Moelis: Cold Water On Restructuring Expectations For Now (NYSE:MC)

naphtalina/iStock via Getty Images

Anyone following the sector needs to also follow Moelis (NYSE:MC) because of its earnings calls. We get a lot of information about what the industry expects as of the latest Q4 call. In all, a banking crisis, albeit an averted one, was not foreseen, and this could mean some structural shifts that should lead to a downward revision for Moelis as well as other players in the sector. Moelis has pretty good mid-market exposure, and this was a holdout for now but could turn on souring economic conditions. Ken Moelis threw cold water on restructuring hopes, but even that narrative might change if financing conditions become truly tighter, which they should. Finally, expectations of comp ratio decline and revenue ramp from the resumption of sponsor activity may not actually materialise, despite an inactive 2022. While MC is a great business, markets may want to look elsewhere.

Q4 Update

Comp ratios are up relative to 2020, but also relative to 2021 with revenues declining ahead of comp. Some headcount reductions are being done at the high levels, but this reflects more or less a continuous review of the headcount rather than a major specific event.

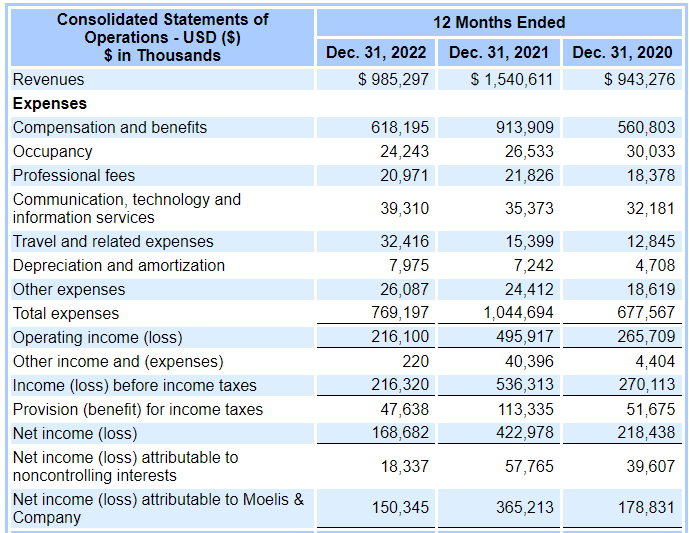

IS MC (10-K)

Revenues are still ahead of 2020 levels, which ended up being a good year for advisors, ahead of 2019 and 2018, but net income is lower than in 2020 primarily due to higher headcounts and compensation, but also because non-compensation expenses have stepped up, especially travel expenses which were minimal in 2020 due to lockdowns. Holdouts despite difficulties in capital markets were mid-market corporate customers, where MC has a pretty good presence. Across our coverage, we’ve seen that companies with mid-market presence have outperformed, and Moelis is middle-of-the-pack in terms of performance and their mid-market exposure.

Mid-Market (Q4 2022 Pres)

Expectations in the Call

Management is very direct and told us a lot about what they think will happen in 2023.

- Capital markets will open up, even LevFin, and sponsors should come back online after a really depressed year.

- There is pent-up demand in the corporate space too, and there remains reasons to make decisions and execute transactions.

- Restructuring will not take off despite the maturity wall, and management expects only the base level restructuring activity to take place, not something revolutionary.

While there are many moving parts, we think that expectations are too optimistic given the cracks we are seeing in the economy. Pressure on regional banking, which is not irrelevant in the US, may create some opportunities among sponsors, but in general leverage is so endemic to the economy at this point that a credit tightening should have a pretty profound effect.

The first effect is economical, and we think this is going to make corporate actors take a pause, where they were still pretty strong, especially in the mid-market in 2022. The second is that further hits to capital markets will make big ticker private equity firms struggle further, while there might be some offsets from regional PE plays that focus on very resilient business models, as well as private credit which may fill in the regional banking lending gap. The upshot is that Moelis said that given a reopening of capital markets, the maturity wall in 2024 and 2025 will not be a major restructuring catalyst. While there’s still some time for things to calm down before then, realistically we are now seeing the effects of the beginning of the downcycle, which means it’s possible that capital markets are not as generous with access when maturities need to be refinanced.

Even if it doesn’t cause more distress than a corporate CFO can handle, the maturity wall shouldn’t be ignored, because it’s going to lead to lower corporate profits as companies refinance at higher rates. That could compound some of the issues for other types of activity that MC depends on.

MC trades at a 20x PE ratio on forward 2023 earnings. They expect revenue ramp up and we wouldn’t be so sure. Things could get ugly as the non-linearities of this rate hike regime really start hitting the economy. Not a buy.

If you thought our angle on this company was interesting, you may want to check out our idea room, The Value Lab. We focus on long-only value ideas of interest to us, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our gang could help broaden your horizons and give some inspiration. Give our no-strings-attached free trial a try to see if it’s for you.