Premier Stock: Cost Restructuring Key To Driving Value (PINC)

naphtalina/iStock via Getty Images

Investment Summary

The investment case for building broad exposure to a diversified basket of healthcare securities continues to strengthen in FY23′. Since my last publication on Premier, Inc. (NASDAQ:PINC) in December, titled “Premier Makes Sense at 8.75% trailing FCF yield” the stock has pushed sideways into congestion and hasn’t managed to catch a strong bid. Looking at the company’s latest set of numbers, in my estimation, the buy thesis is still intact when extrapolating the data. The stock is attractively priced at 12.8x forward P/E and trades at a discount to the sector, whilst presenting with a 9.2% trailing FCF yield, and despite incurring headwinds to growth in its Remitra segment, management has not embarked on a cost restructuring to free up liquidity and align resources with its divisional growth strategy. This report will break down the company’s Q2 earnings to exhibit the forward-looking investment debate, supporting a buy rating in doing so. Net-net, I’m reiterating PINC as a buy, looking for a target of $42, around 29% margin of safety on today’s market value.

PINC: Unpacking the data

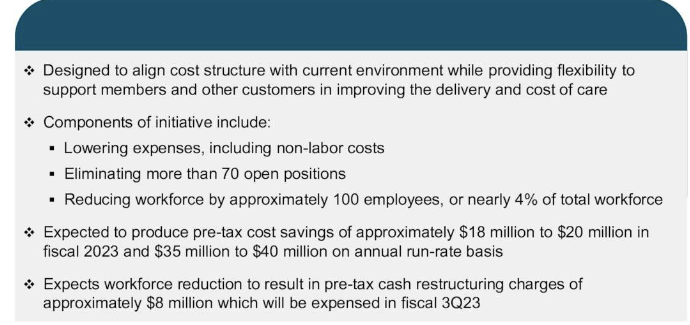

1. Cost restructuring

It’s first important to underline the company’s cost restructuring plans for the coming periods. As mentioned, PINC’s Remitra segment hasn’t performed to expectations and management have pared growth assumptions for the segment looking ahead. As a reminder, Remitra is PINC’s software to streamline compliance, order and payment reconciliation and validation for healthcare providers. Consequently, the company is reducing its capital expenditures to better align resources and hopefully achieve a level of operating efficiency for Remitra. Specifically, it is:

a.) Reducing headcount drastically. Around 4% of its total workforce to be exact, or ~100 employees.

b.) Further, it is cutting non-labor costs by removing >70 open positions. This will impact Remitra as well, as management confirmed it will clip headcount in the business as well.

The company explains the cost-reductions are “designed to position the business to weather the near-term challenges”, and therefore expects $18–$20mm in FY23, eventually saving $35–$40mm on an annualized basis [keep in mind PINC reports FY23 full-year earnings in June].

Fig. (1) PINC cost-restructuring

Data: PINC Investor Presentation, pp. 5

2. Q2 FY23 earnings, key indicators

Now turning to the quarterly numbers, where PINC clipped ~$360mm in top-line revenues, a 500bps YoY decrease on adj. EBITDA of $140.5mm. It pulled this down to earnings of $64mm, down 15.5% YoY. Looking at this in further detail, the divisional takeaways on my end are as follows:

- Supply chain services turnover came in 13% behind last year to $235.5mm, although net administrative fees were 300bps higher. Underlining the fee growth was upsides in the firm’s non-acute purchasing arm. Further, I’d point out further upsides in the company’s GPO portfolio, specifically the foods category, that saw volume growth from more normalized demand and more benign pricing. This includes a normalization of PPE purchasing after the pandemic period has settled. It is important to note, however, that both demand and pricing has pulled back from the highs seen throughout the pandemic. This is understandable, but it could be important for the company to factor in cost-inflation and the propensity to pass-through costs in the wake of this, by estimation.

- With respect to the performance services division, PINC booked a 15% YoY growth to $124mm. Notably, growth was underscored by revenue timing with the company’s license agreements, meaning it may not have been an organic growth schedule. Further, I’d point out the contribution from its Three River Primary Network (“TPRN”) assets that were acquired at the back end of last year. Specifically, PINC acquired these assets for its Contigo Health DTC business. It rebranded the assets as ConfigureNet, and management are projecting a 30–40% YoY growth in the performance services arm as a result of the acquisition. Now, the company can provide access to its network to >900,000 providers in around 4mm locations within the U.S.. As another footnote, the fact that logistics costs have started to pull back to range were a benefit to growth in this segment.

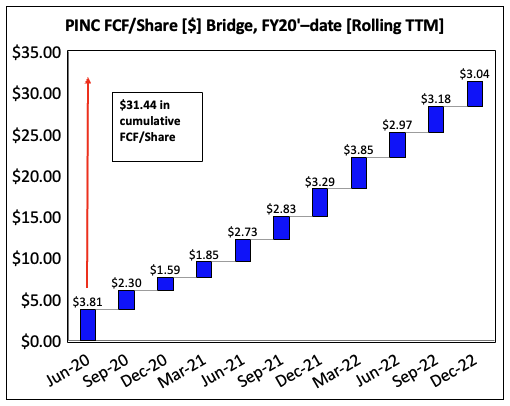

Touching on liquidity and cash flows, the company printed a $109mm quarterly free cash inflow, a $2mm gain from the year prior. I wrote last time that the company realized $55.8mm in TTM FCF so there’s sequential growth at this level, exhibiting the strengths in its bottom-line fundamentals. This arose on the back of a lower CapEx spend on its fixed asset base, and a flat growth in CFFO to $197mm. In further detail, the company has generated accretive value for shareholders in this regard. Looking at a rolling TTM basis, it has generated a cumulative $31.44 in FCF per share since Q2 FY20 [Figure 2]. Hence, the ramp up of FCF/share growth has been notable and serves as a bedrock for investors to recognize the value in this name. This is coupled with a $212mm buyback of stock over the 12 months to date and the cash dividends of $50mm in H1 of its FY23. Hence, the return of capital to shareholders, coupled with the cumulative growth in FCF/share, are supportive of a bullish rating by estimation.

Fig. (2)

Note: Rolling TTM Periods Are Used (Data: Author, data from PINC SEC Filings FY20–23′)

3. FY23 guidance points to strength in performance services

Switching now to the forward estimates, management has revised the breakdown of its FY23 growth assumptions, but has held the outlook firm at $1.4–$1.45Bn at the top-line for the year. The key change comes after it pared back estimates for its supply chain services segment to $980mm at the upper bound, from $1Bn previously. At the same time, it sees $470mm in the performance services arm, up from $450mm at the upper bound previously. The key points, however, relate to where the changes spur from.

- The downward revision in the supply chain services arm stems from a lower outlook on utilization levels because purveyors as currently de-stocking excess inventories that were originally over-stocked due to the pandemic. It sees ~$600–$620mm in GPO net administrative fees as well. Further to this, due to the excess supply levels in the market from inventory management, it sees revenues from direct sourcing product of $285–$315mm, less than the $345mm previously forecast.

- With the upward revision in performance services, it sees growth in the ConfigureNet acquisition, as mentioned, coupled with the cost-savings plan mentioned earlier as well. However, I’d put an asterisk next to the fact that Remitra is still expected to underperform. As such, any surprise to the upside with respect to Remitra would be a welcomed one, and could further justify the company’s restructuring here.

Moving down the P&L, it also foresees FCF conversion at 55% of forecasted EBITDA, calling for $291mm for the full-year. Moreover, it looks to adj. EPS of $2.65, down from a previous high-point of $2.75 previously.

Valuation and conclusion

Chief to the PINC investment debate relates to valuation by estimation. Looking below the bottom line, profitability and free cash conversion are standouts that separate the company from peers, looking at a 25.5% FCF margin and >6% return on capital – both ahead of the industry. Hence, trading at 1.6x book value is attractive, and the stock is priced at ~16x forward earnings on a 9.2% trailing FCF yield. At management’s EPS estimates, I look to an 8% forward earnings yield, well ahead of the S&P 500’s forward number, and an acceptable equity risk premium above the current UST 10-year. Assigning the 16x multiple to management’s EPS forecasts this derives a price target of $42, giving a 29% margin of safety at the time of writing.

Fig. (3)

Data: Seeking Alpha, PINC, see: “Valuation”

Net-net, when extrapolating the data as it relates to investor value, PINC warrants a reiterated buy rating by estimation. Robust FCF/share growth, attractive valuations and the cost restructuring for efficiency are all key supportive factors for the buy rating. I am looking to upside potential to $42, a 29% margin of safety at the time of writing. Hence, I rate the stock a buy.