Meritage Homes: Lack Of Market Visibility Leaves Little Upside

Jaskaran Kooner

Meritage Homes (NYSE:MTH) has seen record order volume in the first half of the year, has benefitted from strong pricing power on its homes, and even seems undervalued relative to peers. However, the overall macro picture with the housing market along with a spike in cancellation rates being seen by the company lead me to believe that an investor’s best course of action is to sit on the sidelines. Purchasing mortgage rate locks ahead of time was supposed to mitigate some of the potential cancellations, but the uptick proves that there is no sure solution. With the Q3 call tomorrow after the bell, investors need updated guidance on what the stock is seeing from a demand, price, and supply chain perspective before making a decision whether to invest.

My method of analysis rests in looking at the past two earnings calls of companies and seeing what changed vs. what stayed the same. I’ll then talk about what those similarities and differences mean for the stock going forward as well as how it plays into my valuation of the company through a DCF/3-Statement Model.

What Stayed the Same from Q1 to Q2

Price and Volume Dynamics

Tough comps along with tight supply chain issues caused a common theme of lower home closing volumes across Q1 and Q2. In Q1 the company stated their closing volumes were down 1%, while in Q2 those volumes were down 2%. Still with strong order volumes, the company is doing what it can to mitigate the effects of a tangled supply chain. Pre-starting their entry level homes is one method. The company does this to get a head start on the materials ordering and labor in hopes that by the time a buyer wants to purchase one of their homes, the firm’s planning will have paid off so that the house has already worked through the typical delays. The company also calls out locking in supply volumes with vendors and providing trade constraints visibility in scheduling as ways to maneuver in a tight market.

Even with closing volumes down, revenue has seen a strong jolt upward thanks to the increase in average selling price. Q1 saw price increase 17% while Q2 saw an increase of 13% despite a gradual mix shift from the company into more entry level homes that usually command a lower average selling price. The pricing environment should be interesting going forward- the company stated they still expect to see some pricing benefit with their current backlog in the near term, but as interest rates continue to rise and housing prices are decreasing sequentially (albeit a small amount), the company could start seeing some pressure in 2023. I would argue some price normalization isn’t necessarily a bad thing, especially considering 23 of the last 26 months have seen double digit YoY price growth (the previous 3 months were only single digit increases).

Lumber Locks Pricing Benefit Expected in Future

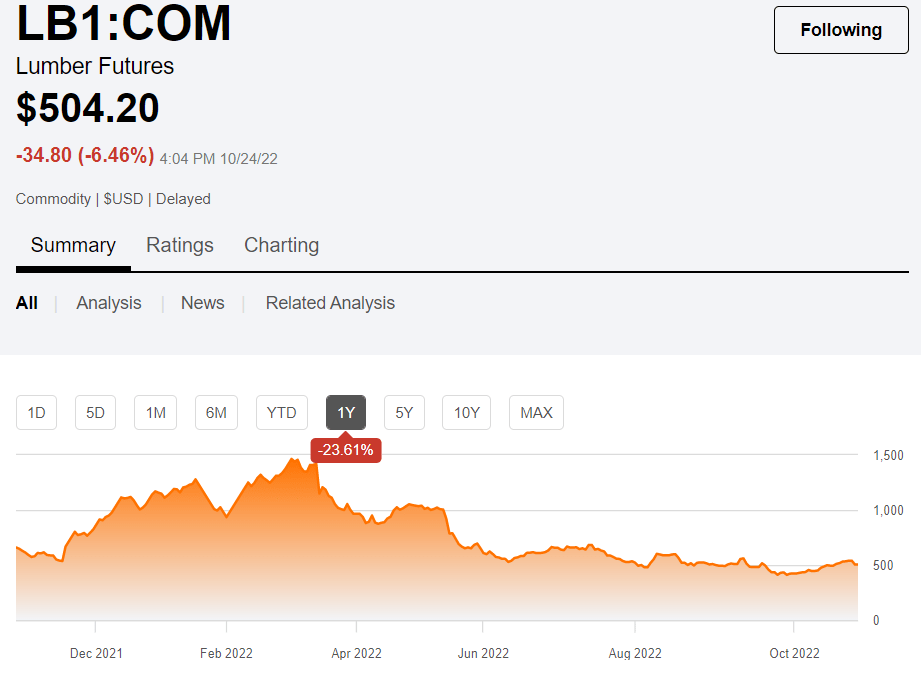

Amid the scorching run of commodity prices last year and early in 2022, Meritage hoped to lock in lumber prices at whatever level they currently were at in hopes to stave off further increases in prices. Since new lumber locks take 6 to 7 months to flow through the financials, lumber prices that were “locked in” at these higher prices have affected and will continue to affect margins throughout the rest of the year. However, now that lumber prices are lower- despite a recent run up- YoY comparisons are expected to be favorable as the company enters the new year assuming the stock is able to lock in at these comparably lower prices at the present day. Here is a graph from Seeking Alpha that should help picture what the company is referring to.

Seeking Alpha

As you can see, lumber locks purchased at the end of ’21 and early ’22 are only just beginning to work their way through the financial statements, but anything locked in around the June timeframe won’t be reflected until at least the end of the year. Unfortunately, on a net-net basis these benefits could be offset by other materials rising as well as increased labor costs.

What Changed from Q1 to Q2

Removal of FY 2022 Guidance

In the Q1 call, FY 2022 guidance was given for a variety of metrics. Revenue was estimated to be between $6.5-$6.9 billion, gross margins at 28%, and an EPS of between $26.30 and $27.90. Nice straightforward guidance that’s easy to model. This no longer was the case in Q2. Due to growing market uncertainty, the company no longer offered full year guidance- although they did offer Q3 guidance (which at that point what’s one more quarter). Perhaps a big part of that decision was a large uptick in cancellation rates seen by the company. In Q1 the cancellation rate was 9.6%, a number that aligned with the previous eight quarters. Q2 saw a large increase to ~20%, with July even higher than that. Meritage was hoping their strategy of purchasing mortgage rate locks for customers in Q1 would decrease cancellations down the road, but it seems the company still got hit hard by the changing sentiment of the market experienced by the rest of the homebuilders.

Looking forward, uncertainty doesn’t seem to be leaving anytime soon. Starts have been on a downward trend and in general, builders look to be slowing down their output thanks to their large backlogs to fall back on. Record mortgage rates combined with stubbornly high housing prices are also creating high monthly payments for potential buyers, adding another layer of hesitancy to the consumer. One could argue that the gloomy outlook has already been reflected in the stock’s price, with the stock boasting a dismal -42% YTD performance, but we’ll get to the valuation shortly.

Large Shift in Share Repurchase Pace

Over the course of Q1, Meritage repurchased over 1 million shares worth about $99 million dollars, leaving ~$54 million left on their most recent authorization. In the Q2 call, the company only reported buying back 128,000 shares for just $10 million- quite the large drop-off despite receiving a new $200 million authorization from the board. Management explained the variance was largely due to a strong focus on using excess cash to build inventory in the quarter. It was also said that in the next quarter or so, more would be revealed on guidance surrounding the topic, but as far as I’m aware, nothing has been released.

A potential investor could take management’s comments at face value and believe that this downshift in buybacks was truly a result of timing and inventory build. A cynic would view that as a cover for the company having concerns about market conditions in the near term, thus wanting to preserve some of that cash flow. For now I see no red flags despite the abrupt shift. With a new share repurchase authorization and solid cash flow prospects- even amid a slowdown- I think share buybacks will pick back up.

What This All Means for MTH’s Valuation

As mentioned in the intro of my article, I derive my share price targets from a discounted cash flow model that is driven by a full three-statement model for each company I analyze. At a high level, here are some assumptions for 2022 and beyond I gained from each earnings call that is input into my models.

1. The first assumptions I implemented into the model was revenue and EPS. For each I used the Seeking Alpha earnings estimates page that holds consensus estimates from 2022 to 2025. Below is a table listing the assumptions:

| Revenue | EPS | |

| 2022 | $6.15B | $25.91 |

| 2023 | $6.29B | $18.91 |

| 2024 | $6.75B | $20.06 |

| 2024 | $7.12B | $21.15 |

Relatively consistent top line growth contradicts a pretty steep fall in annual EPS from 2022 to 2023, which can be attributed to a pretty murky picture for housing next year.

2. The 10-year yield in my model is 4%, a level it’s been hovering around for several weeks now. Significant changes in this rate affect the valuation in a DCF and is certainly something to monitor amid the hawkish path Fed is still going down- although there is increased optimism circulating that they slow down their current pace.

3. Since no official guidance was given in the second quarter, there wasn’t a whole lot of assumptions to go off of. There was some guidance leftover from the Q1 call that is useable. The most straightforward one was an effective tax rate of 25%. One may notice this is quite a bit higher than last year which is due to the fact that the company is no longer receiving tax breaks associated with some of their building last year.

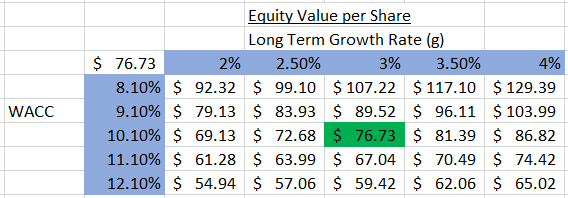

For those familiar with these types of models, there are obviously a lot more assumptions that go into it. In future articles, I plan on digging into my assumptions and what went wrong versus what went right. But to oversimplify everything and provide some numbers, here is a snippet of a valuation sensitivity table with a range of WACC (Weighted Average Cost of Capital) and Long-term growth rate assumptions (both very important for the terminal value of a DCF).

Personal Financial Model

A few notes about the inner-workings of my model and DCFs in general. A DCF sums the present value of all future years’ cash flows. There are two periods we project unlevered free cash flow for. The first stage is your forecast period, which for this model is 5 years. The stage one cash flows are ultimately determined by various assumptions such as revenue growth rate and profit margins, among other things. These 5 years of free cash flows are then discounted by some factor to get the present value of each and then summed together. For Meritage Homes, the sum of its present valued cash flows for the next 5 years is $1.59 billion.

This completes the first half of the enterprise value calculation. The remaining step is to find a way to quantify the present value of all future cash flows after the initial 5-year forecast period. There are a few methods of doing this, but I use the Perpetuity Growth Model. At a high level, this model assumes an infinite long-term growth rate of free cash flows and utilizes this growth rate and Weighted Average Cost of Capital to arrive at the terminal value. This terminal value is then discounted to find the present value, and for Meritage this number is $2.12 billion. Adding this $2.12 billion terminal value of cash flows to the $1.59 billion of stage 1 cash flows brings us to the Enterprise Value of $3.71 billion.

We then need to get to Equity Value, which is first obtained by subtracting cash & equivalents from long-term debt to get Net Debt. For MTH, Net Debt is equal to $877 million. This number is subtracted from Enterprise Value and leaves us with an Equity Value of $2.82 billion. To get our final share price estimate, take this equity value and divide it by our diluted common shares outstanding (36.7 million) to get an average share price of $76.73.

As mentioned earlier, I will be reviewing particular assumptions and their accuracy (or lack thereof) in future articles when more company actuals are available.

Comps

This chart shows some comparable companies to Meritage and how they stack up to one another on certain metrics. It seems like the stock is still pretty cheap comparatively, partly because it also hasn’t seen the same levels of appreciation over the last month. In fact, performance would be well into the negative if it wasn’t for a 5.58% jump in today’s trading session (10/25). To me this puts the stock in a positive light relative to peers.

| KB Home (KBH) | Meritage (MTH) | Toll Brothers (TOL) | |

| EPS (Forward) | 9.58 | 25.91 | 9.27 |

| EV/EBITDA | 4.02 | 2.81 | 5.77 |

| EV/Sales | 0.63 | 0.63 | 0.82 |

| P/E Ratio (Forward) | 2.88 | 2.61 | 4.52 |

| 1 Month Performance | +8.33% | +0.61% | +4.15% |

Source: Seeking Alpha Financials

The Bottom Line

There are certainly shortcomings to primarily analyzing earnings calls, but I believe it can be a very useful tool in a holistic analysis of a stock – especially as wording from executives across these calls can be so strategic and have a deeper meaning than face-value. Financial models also rely on forecasts and inputted assumptions, but just like earnings calls, if they are utilized correctly, they can provide valuable insights into the valuation and financial health of a company.

My Discounted Cash Flow valuation model suggests the intrinsic value of Meritage Home’s stock is $76.73, representing a ~5% upside from the most recent closing price of $73.05.

I still think this stock is undervalued versus some of its competitors, but even with that being said, the market seems to be only leaving a little bit of upside at the current moment. I certainly wish I submitted the article a day earlier to capture today’s nearly 6% increase, but that miss is just part of the fun. The 2023 housing market ultimately is presenting the company with uncertainty, enough so that they even took away 2022 full year guidance. In general, builders are slowing down on what they’re starting and some have started decreasing their average selling prices on a sequential basis. Although the company seems to think there’s pricing left to capture, overall affordability concerns associated with home prices and mortgage rates at 20-year highs may start to bite into those earnings. With their Q3 call tomorrow after close, be on the lookout for updated commentary which can either give investors comfort in Meritage’s strategy to weather the upcoming storm or give investors a reason to be wary about macro factors working their way through the financials in the back half of 2022 and into 2023.