ProFrac Holding: For Those About To Frac (NASDAQ:ACDC)

AC/DC Performs At Dodger Stadium Kevin Winter

Introduction

ProFrac Holding Corp. (NASDAQ:ACDC) is in the business of providing pumping and ancillary services to the U.S. fracturing industry. It has grown rapidly through acquisitions and is now one of the top 2 or 3 competitors in the frac segment of the OFS space.

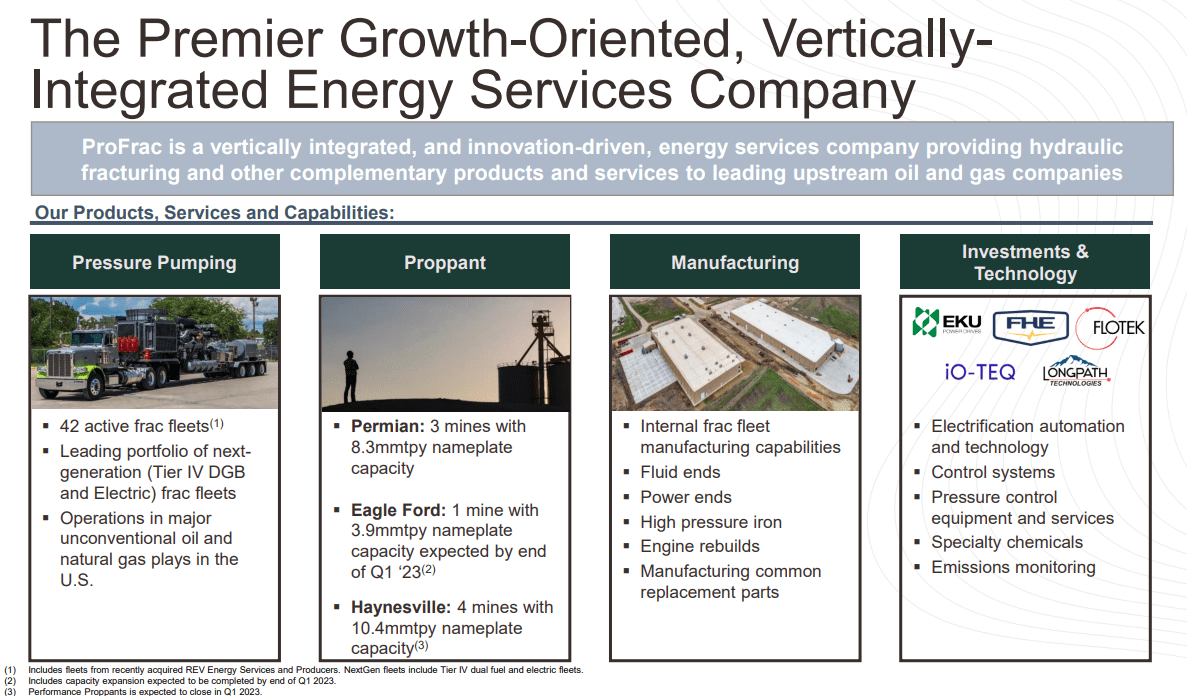

The slide below shows the company as exists today. Some recent ProFrac M&A activity isn’t shown and should be noted. In 2022 they bought U.S. Well Services, and just in Jan of 2023 they acquired Rev Energy Services.

ProFrac Integration (ProFrac Holdings)

In this article we will review the fundamental business case for ACDC and look at a possible new play that could drive earnings in 2024 and beyond. If shale production is to be maintained, fracking has a long run ahead of it. ProFrac has positioned itself to be a star in this space.

I think risk tolerant investors should take a careful look to see if a company like ProFrac meets their investing objectives.

The thesis for ProFrac Holding

The Wilks family knows when to hold ’em and when to fold ’em. You may not be familiar with them, but they first blazed a trail across the oil patch firmament with Frac Tech-FTS, in 2002. In 2011, far ahead of the mid-2014 oil crash they cashed in their chips, and sold the company to a Singaporean investment house for $3.5 bn. A few years later they bought back the remnants of FTS and merged with another struggling fracker – ProFrac Holding – started by Dan and Farris Wilks in 2016, and began to rebuild their oilfield empire. Bit by discounted bit.

With about 1.6 mm HHP in the field, ACDC today is one of the largest and certainly the most vertically integrated pumping company pushing sand into the earth. With 22.5 mmtpa nameplate capacity across three major basins, they are also one of the largest sand suppliers. Being able to deliver this product internally is a value added item for customers, and for ACDC (I swear I am going to have to dust off the old AC/DC rock catalogue as I finish this article), is a win as well.

Supply chain is another area where ProFrac has developed some internal capacity that helps it maintain, and add to their inventory as needed. Particularly in the area of efleet, of which they will have 5-on the ground this year. Some of their other investments are noted in the slide above at the extreme right. All of them have something to do with improving processes, controlling emissions, and in the case of Flotek (FTK) (subject of another article) is attempting to impact the ease of production from the well.

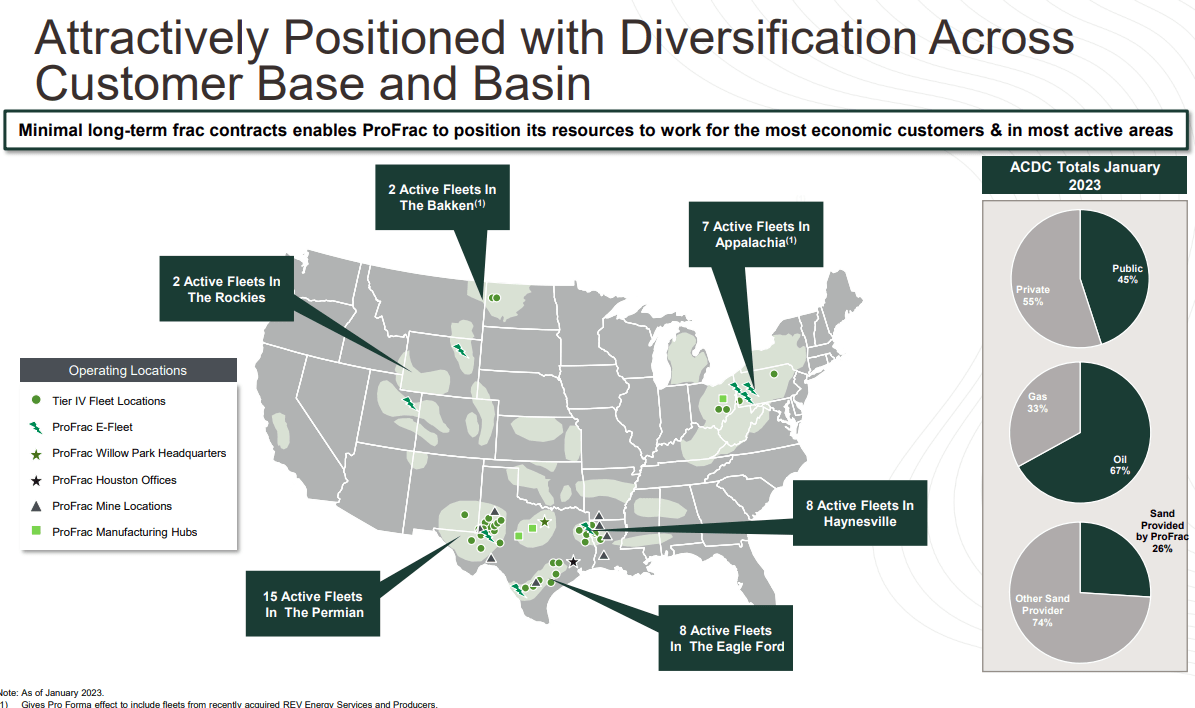

ProFrac Diversification (ProFrac Holdings)

The bottom line for ACDC is with its vertical integration and footprint in key shale basins; the Permian, Eagle Ford, and Haynesville in particular, is primed to do well. ACDC CEO Ladd Wilks comments on the importance of vertical integration to their strategy:

Vertical integration allows us to capture more share of our customers’ completions budget and this is a priority for ProFrac as we believe it represents our largest topline growth opportunity in 2023.

(Source)

A Possible Catalyst for ProFrac in 2024-5

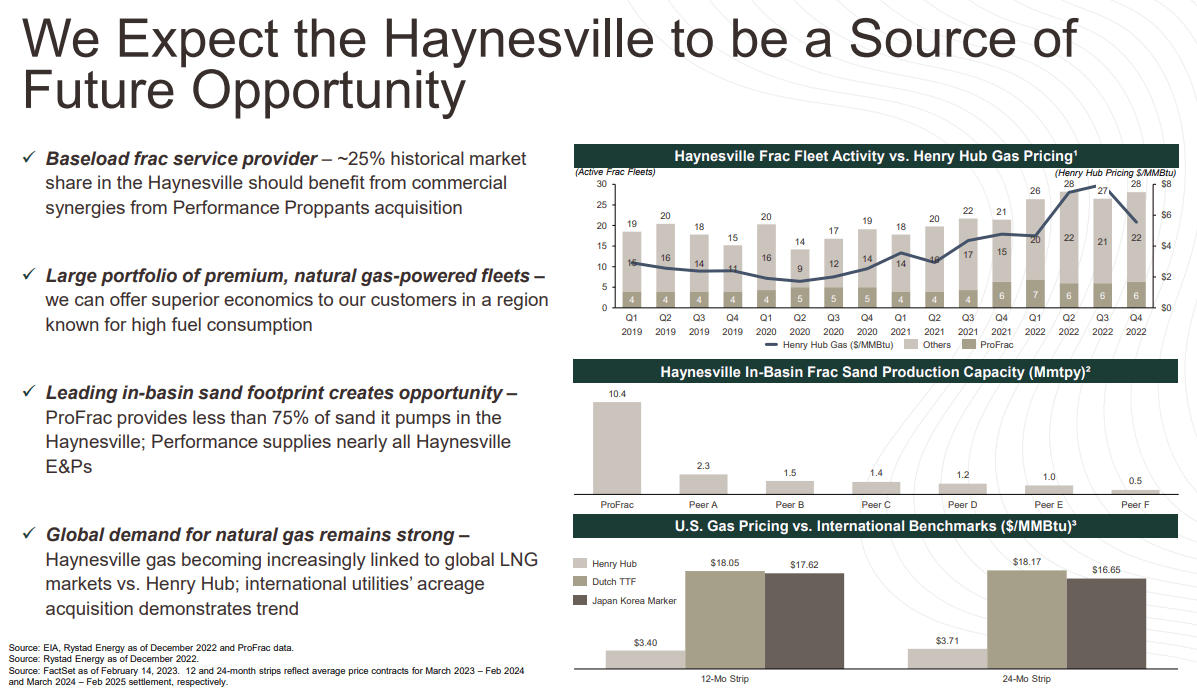

I think the Haynesville, which is currently dialed back a bit due to its gassiness, will experience a resurgence in the time frame I mention in the heading. The reason of course will be new LNG capacity hitting the market and needing feedstock. There’s another reason, the Haynesville could be experiencing growth from an enhanced resource. Comstock Resources (CRK) has made a couple of barnburner wells, 100 miles to the west of existing Haynesville production. (This will be discussed in a future article on Comstock) New discoveries like this can stimulate an increase in drilling as other operators delineate the new field extensions.

Now you may say, “That’s great for Comstock, but what does it have to do with ProFrac? Permeability.

The Haynesville is tight. Really tight. These reservoirs are low porosity-~5%, with almost non-existent matrix permeability-measured in nano-Darcies. For those who are new, a Darcy is measure of the ability of rock to permit fluid flow. Often measured in milli-thousands, of a Darcy, micro-millionths, or nano-one billionth of a meter. Like I said, the Haynesville is tight.

In order to inject some permeability into the rock frackers are pumping between 3-4,000 pounds per foot. This compares with the 2-2,500 ppf common in other basins. It should be obvious now, that ACDC will realize about 30% more sand sales in this basin. More sand also means, more pumping and more stages. All revenue generators for a pumping company, as we mentioned in the central thesis for ACDC.

ProFrac Haynesville Opportunity (ProFrac Holdings)

We haven’t yet addressed what contributes to the “tightness” that characterizes the Haynesville. There are a couple of reasons. The reservoir itself is comprised of silty, argillaceous-clayey, mudstones contain more than 30% silt-sized siliceous grains. The silt often occurs as laminations within these mudstones. In addition, the argillaceous matrix of such mudstones frequently contains numerous calcareous particles and stringers. The calcareous particles include coccoliths, bivalve, and gastropod fragments, and calcispheres. All of this results from a thermal-pressure related, rock-maturation process called, Diagenisis. But that’s not the end of the story.

The sedimentary depositional environment also played a role in determining the tightness of the Haynesville. This was a restricted-shoaly, shallow marine basin that allowed for very fine granular packing of the carbonate fossil sediments, along with the aeolian (wind-driven) clastic particulates. The restricted access to this basin created an anoxic environment for the plantonic goo that coated these particulates as they settled, and allowed them to be preserved and incorporated into the sediments as they became more deeply buried. Plantonic organics are strongly associated with the development of gassy hydrocarbons.

So what does all of this have to do with ProFrac’s opportunity in the modern-day Haynesville? Quite a lot actually, or I wouldn’t have bored you with the geology lesson. When you begin pumping sand into a formation like this, the first thing you pump is chemistry. Chemistry-acids, to break down the clays lining the pores of the mudstone, and solvents and surfactants to minimize emulsions, and reduce friction. (When you are pumping sand at 3,500 ppf, you are pumping at 40-50 bpm and friction reducers are necessary to keep the hydraulic window open.) And, of course the vertical tie-in there is with Flotek. (We will discuss Flotek in a separate article.)

Q-3, 2022 and Guidance

ProFrac grew revenues 3.5X to $696 mm in the quarter, from the prior year, and 15% from the prior quarter. EBITDA grew 5X to $248 mm from the prior year and ramped 66% from the second quarter’s $165 mm. As we go into the 4th quarter with 31 active fleets, ACDC was reporting EBITDA of $34 mm per fleet. Net LT was ~$650 mm after absorbent USWS and issuing 12.9 mm share of ACDC to their shareholder. Liquid stood at $249 mm consisting of cash and availability on their ABL.

Management was a bit opaque about the prospects for the 4th quarter of 2022. We can draw some conclusions about this from companies that have already reported.

As we look into the fourth quarter, as Ladd mentioned, pricing continues to remain strong.

As we incorporate the fleets acquired in the U.S. Well Service acquisition, we expect some fluctuations in our per-fleet profitability metrics. Activity levels and more importantly efficiency levels have started strong, but visibility into November and December is opaque. That being said, we expect incremental improvement to our third quarter revenue with the higher fleet count as we add the U.S. Well Services fleets into our operations.

(Source)

Risks

Based on TTM financial results the case for buying ACDC at $14.00 per share is pretty strong. We have to balance that backward looking view against the market rumblings we are now experiencing. Oil and gas are in a rout presently, and sooner or later that is going to show up in North American activity. Rigs will go down. Frac spreads will go to the yard.

It’s not the fault of the oil market per se. There is a crisis of confidence in the banking system, thanks to recent events that is spilling over into nearly every market sector. If you are a Seeking Alpha member, you know this, so I won’t belabor the point further.

The bottom line here is, although current pricing is a great entry point for ACDC, until we get a catalyst to move oil back into at least the upper $70’s, the company could be dead money. It will come, but patience might be needed. Or it could happen next week.

Your takeaway

I think ACDC makes a strong ownership case at present levels. With its footprint, self-sourced consumables, technology, and fleet makeup, at current WTI prices the company has every expectation of growing revenues and profits in 2023. As we move into 2024, the catalyst I mentioned in the Haynesville should come into play. In that scenario, I can see the stock price for ACDC moving higher toward analysts’ estimates.

Clearly at this point, the market is not valuing companies like ACDC as generously as the analyst class, which has a buy rating on the stock and a price range of $25-39. No surprise there, given the general dour outlook the market has for OFS companies at the present point, thanks to the wishy-washiness of oil and gas prices these days. The market is overlooking the tremendous field in which they have to run and there’s just not much we can do about it. Except, take advantage of this extra price drop and scoop up some shares of the company.

When the worm turns, as it eventually will, ACDC will shine.