Intrepid Potash Stock: Promising But Not At This Price (NYSE:IPI)

iamporpla

Introduction

Over the past year, Intrepid Potash Incorporated (NYSE:IPI) stock has fallen by 25.19% due to high fertilizer costs and the popping of a bubble created by potash supply shock due to the War in Ukraine. While this wasn’t its best year, the company continues to show growth in revenue and sales and benefits from secular growth. Still, not only are macroeconomic risks prevalent, the stock is not trading at an attractive valuation to warrant a sufficient margin of safety. As a result, we place a HOLD rating on the stock and recommend waiting for better buying opportunities.

Company Financials Overview

IPI is a diversified mineral company that produces potassium (potash), sulfur, salt, and water products that are essential in agriculture, animal feed, and the oil & gas industry. However, it’s main two products, which accounted for 91% of total company revenue in Q3 2022, are Potash and its specialty fertilizer Trio. All extraction and production of products are conducted entirely within the United States, with IPI being the only American producer of potash. The locations of extraction and production, or its mines, are concentrated mostly in New Mexico, with the rest coming from Utah.

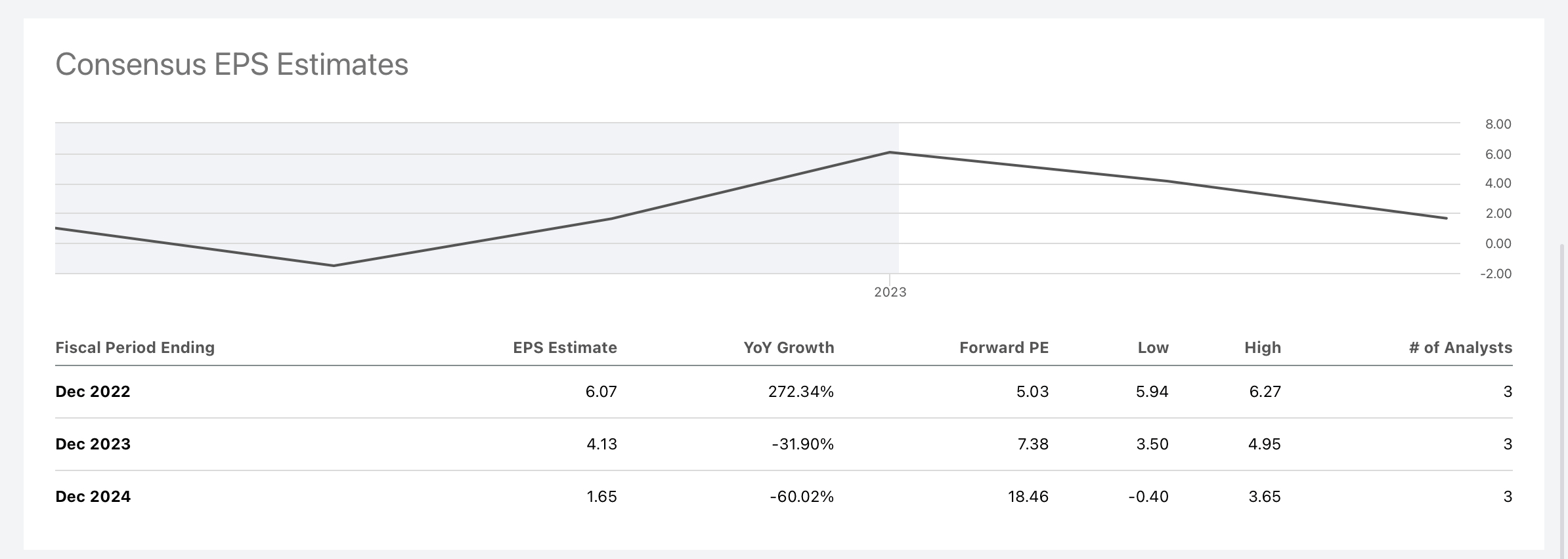

From Q3 2021 to 2022 IPI’s financials have been mixed. Over this period, revenue increased by 36% and net profit decreased by 5%. On top of that, net profit margins increased from 10% to 25%. While the company saw some success throughout 2022, it ultimately ended up having a lukewarm year as it saw a great spike in earnings in the middle of the year and later experienced a decline in earnings back to levels not inflated by a supply shock. As a result, the market rightly priced in the decline in earnings. However, the company is still on track to grow, as analysts are predicting earnings that are still above 2019 and 2020 levels before the artificial spike.

Seeking Alpha

Tailwinds

Future Increased Production Through Expansions and Projects

IPI has had an intense focus on increasing its Potash and Trio production. According to its Q3 2022 earnings call transcript, one focus is IPI’s Moab Cavern Drilling Program, which is on track to have brine production from a new cavern in Moab, Utah by early Q1 of 2023. This brine will be available for the 2023 evaporation season, which in turn will increase Moab’s potash production. At its Carlsbad, New Mexico HB Solar Solution mine, they remain on track to significantly increase brine injection rates into the mine in the first quarter of 2023. The more brine injected directly correlates to the future production of additional products. At the Wendover mine, for the first time in several years, they have recently completed their first new deep brine as well. IPI expects to drill more wells in 2023 to sustain the anticipated increased production for numerous years to come. All these projects are extremely promising during a time when the supply of fertilizer is low and demand and price is high.

The Projected Strength of the United States Cattle Market in 2023

In Q3 2022, animal feed alongside industrial sales comprised up to 40% of IPI company sales. It is important to note that the war with Russia and Ukraine has also affected livestock feed supply and prices throughout 2022. Farmers in the Midwestern U.S. were financially strained by the war, which in turn disrupted feed exports (primarily corn). However, the initial storm has subsided and the feed market is in for a rebound. Decreasing supply of cattle resulting from the contraction in the cattle industry from 2022 should combine with resurgent demand to provide support for prices throughout the year. If demand for cattle rises, especially for beef production, for which the outlook is very positive, then demand for cattle or livestock feed will also increase. IPI can benefit from this in two ways. First, IPI could capitalize on the increased demand for animal feed with its line of products. Second, since increasing demand for corn or soybeans as an animal feed directly correlates to demand fertilizers in the United States, IPI could seriously profit moving forward through its potash and trio fertilizers.

Risk

Farmers Deviating from Potassium (Potash) Fertilizers

With IPI’s potash segment making 54% of its company’s revenue throughout the three quarters in 2022, the potash market is both the greatest opportunity for growth and carries the most risk. In 2022, the potash market experienced a supply shock due to the rapid disappearance of Ukrainian and then Russian potash. This resulted in rapid spikes in price, which subsequently resulted in a significant drop in demand, precipitating a cutback in supply, followed by a fall in price. The inflated prices are predicted to drop between 25% to 30% in 2023. This has already been reflected in the poor earnings shown in Q3 2022. While the global shortage will exist soon, the shortage is not enough to counteract the price fluctuations which not only already have taken a big bite out of earnings but are projected to even more so. This anticipated trajectory in potash prices inherently brings uncertainty for IPI in the near future and greatly contributes to our recommendation against a purchase.

Valuation

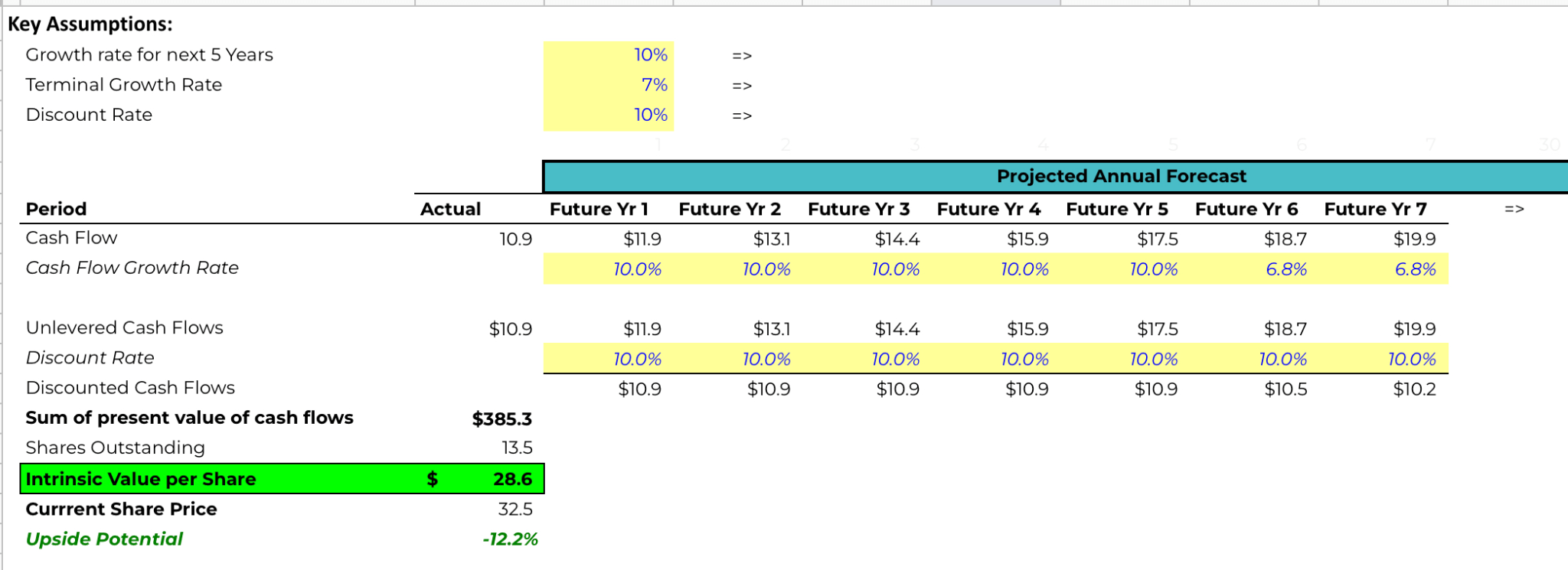

Excel

After performing a DCF analysis, we believe that IPI is overpriced. Using very optimistic assumptions: a 10% 5 YR growth rate, 7% terminal growth rate, and a 10% discount rate, our model still predicts a lower intrinsic value. Wall St isn’t optimistic either, as UBS recently placed a sell rating on the stock, with a $29 price target.

This valuation, corroborated by industry analysts shows that IPI is most likely overvalued.

ESG

IPI’s potash is produced from solar solution mining, which is among the safest and most environmentally-friendly production methods. It does this through its Solar Evaporation Mines.

In terms of worker safety, IPI has committed to exceptionalism. For example, they strive for best-in-class safety (2022 RMMI Safety Award for Large Underground Mines for outstanding safety performance in 2021). They also ensured that not a single worker lost their job during the pandemic, a rarity in the natural resources sector.

Conclusion

In summary, IPI is a company that has had a rough year in terms of stock price. When the general macroeconomic tailwinds and planned expansions are taken into consideration, the company’s fundamentals look strong. However, the current price of the stock and expected declines in potash prices simply do not provide a sufficient margin of safety even with the most optimistic assumptions. Thus, we recommend investors look for better buying opportunities.