (“ETF”), tracking the commodity, could offer investors direct exposure without assuming the operating risks of a miner. The Sprott Physical Silver Trust (NYSEARCA:PSLV) offers just that and trades at around a 3% discount to its NAV.

Rapid demand recovery

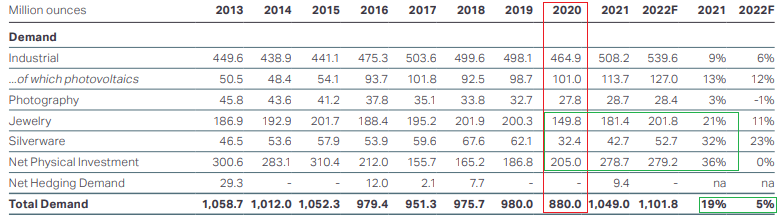

For the past 7 years prior to 2020, silver consumption was fluctuating around the 1B ounces mark. As the world was hit by the pandemic and the subsequent lockdowns, total demand fell 10% YoY mainly on sharp reduction of jewelry and silverware related consumption. The only category that registered an increase in 2020 was investment-related demand, which indicates that some investors see the metals as a safe-haven in turbulent times.

Silver demand (Metals Focus)

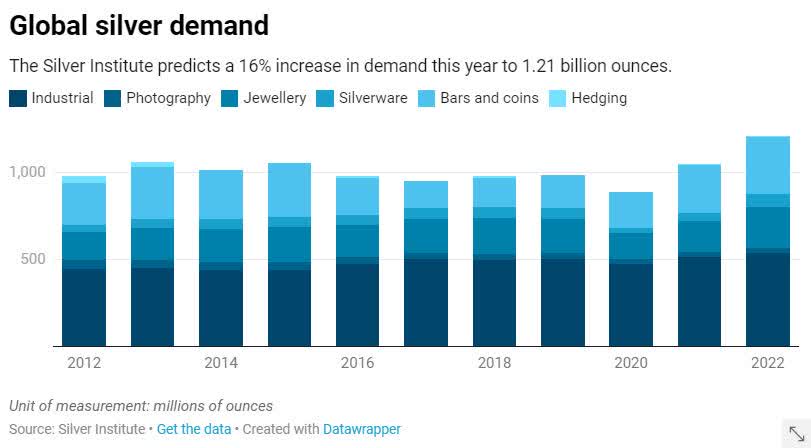

In the subsequent two years, the recovery in demand was impressive, as in 2021 a 19% YoY surge was registered, while a 5% YoY increase is projected for 2022. This will put total demand for silver beyond the 1.1B mark, hitting a record level. It has to be noted that the driving forces behind the rally were mainly industrial and investment demand, while jewelry and silverware have recovered to their pre-2020 levels.

Global silver demand (Silver Institute)

Growing “green” usage of silver?

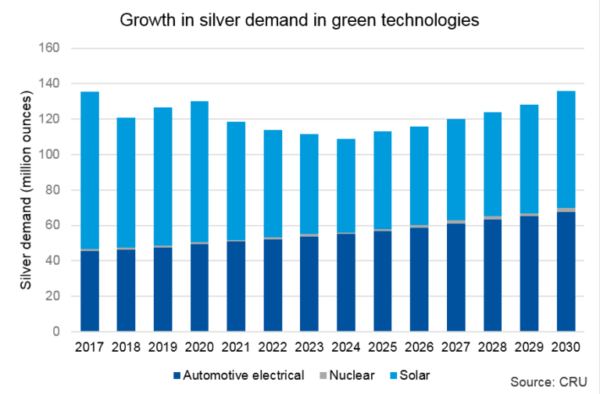

Silver is being used in the energy transition of the world as part of photovoltaics. However, the potential for consumption growth from this submarket seems exaggerated. While it’s true that solar panels are a growing part of the energy mix, due to technological advancement, the amount of silver used in solar cells is shrinking year after year. The two effects mostly balance out, and as a result, the silver demand as part of photovoltaics is not expected to be a source of rapid growth in the consumption of the metal.

“Green” demand for silver (CRU Group)

India – a rapidly growing market

Precious metals have been deeply embedded as part of the Hindu culture. It’s believed that jewelries enhance the beauty of a bride, therefore, they are an important part of wedding ceremonies. Understandably, gold is the first choice, but its relatively high price makes it unaffordable for some families in India, so silver comes at the rescue.

Silver imports into India (India’s Trade Ministry; Bloomberg)

Following the lockdowns in 2020 and 2021, weddings in the country are on the rise, and so is the demand for silver. According to the latest projections, the imports of the grey metal into India are projected to reach record levels in 2022, surpassing 8k tonnes.

Supply challenges

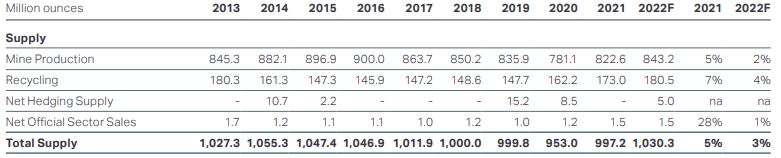

While demand is rapidly expanding, the same couldn’t be said about supply. For the past ten years, supply has been pretty much flat at a bit above 1B ounces per year, with over 80% of it being mine production, while recycling accounts for less than 20%. While supply fell in 2020 as some mines faced operational challenges, it has recovered in 2021 and 2022 to its pre-pandemic levels. However, the “speed” of recovery is considerably lagging behind demand expansion.

Silver supply (Metals Focus)

There are technological reasons for this. Silver is primarily a by-product from mines, where another metal – usually gold, copper, lead or zinc – is the main ingredient of the ore. So the driving force behind potential increase in silver supply should be more mining of other metals. Mining itself is a difficult business as it is capital intensive, while permitting and construction of a mine takes multiple years, especially in developed countries. To make matters worse, one of the biggest producers of silver have been hit by operating costs inflation, reducing their free-cash flow, hence the ability to invest in production expansion.

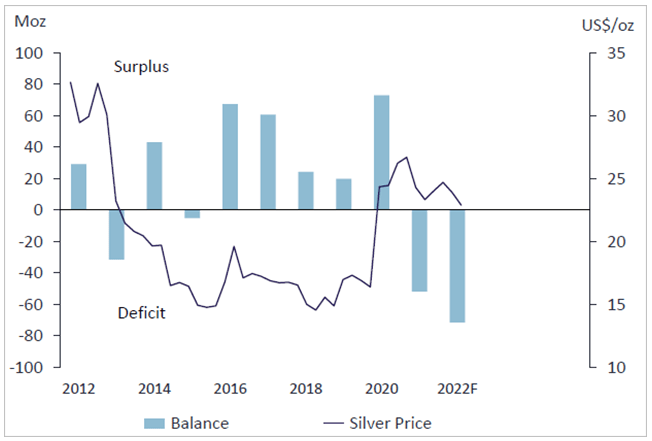

The market balance

Silver market balance (Metals Focus)

The end result of the supply/demand dynamics is a deficit on the silver market, which could become a lot worse in the coming years, as supply growth from mining is constrained. While the existing jewelry and silverware could be a source of secondary supply, probably a lot higher market prices are needed in order to incentivize this secondary source to come to market. This makes the long silver thesis a logical conclusion.

Why PSLV?

As already established, pure-play silver producers are very rare, so through equity an investor will most likely be exposed to a plethora of metals. Furthermore, miners face additional risks like operational risk, exploration risk, permitting risk etc. Alternatively, a direct exposure on the metal could be obtained through futures, but more often than not, they’re “paper” contracts with no real metal behind them. The data indicates, that only one in 250 “paper” ounces of silver is backed by the physical metal. For that reason, in order to further de-risk their exposure, some investors prefer physical exposure to the metal. But holding silver in your home is not convenient, especially for larger quantities, given that the metal is quite spacious. This is where ETFs like Sprott Physical Silver Trust come into play.

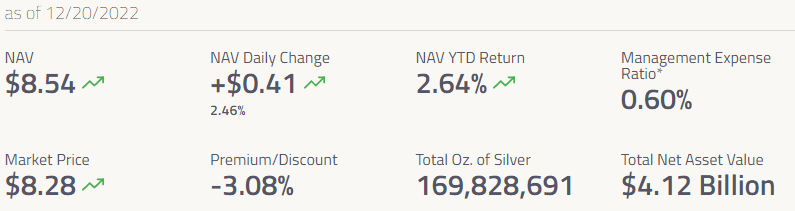

PSLV highlights (Sprott)

While it’s smaller in assets under management (“AUM”) and has slightly higher fees than its main competitor – the iShares Silver Trust ETF (SLV) – PSLV has some advantages as well.

Firstly, it trades at a 3% discount to NAV, while SLV is currently priced at a premium of about 1.8%. Secondly, PSLV uses the Royal Bank of Canada as a custodian, compared to JPMorgan Chase & Co. (JPM) for SLV. Given that the investment bank has been involved in precious metals manipulation schemes, some investors will likely be more confident in the Royal Bank of Canada safeguarding their investment. Last but not least, PSLV has an established procedure for physical redemption of the shares an investor holds, as long as they equate to more than ten 1000oz silver bars.

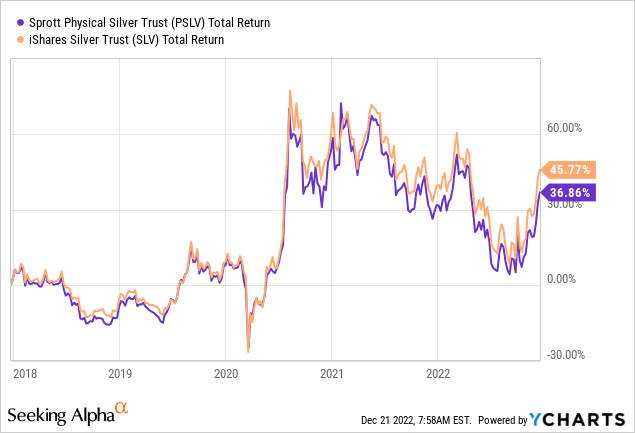

For the sake of being objective, I have to stress that in longer time frames, SLV tends to outperform PSLV with one of the reasons for this being the lower fees that it offers. In the end, choosing between the two ETFs is a matter of priorities – a slightly lower risk profile, the option for physical redemption and discount to NAV, compared to better historical performance and vice versa.

Risks

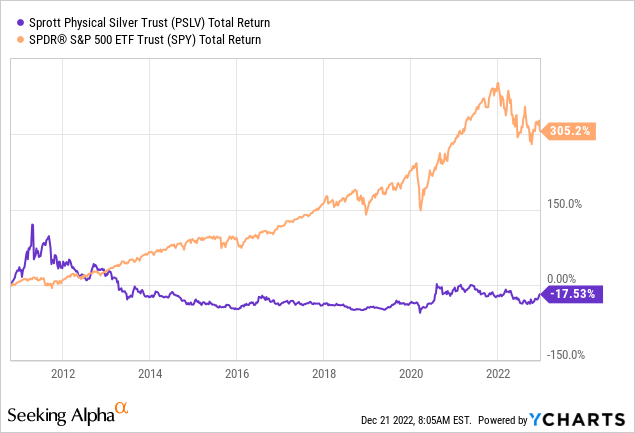

While the nature of PSLV makes bankruptcy risk pretty much non-existent, market underperformance is the biggest treat. Historically, silver has been quite volatile and the upward moves have been pretty rapid in short time frames. However, on a longer time frame, the broad market seems to be yielding better returns. That being said, I think that given the current supply/demand dynamics on the silver market, a significant move to the upside for Sprott Physical Silver Trust may be coming.