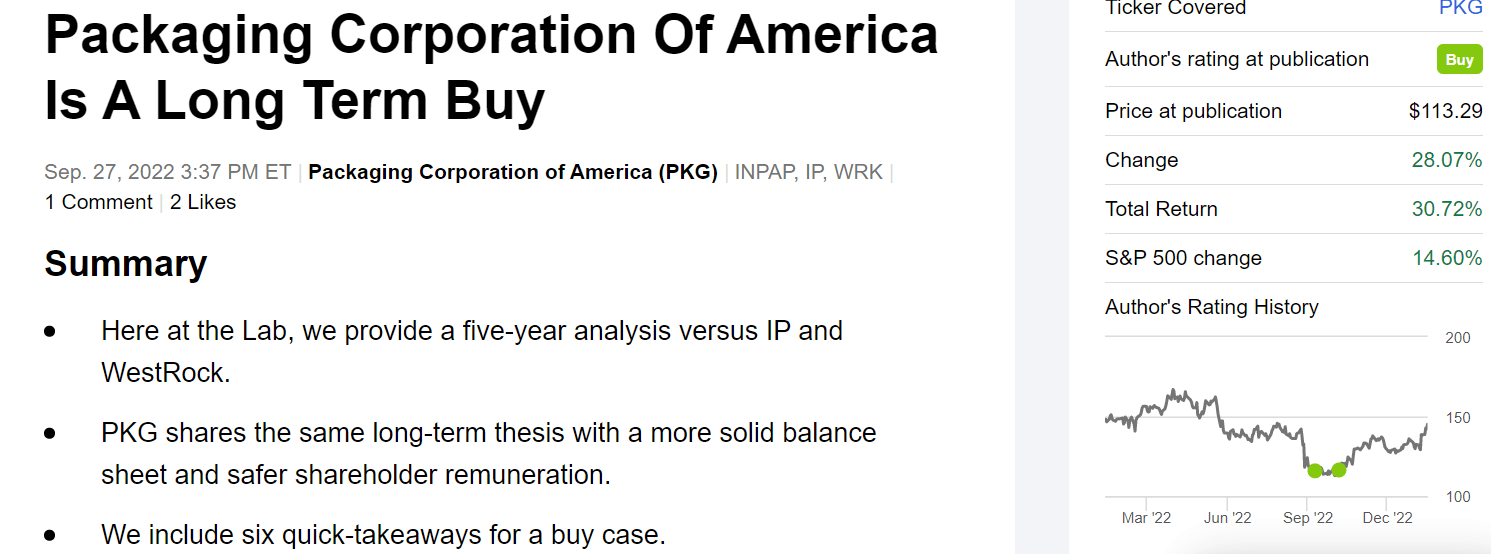

Packaging Corp. Of America: Solid Numbers, Reiterate Buy

malamus-UK

Our readers know that we very much like paper companies. Following our follow-up note on WestRock (WRK) and International Paper (IP), today we are looking at Packaging Corporation of America (NYSE:PKG). In our initiation of coverage, we provided a 5 years’ comps analysis in our US universe coverage, and we recognized PKG as the clear paper market leader. As a reminder, we emphasized how Packaging Corporation of America, out of the three companies, has always been the most resilient. Last time, with we took advantage of a negative note from Jefferies and the FedEx (FDX) profit warming, initiating the company with a clear buy. Supported by the Q3 results analysis, PKG delivered a solid stock price appreciation, outperforming the S&P 500 return; however, the company is still trading at a 10% compared to Mare Evidence Lab’s buy rating target.

Mare Evidence Lab’s previous publication

Q4 Results analysis

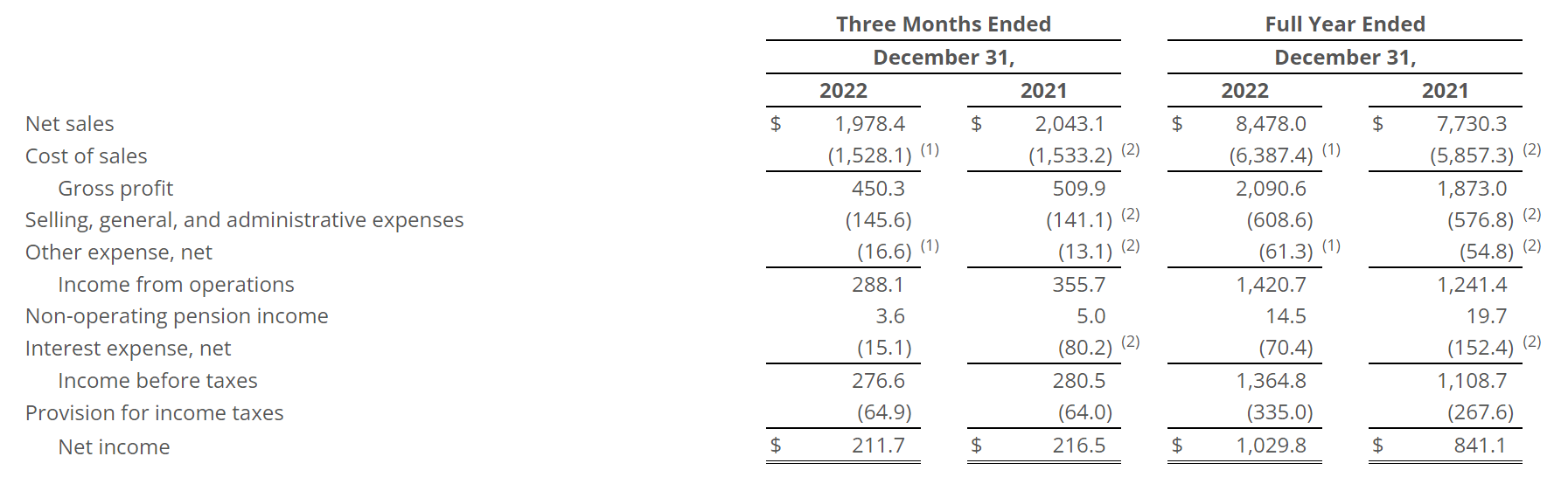

Q4 top-line sales reached $1.98 billion and were slightly down compared to the previous year’s quarter end; however, at the aggregate level, the company’s total sales were up 9.6% to $8.47 billion.

PKG financials in a Snap

Source: Packaging Corporation of America Q4 and FY results – Press Release

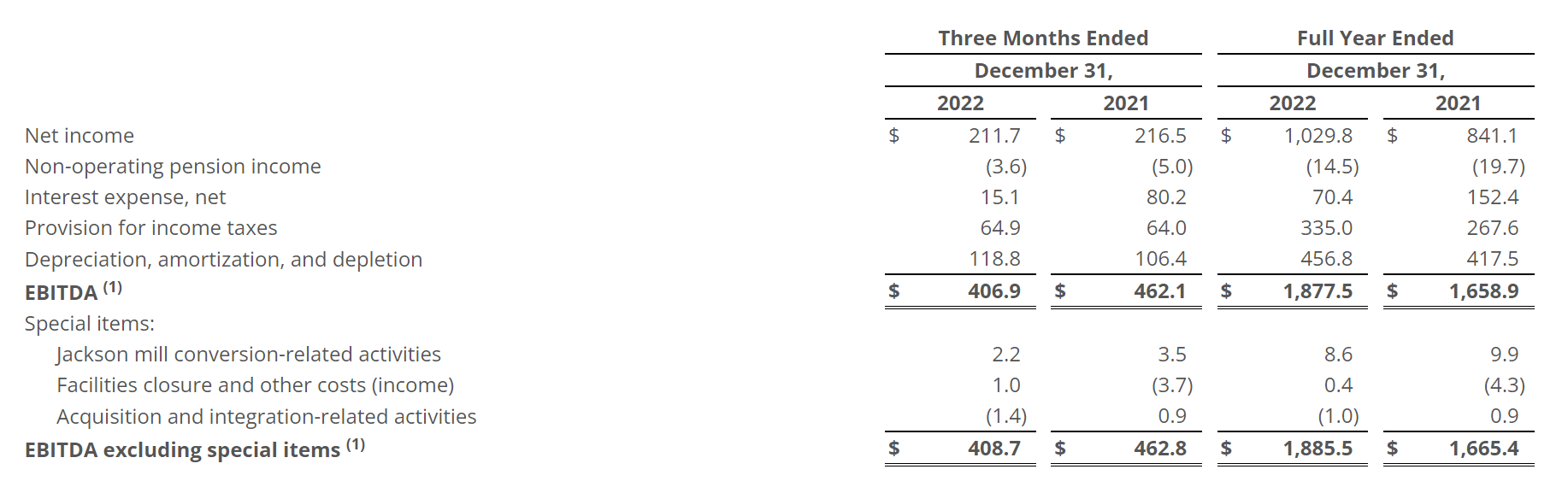

Going down to the P&L, in Q4, EBITDA was lower versus Q4 2021, this was mainly due to lower volumes in the paper and packaging segment, higher scheduled maintenance, and more logistic costs, especially in freight. These costs were partially offset by positive price mix development and lower tax and interest expenses. In detail, despite lower results on the core business (above the EBITDA level), PKG managed to increase its quarterly net income, beating its own internal estimates by $0.12 at the EPS level. At the full-year level and excluding special items, net profit reached $1.03 billion, or $11.03 per share, compared to the $841.1 million reached in 2021.

PKG EBITDA development

In Q4, Packaging Corporation of America was able to offset a slowdown in the packaging segment demand thanks to the mills’ efficiency and effective cost management.

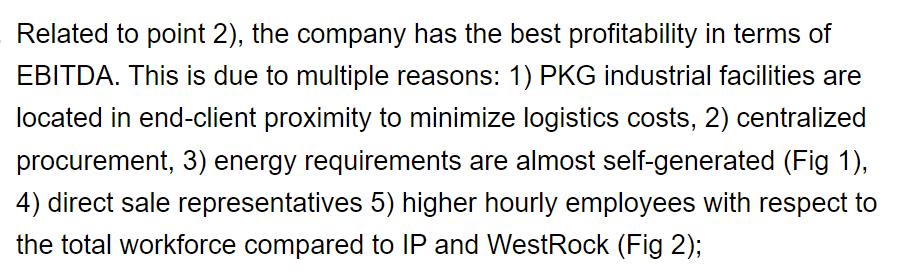

This fully supports Mare Evidence Lab’s investment thesis on PKG’s competitive advantages. As a reminder:

Mare Evidence Lab’s previous publication

Lower volumes were also recorded in IP and WestRock Q4 accounts, this was due to continue inventory destocking. It is important to emphasize how the company is guiding Q1 2023, the CEO said that “in the Packaging segment, PKG expects box demand on a per-day basis to be similar to Q4 levels, although they foresee higher total volume with corrugated plants having four additional shipping days“. He also explained how prices will be lower in domestic containerboard prices as well as in export. Salary and other additional costs such as chemicals will be higher, but they expect lower costs in energy, fiber prices, and logistics.

Conclusion and Valuation

With a lower SG&A expense ratio among the three companies, a lower debt consideration (WestRock’s total debt was again up by $1.7 billion due to the Grupo Gondi acquisition), an improvement in the commodities market with an initial decline in COGS, and an ongoing buyback plan, we expect a Q1 EPS at $2.25 per share which is fully in line with our 2024 target price. Given the peers, Q1 guidances were positive. Therefore, we reiterate our buy rating target at $160 per share.