Netlist Stock: Losses Are Mounting And More License Fees Seem Unlikely (NLST)

DNY59

Introduction

In July 2022, I wrote a bearish article on SA about semiconductor company Netlist (OTCQB:NLST) in which I said that its operating loss could exceed $20 million by the end of 2022 and that I thought the share price would eventually decline to around $2.00.

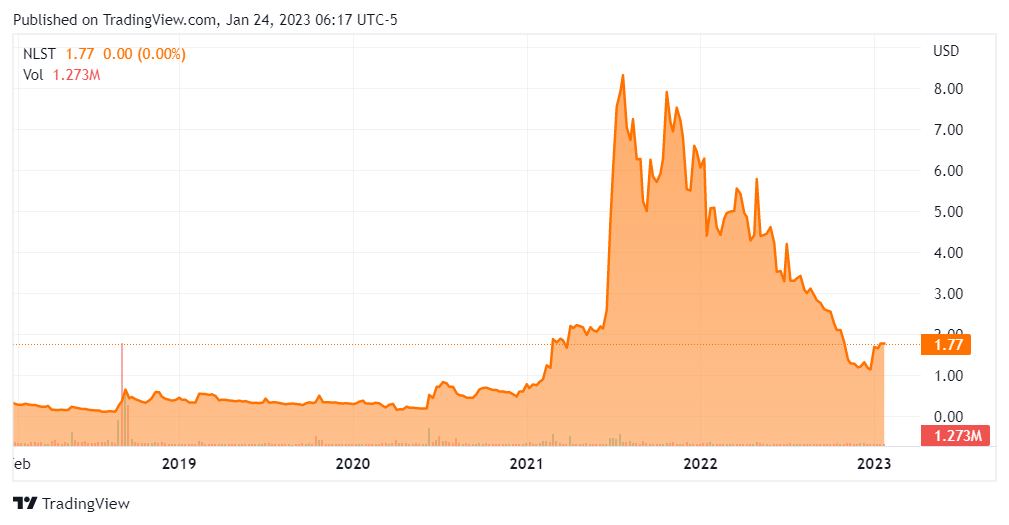

Well, the operating loss surpassed $20 million by the end of Q3 2022, and the share price went below the $2.00 mark in early November. Also, none of Netlist’s major patent infringement lawsuits have made significant progress over the past months. Considering the market valuation of the company has soared by over 60% since late December, I think this could be a good time to open a small short position as the short borrow fee rate is still low. Let’s review.

Overview of the recent developments

If you haven’t read any of my previous articles about Netlist, here’s a brief description of the business. The company is a supplier of solid-state drives (SSDs) and modular memory solutions to enterprise customers. It specializes in hybrid memory solutions such as NVDIMMs. Netlist is based in California but its manufacturing and testing facilities are located in the city of Suzhou in China.

Netlist

The company was listed on NASDAQ in late 2006 but was delisted in 2018 as its share price moved below $1.00. It currently trades on the OTCQB, and it hasn’t tried to uplist despite its share price soaring above $8.00 in the middle of 2021.

Seeking Alpha

In my view, the likely reason for the significant increase in the market valuation back then was significant retail investor interest, as it seemed Netlist had gained meme stock status on the heels of a strategic agreement with South Korean semiconductor giant SK Hynix (HXSCF). You see, Netlist entered into a 5-year product purchase and supply agreement with the South Korean firm after the latter agreed to pay a $40 million license fee following a lengthy lawsuit over patent infringement. This fueled optimism among investors that similar agreements with other players in the sector could follow as Netlist is currently involved in patent infringement lawsuits against Samsung (OTCPK:SSNLF), Alphabet (GOOG, GOOGL), and Micron (MU). The issue here is that these companies aren’t as eager to settle with Netlist as SK Hynix were. Also, it doesn’t seem that Netlist is anywhere close to winning any of the lawsuits. There hasn’t been significant progress over the past few months on any of them. The lawsuits against Samsung and Alphabet revolve around U.S. Patent No. 7,619,912, known as the ‘912 patent, which relates generally to technologies to implement rank multiplication. The lawsuit against Micron, in turn, is about allegedly infringing patented RDIMM and LRDIMM technology, including the ‘912 patent. Considering Netlist spends less than $10 million on R&D per year, it seems highly unlikely that the company is in a position to develop industry-leading technology that multi-billion dollar companies would simply steal. For comparison, intellectual property legal fees for Q3 2022 alone stood at $5.6 million. So even if Netlist gets another license fee payment similar to the one with SK Hynix, the fresh funds will quickly be spent on other lawsuits. After all, Netlist has been suing Alphabet for over a decade.

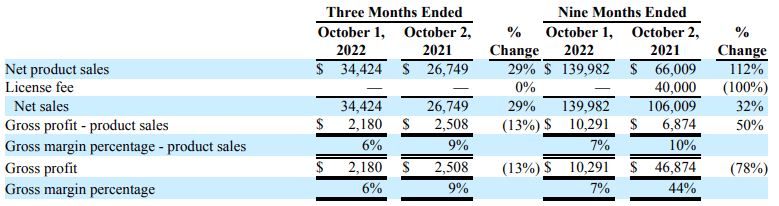

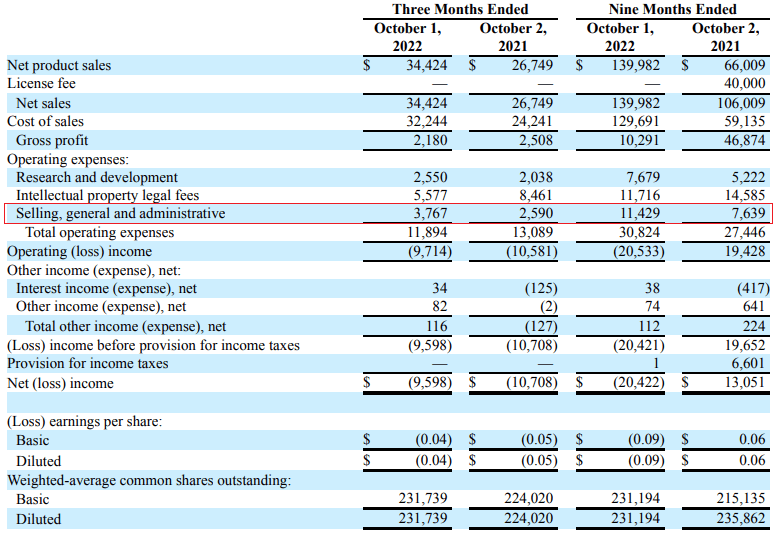

Turning our attention to the financial results for the first nine months of 2022, we can see that while the resale of SK Hynix products is boosting gross profits significantly, the higher SG&A expenses associated with the higher volumes are putting Netlist back to square one in terms of profitability improvement. In addition, we can see from the Q3 2022 results that there don’t seem to be any economies of scale, as the gross profit margin declined to just 6.3%.

Netlist Netlist Netlist

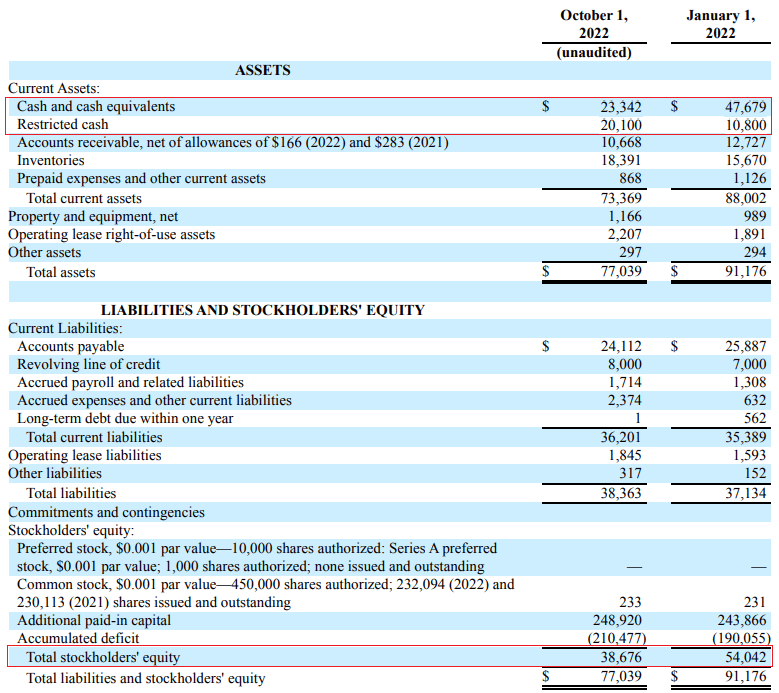

Overall, Netlist has a low-margin business and about three-thirds of its revenues are coming from the resale of third-party products. In my view, the company’s strategy of pursuing patent litigation against major competitors has yielded inconsequential results over the past decade, as the only notable victory is the $40 million license fee from SK Hynix. I think that the companies financial losses are likely to continue mounting over the coming years and that significant stock dilution could be coming in late 2024 as funds start to run out by then. As of October 1, cash and cash equivalents were down to $43.3 million while the stockholders’ equity stood at just $38.4 million.

Netlist

In my view, Netlist is overvalued from a fundamentals standpoint, and I expect the share price to return to below $1.00 in the coming months. So, how do you play this? Well, short selling seems like a viable idea as data from Fintel shows the short borrow fee rate is 6.69% as of the time of writing. The short interest is just 1.02% of the float, and it takes 2.35 days to cover, so the short squeeze risk seems negligible. Unfortunately, hedging is an issue as there are no call options available for this stock.

Looking at the risk for the bear case, I think that the major one is that the share prices of microcap companies can sometimes increase for spurious and unknown reasons. This has certainly happened here in the past on a few occasions. In view of this, it could be best to limit the size of short positions or avoid Netlist altogether.

Investor takeaway

Netlist achieved significant revenue growth over the past few quarters thanks to its licensing deal with SK Hynix, but the company is still in the red and this seems unlikely to change anytime soon. I think that it’s unlikely that Netlist will secure more license fees or settlement payments anytime soon, and the recent increase in the market valuation of the company seems unjustified.

The short borrow fee rate seems low enough to make opening a small short position viable. However, there are no call options available, and I think it could be best for risk-averse investors to avoid this stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.