Is V.F. Corp.’s Dividend Now A Buy After The Cut? (NYSE:VFC)

Sjo/iStock Unreleased via Getty Images

Three months ago, I published an article reviewing V.F. Corporation’s (NYSE:VFC) dividend, criticized the lack of safety and growth, and cautioned investors just there for the high dividend.

Previous VFC Article (Seeking Alpha)

A month after my article, the company declared its next dividend payment and reduced it by 41% to $0.3 per share. Let’s look at the recent earnings and determine if the outlook for the business is now better after the dividend has been cut and the price has declined by 30%.

Third quarter earnings and dividend cut

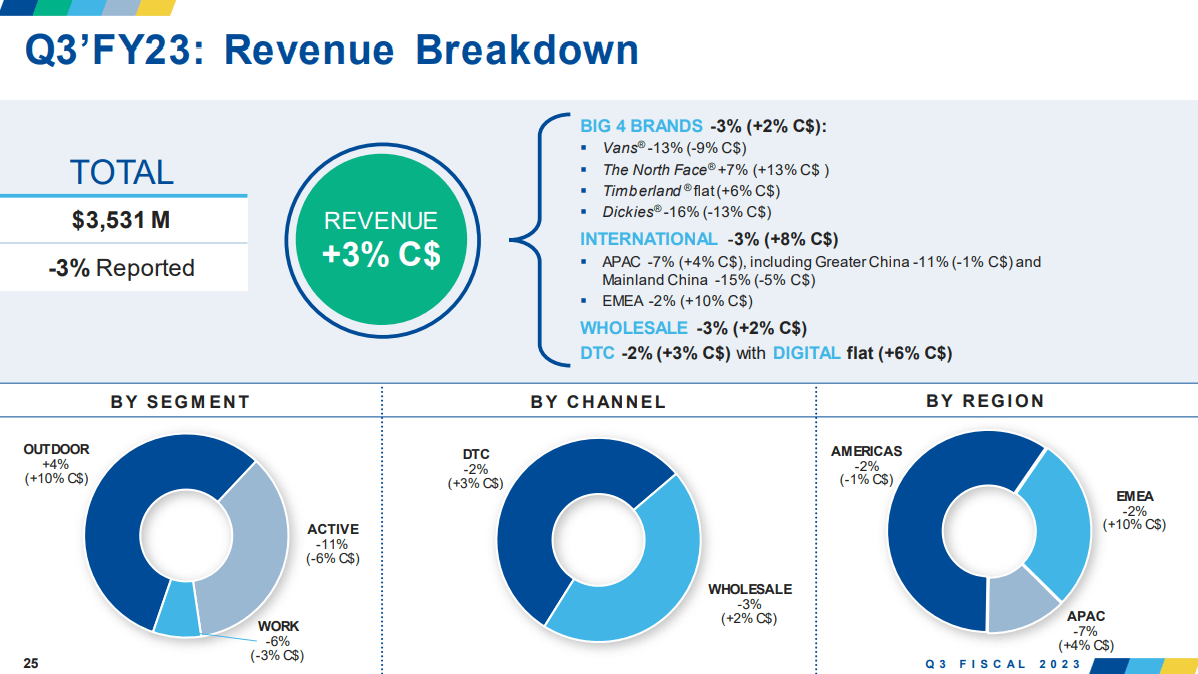

VFC reported its third-quarter earnings in early February and beat expectations ($0.13 Non-GAAP EPS beat, $50 million revenue beat), despite the announced dividend cut. If we look at the revenue breakdown, we see that sales came in 3% below last year but up 3% in constant currencies (“CC”). North Face was the quarter’s highlight, with strong 13% CC growth. International had a good quarter in CC with 8% growth. Vans and Dickies continued to show weak performance. Adjusted EPS came in at $1.12, down 17%. The company managed to reduce inventories by $158 million. As a result of the agreement in Q1 to take ownership of inventory near the point of shipment instead of at the destination, accounts payable increased by 62%. VFC had a negative operating cash flow of $833 million for the first three quarters, an improvement from the $913 million negative operating cash flow after the first two quarters.

Q3 Revenue Breakdown (VFC Q3 Results)

Evolution of FY 23 guidance

Over the last year, the company showed a constant trend of lowering its guidance. In the table below, I compiled the evolution of the guidance starting from before the Investor Day in late September until the most recent outlook. I could have included the Q2 outlook as well, which showed a similar trend, but I did not want to overload the table. We can see that all metrics are declining significantly, especially profitability. Revenues stayed relatively flat, but profitability declined by over 30%. The company has continued to reduce its CapEx expectations, but that doesn’t move the needle.

| Timeframe | Before Investor Day | Investor Day | Q3 Outlook |

| Revenue (C$) | 7%+ | 5-6%+ | 3%+ |

| Adjusted gross margin | up slightly | down 50 bps | down 200 bps |

| Adjusted operating margin | 13.2% | 12% | 9.5% |

| Tax Rate | 16% | 16% | 13% |

| Adjusted EPS | $3.05-$3.15 | $2.6-$2.7 | $2.05-$2.15 |

| Adjusted operating cash flow | $1.2 billion | $1 billion | $700 million |

| Capital Expenditures | $250 million | $240 million | $200 million |

Changes in capital allocation

As a result of the deteriorating fundamentals, management finally decided to announce significant changes to the company’s capital allocation. Starting with the bombshell: The quarterly dividend is getting cut by 40% down to $0.3 per share, and it is explicitly mentioned that returning capital to shareholders is done via the dividend. This rules out buybacks. VFC now also wants to focus on its current portfolio to reinforce the business’s core strengths. Furthermore, they want to pursue strategic alternatives for their global Packs business. To put this into plain English, it means divesting not just JanSport but now also Kipling, Eastpak, and non-core assets ($100 million in land and real estate has already been sold off). The company is looking to lean into cost savings (expected to save $250 million annually by 2024) and focus on investments in its brand and consumer needs. Also, working capital is getting reduced and inventories are aligned. Finally, management strives to realign focus to its highest value creation opportunities and to reduce leverage.

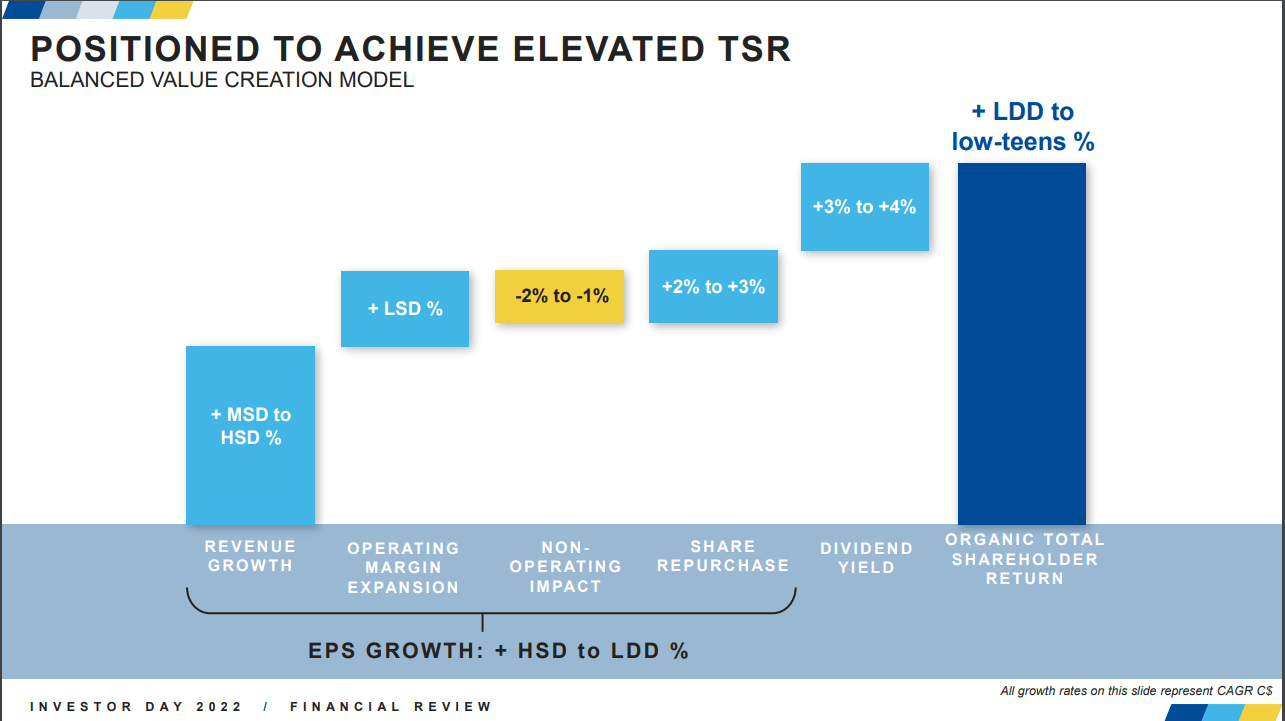

In my last article, I mentioned that Management was too optimistic about future returns for shareholders on its Investor Day. Let’s review what they laid out back then to this reality:

On slide 161, the company showed its FY27 cumulative target of $5.5 billion in free cash flow (“FCF”) generation and $7 billion available to return to shareholders. This means the plan was to lever up more by around $1.5 billion to pursue more buybacks. Now VFC cut the dividend, canceled buybacks, and started to de-lever its balance sheet, quite the 180-degree turn. Furthermore, on slide 162, Business Development and M&A are mentioned to deploy excess capital. Now we see a refocus on the core portfolio and divestitures of non-core assets and underperformers. It looks like management finally accepted the reality and is taking tangible steps to turn around the company. VFC aims to return to its standard supply chain operations in FY24, which severely impacted the business over the last months.

Investor Day TSR outlook (VFC Investor Day)

Is the dividend now safe?

In my last article, I noted that VFC spent much more than its FCF on dividends on buybacks in the past. Now this situation shifted:

- The dividend payout for the next year dropped from $780 million to $465 million.

- Buybacks should be halted.

- Operating Cash Flow is guided at $700 million – $200 million CapEx = $500 million Free cash flow.

- Margins are expected to return to low double digits.

- Asset sales plus excess Free Cash flow can be used to de-lever the balance sheet.

VF Corp is not out of the woods yet, but Management announced the right changes to turn this ship around. There remain several question marks:

- Will the macro drive sales down in case of a recession?

- Can the temporary CEO execute on the ambitions?

- Will a new and competent CEO be found?

- Can the supply chain be right-sized fast enough?

Seeking Alpha also upgraded the dividend safety from F to a D-.

Is V.F. Corp. now a buy?

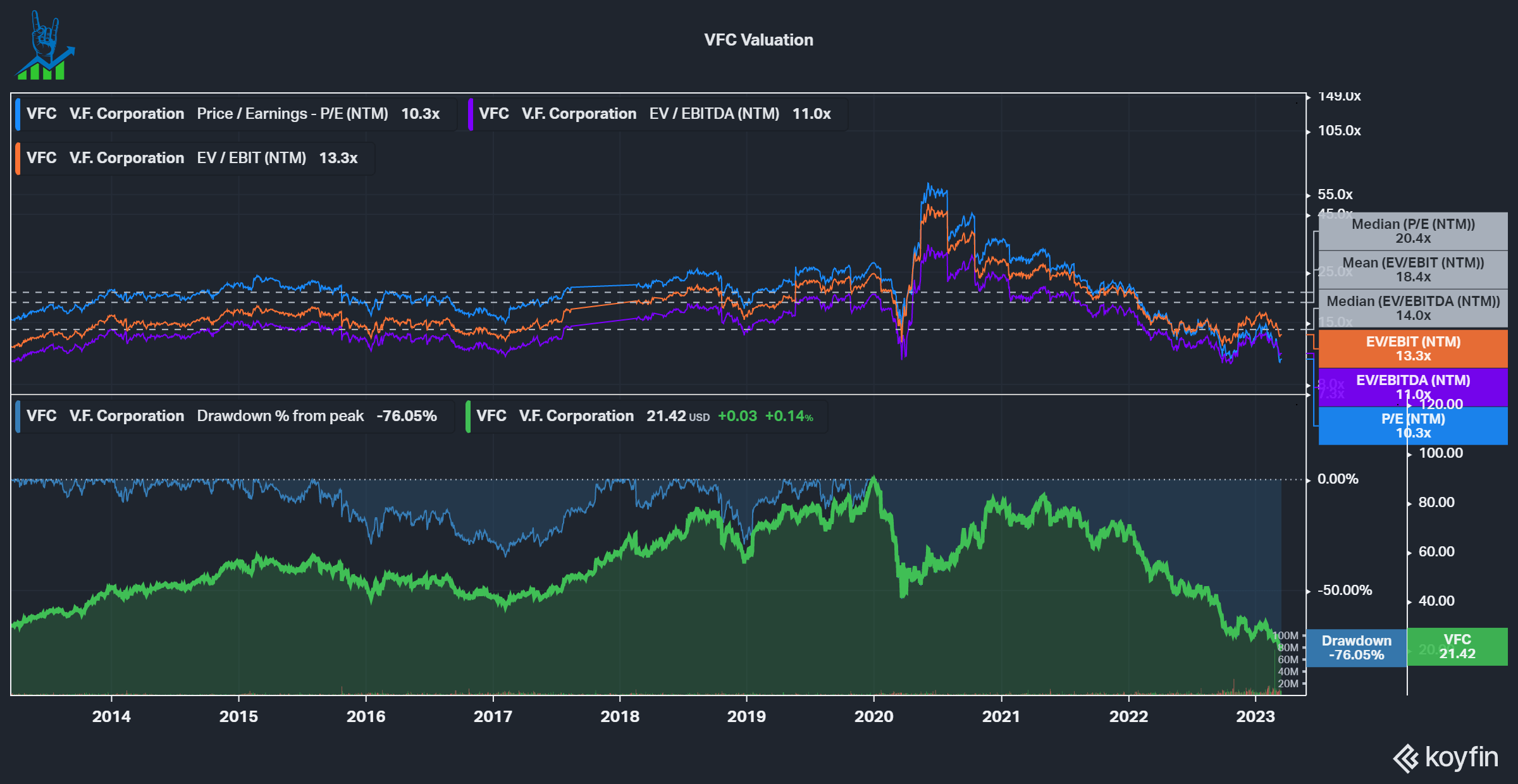

Lastly, let’s look at the valuation. Since my last article, the stock has dropped another 30% and trades at even lower multiples despite the further deterioration in expectations. I excluded FCF yield due to the negative yield, but on P/E, EV/EBITDA, and EV/EBIT multiples, the stock is trading at attractive levels. We cannot forget that V.F. Corporation still owns valuable brands and can make a turnaround if appropriately managed.

I upgrade V.F. Corporation from a sell to a hold. The proposed changes to operations and capital allocation seem promising and are a remarkable turnaround from a prior management standpoint, but we need to see them execute on it. I believe buying a turnaround after it shows signs of success is better than trying to catch the bottom. I will keep monitoring V.F. Corporation, but there are still too many unknowns for me to rate it a buy right now. After all, as the saying goes, “Turnarounds seldom turn.”

VFC Valuation (Koyfin)