MYT Netherlands: Double-Digit Customer Growth And Cheap (NYSE:MYTE)

AaronAmat/iStock via Getty Images

E-commerce developer MYT Netherlands Parent B.V. (NYSE:MYTE) recently reported double digit customer growth in Q1 2023 and successful performance of the company’s mobile app. In my view, if management continues accumulating information about customers and fashion trends, the fair price would be significantly higher than the current market price. I fear risks from luxury market regulations and failed forecasts of new trends; however, the stock price appears too low right now.

Significant E-Commerce Expertise And Double Digit Customer Growth

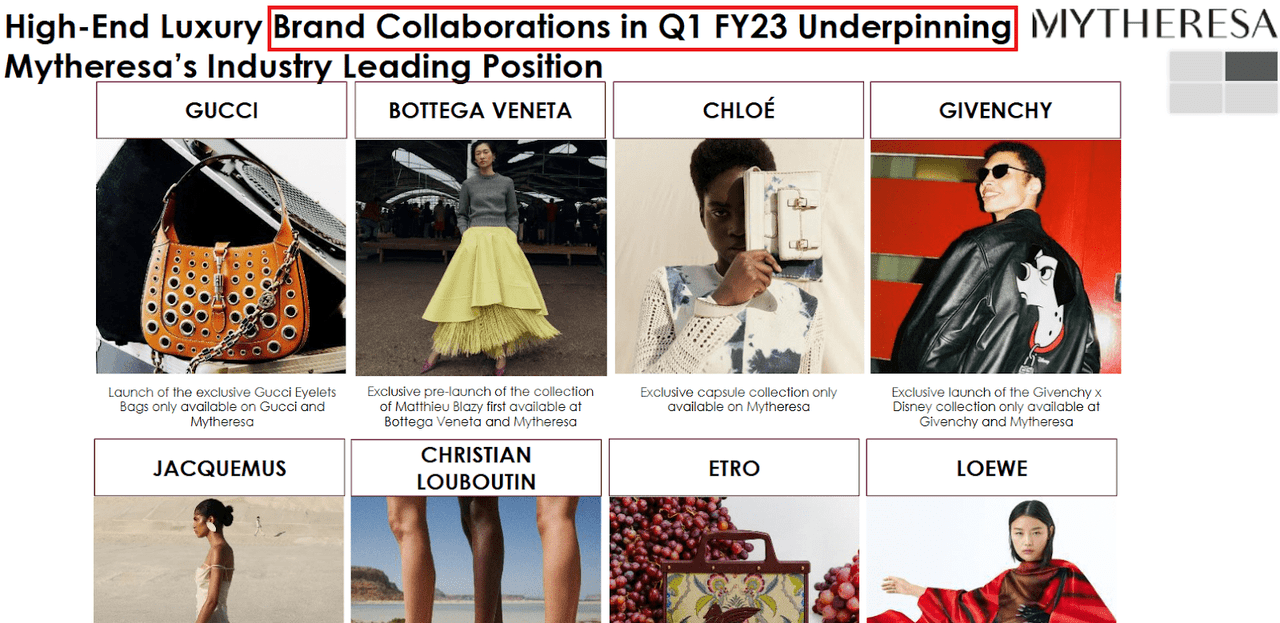

MYT Netherlands Parent, through its subsidiary Mytheresa, offers an e-commerce platform for haute couture and design garments. I believe that the company was a great read after reviewing the most recent agreements with high-end luxury brands reported in a recent presentation to investors.

Source: Investor Presentation

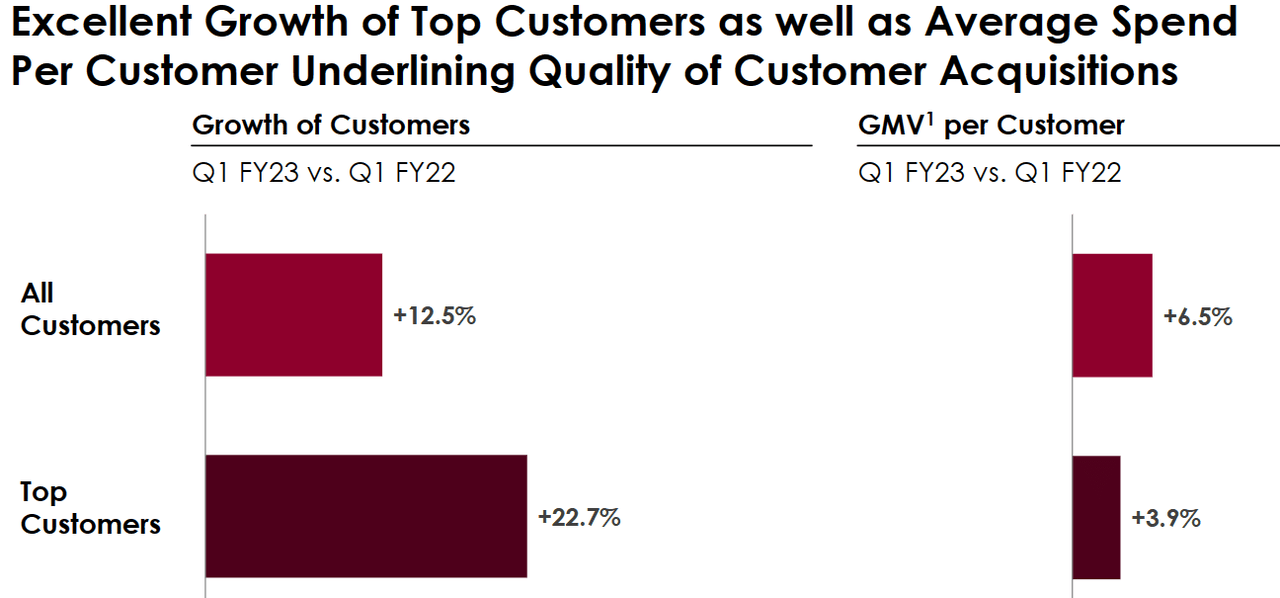

MYT Netherlands does not manufacture or design the products. It only has an online platform. Hence, management appears to be an expert in the analysis of new trends for each season, agreements with the product supplier brands, and marketing and communication strategies to position this platform. In line with these words, I must say that management seems to be quite successful. In Q1 2023, the number of customers increased at the double digit, with average spend per customer increasing too.

Source: Investor Presentation

Solid Balance Sheet With Plenty Of Cash And Little Debt

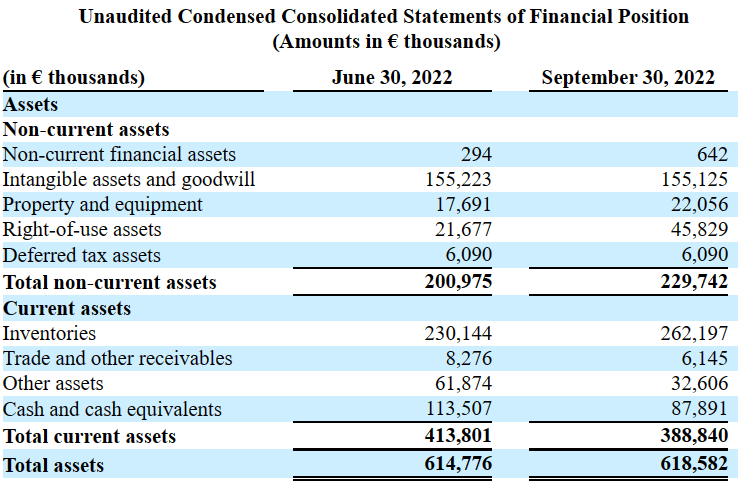

As of September 30, 2022, the company reported intangible assets and goodwill worth €155 million, in addition to property of €22 million and right of use assets of €45 million. Total non-current assets are close to €229 million, with inventories worth €262 million and other assets worth €32 million. Finally, cash stands at €87 million, with total current assets of €388 million and total assets of €618 million. With an asset/liability ratio of more than 3x, I believe that the MYT’s balance sheet appears quite solid.

Source: 10-Q

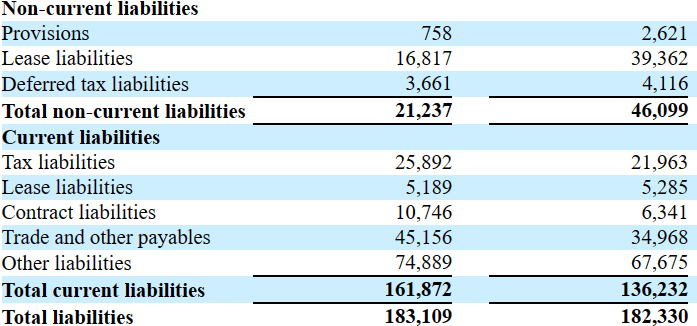

The liabilities reported included lease liabilities worth €39 million with deferred tax liabilities of €4 million. The total non-current liabilities were close to €46 million with tax liabilities worth around €21 million. Besides, contract liabilities stood at €10 million in addition to trade and other payables close to €45 million. Finally, total current liabilities are worth €136 million together with total liabilities of €182 million.

Source: 10-Q

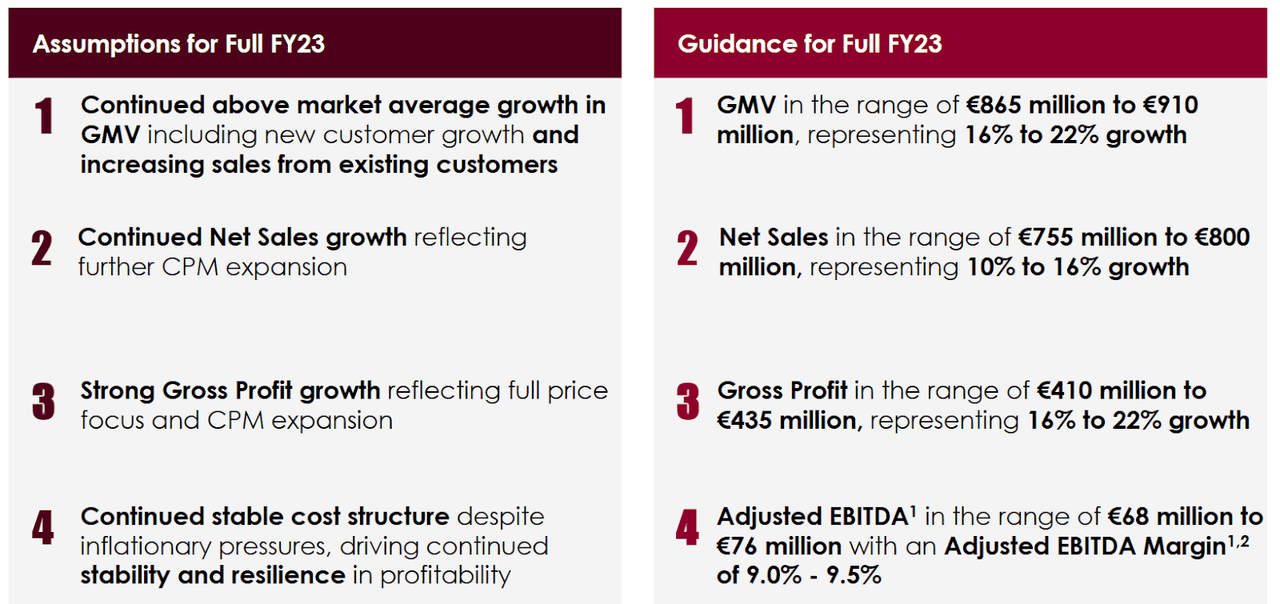

2023 Guidance And Expectations From Analysts Appear Beneficial

In my financial model, I would like to include guidance numbers from management. 2023 net sales would be close to €755-€800 million with sales growth close to 16%-22%. Adjusted EBITDA would stand at close to €68-€76 million, which would imply an EBITDA margin close to 9%-9.5%.

Source: Investor Presentation

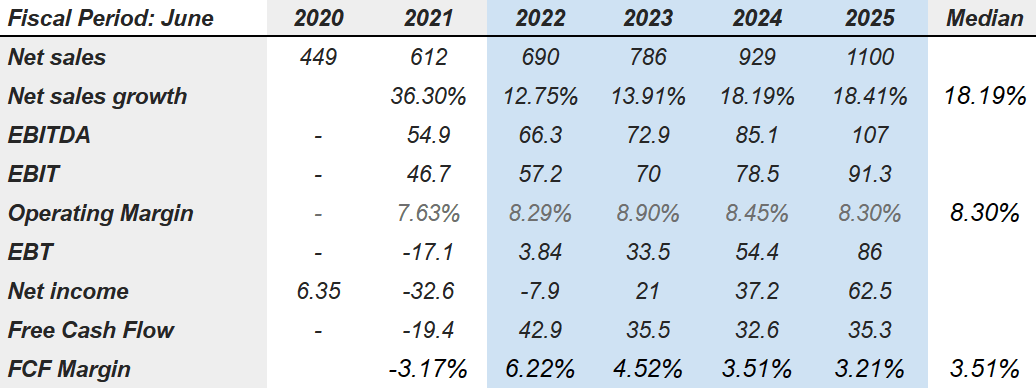

In my view, the numbers of analysts are also optimistic. 2025 net sales would stand at €1.100 billion together with net sales growth of 18.41%. 2025 EBITDA would stand at €107 million with 2025 EBIT of €91.3 million. Operating margin would be close to 8.30% with an EBT of €86 million. Finally, net income would stand at close to €62.5 million, and 2025 free cash flow would stand at close to €35.3 million with an FCF margin of 3.21%.

Source: Marketscreener.com

Better Phone App Applications Could Result In A Fair Price Of $28.3 Per Share

In my view, Mytheresa combines a lot of know-how about the needs of a global segment of the population – mainly in Europe and the United States – valuable information about cost management, and an intelligent observation about the possibilities of technology when it comes to scaling businesses. Under this case scenario, I assumed that this accumulated know-how will likely bring revenue growth and FCF margin generation.

According to the last annual report, MYT Netherlands currently has active operations in 130 countries, reporting more than 781 thousand active customers. Almost 50% of the purchases were made through its digital application (not its website). I believe that further improvements in the company’s mobile and tablet applications could bring significant revenue growth. Let’s keep in mind that the global mobile application market is expected to grow at a CAGR of more than 13%.

Purchases using mobile devices by customers generally, and by our customers specifically, have increased significantly, and we expect this trend to continue. In fiscal 2022, mobile orders accounted for 50% of our net sales, of which 38% were app orders, and approximately 79% of page views were generated via mobile app, tablet and mobile phone. (Source: 20-F)

The global mobile application market size amounted to USD 187.58 billion in 2021 and is projected to grow at a compound annual growth rate of 13.4% from 2022 to 2030. (Source: Mobile Application Market Size, Share & Trends Report, 2030)

I also believe that MYT Netherlands’ stock could be a great asset to protect investors from inflation. Let’s keep in mind that luxury products don’t suffer significant demand declines in inflationary periods. In this regard, management noted the following information.

The demand for luxury products worldwide has been less effected by demand shifts due to inflation than other industries. Source: 10-Q

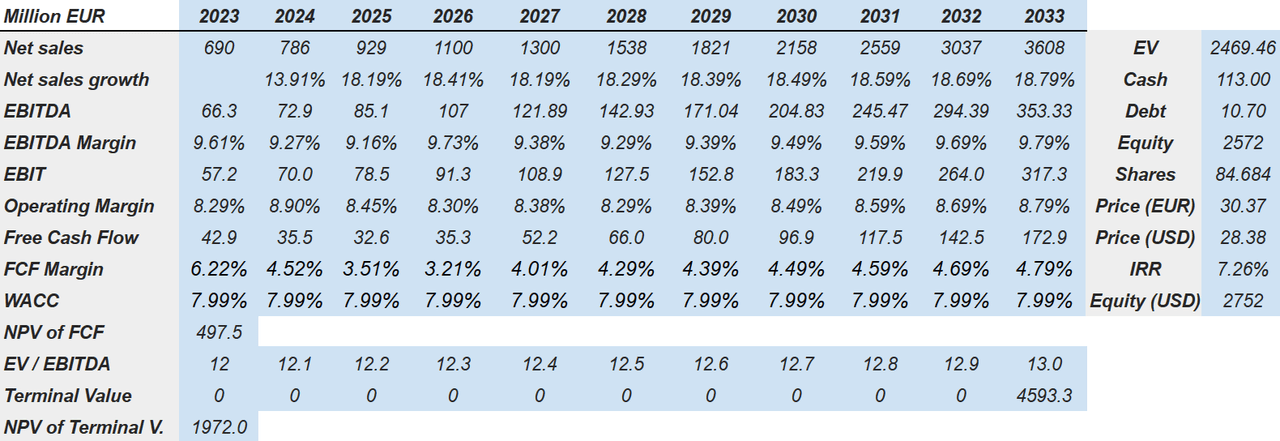

Considering the previous assumptions, I included 2033 net sales of €3.608 billion with a net sales growth of 18.79%. 2033 EBITDA would be €353.33 million with 2033 EBITDA margin of 9.79%. 2033 EBIT would be €317 million along with an operating margin of 8.79%. 2033 free cash flow would be €172.9 million with an FCF margin of 4.79%.

Source: Author’s Financial Model

If we include a WACC of 7.99%, the estimated NPV of FCF would be close to €497.5 million. Besides, with an EV/EBITDA of 13x, the terminal value would stand at €4.593 billion. The NPV of the terminal value would stand at €1972 million.

Under this case scenario, my results would include an enterprise value of €2.46 billion, accompanied by cash of €113 million and debt of €10.70 million. The implied equity valuation would stand at €2.572 billion. The fair price would stand at $28.38 million, and the internal return would be 7.26%.

Risks From Renovation Of Contracts Could Imply A Valuation Of $6.58 Per Share

The digital commerce market for luxury goods is effectively competitive, which forces Mytheresa to be permanently innovating besides providing quality service to its customers. This level of competitiveness is obviously a risk factor for the company. However, it must also be taken into account that due to the high cost, luxury goods are not highly accessible at a mass level, generating a direct dependency on their consumers, who must have a considerable income to make these purchases. Given the economic crisis forecast for 2023, the purchase of luxury goods may be directly reduced, since none of the products on its platform is of vital necessity, and they are not part of an active business network, unlike technology companies.

In the same way, the renewal of contract with brands is a must for future operations since a migration of these brands to other platforms could mean a decrease in the quality of their products as well as their image to consumers. Some of these brands generated exclusivity agreements for some products, which were launched to the market in the Munich store and on the digital platform before anywhere else.

It is difficult, in the case of the fashion and clothing industry, to make reliable projections for the future, since trends and needs of consumers change year after year. Misreading of consumer trends could generate a considerable decrease in profits and the growth of the MYT Netherlands. Under this case scenario, I assumed certain failures, which may bring lower free cash flow margins, and lower fair value.

Finally, as a key risk factor, we could highlight that the change in regulations for businesses of this type in the coming years in China, the United States, and the rest of the world could lead Mytheresa to have to readjust its plans of strategy and business.

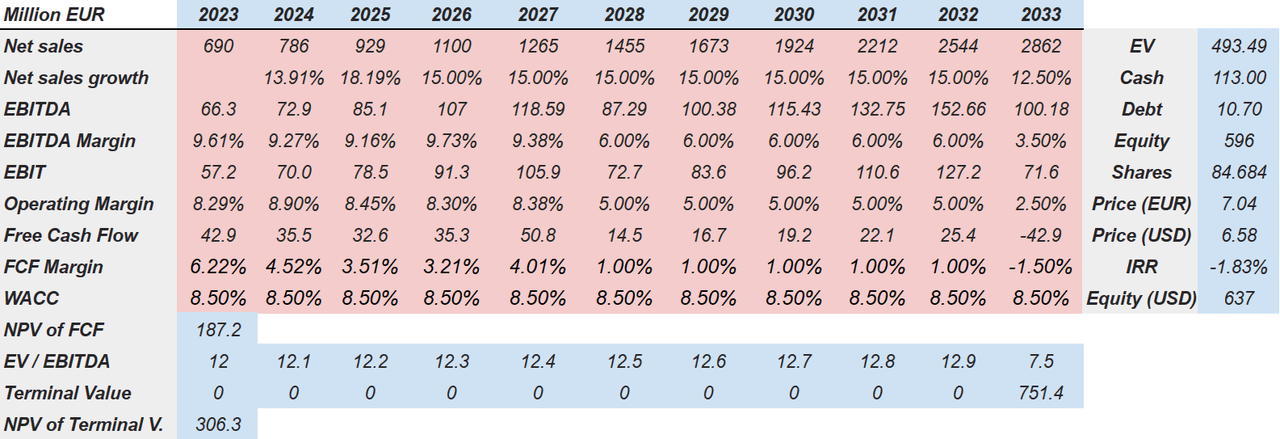

Under the previous conditions, I assumed 2033 net sales of €2.862 billion with an approximate net sales growth of 12.50%. 2033 EBITDA would be €100.18 million together with an EBITDA margin close to 3.50%. 2033 EBIT would be close to €71.6 million with operating margin close to 2.50%. Finally, the FCF would stand at close to -€42.9 million with an FCF margin of -1.50%.

Source: Author’s Financial Model

If we assume a WACC of 8.50%, the net present value of future FCF would be close to €187.2 million. Besides, if we assume an EV/EBITDA multiple of 7.5x, 2033 terminal value would be close to €751.4 million, and the NPV of terminal value would be €306.3 million.

My results would also include an enterprise value of €493.49 million, along with cash of €113 million and debt close to €10.70 million. Equity would be close to €596 million. Finally, the fair price would stand at $6.58 per share, and the internal rate of return would be -1.83%.

My Takeaway

Considering previous customer growth figures and mobile phone app usage, MYT Netherlands appears to know very well how to run its ecommerce business. I believe that further investment in app usability, successful escalation of the business, and sufficient information about customers with sufficient income will likely bring revenue growth. In my opinion, the company appears undervalued. In my base case scenario, I obtained an internal rate of return more significant than 7% and a fair value close to $28.3 per share. Under my bearish case scenario, which included risks from regulation of the luxury industry and no renovation of contracts with certain brands, the implied valuation stood at $6.58 per share.