Inflation Is A Rorschach Test

Ibrahim Akcengiz

Inflation data continues to be something of a Rorschach test, with conflicting evidence of both structural inflation and a return to low inflation allowing investors to slice the data to support their a priori beliefs. While inflation has remained higher than I expected in some areas, and deflation hasn’t been as large or as sustained as I expected last year, in aggregate high inflation still appears to be a 2021 / 2022 phenomena. From an investor’s perspective, this may not matter, if monetary policy continues to be guided by the highly lagging shelter component of inflation. Higher for longer interest rates still appear likely until something in the economy breaks, although there are already an increasing number of signs of this occurring.

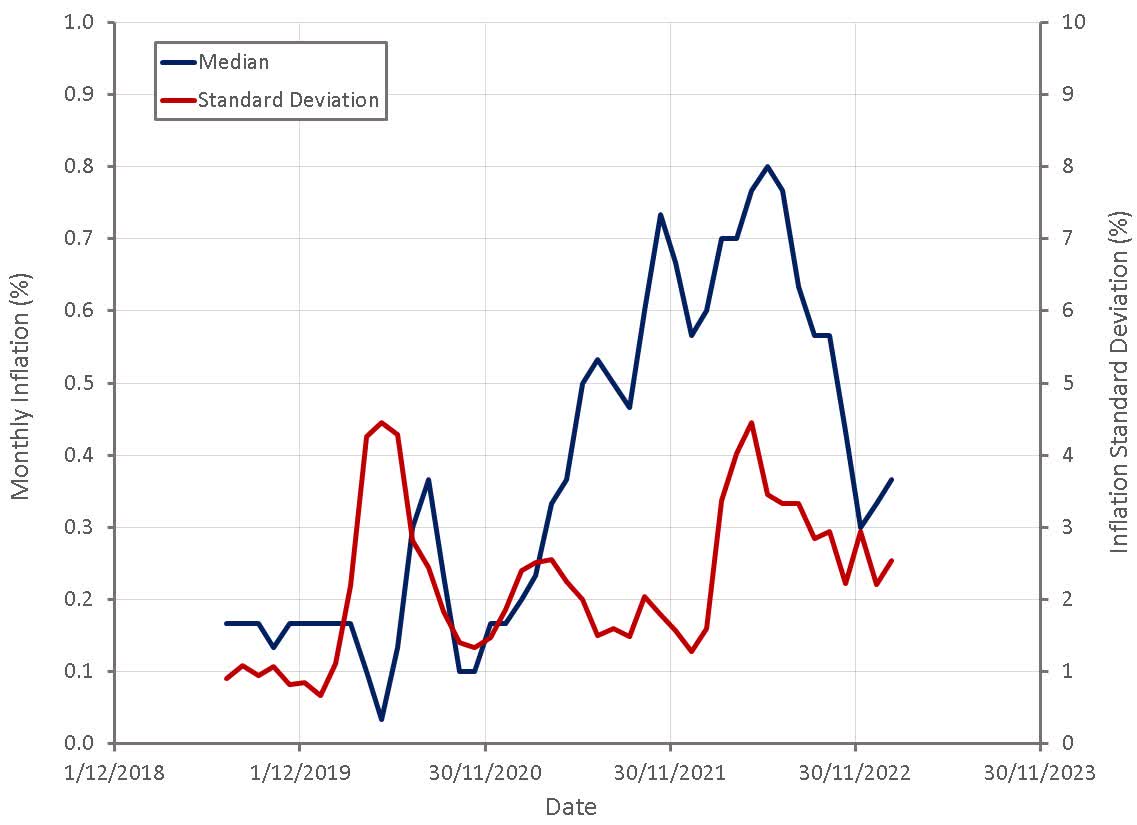

Inflation has clearly still not fully returned to pre-pandemic levels. The prices of many CPI components continue to increase at an elevated rate, and the variance in inflation between components is also still high.

Figure 1: Median CPI Component Inflation and Standard Deviation of Inflation Between Components (source: Created by author using data from BLS)

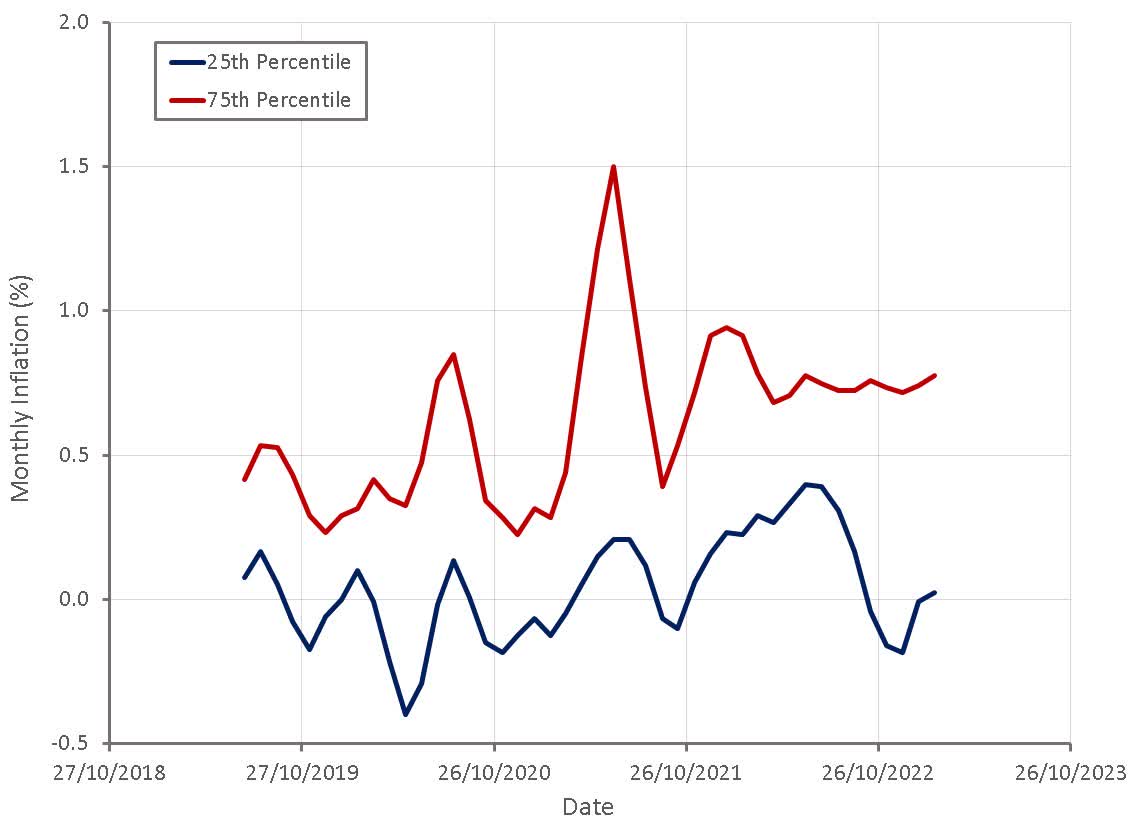

Deflation is also proving to be a fairly short-lived phenomena, with the number of components observing declining prices returning to fairly normal levels.

Figure 2: CPI Component Inflation by Ranked by Percentile (source: Created by author using data from BLS) Figure 3: CPI Components with Declining Prices (source: Created by author using data from BLS)

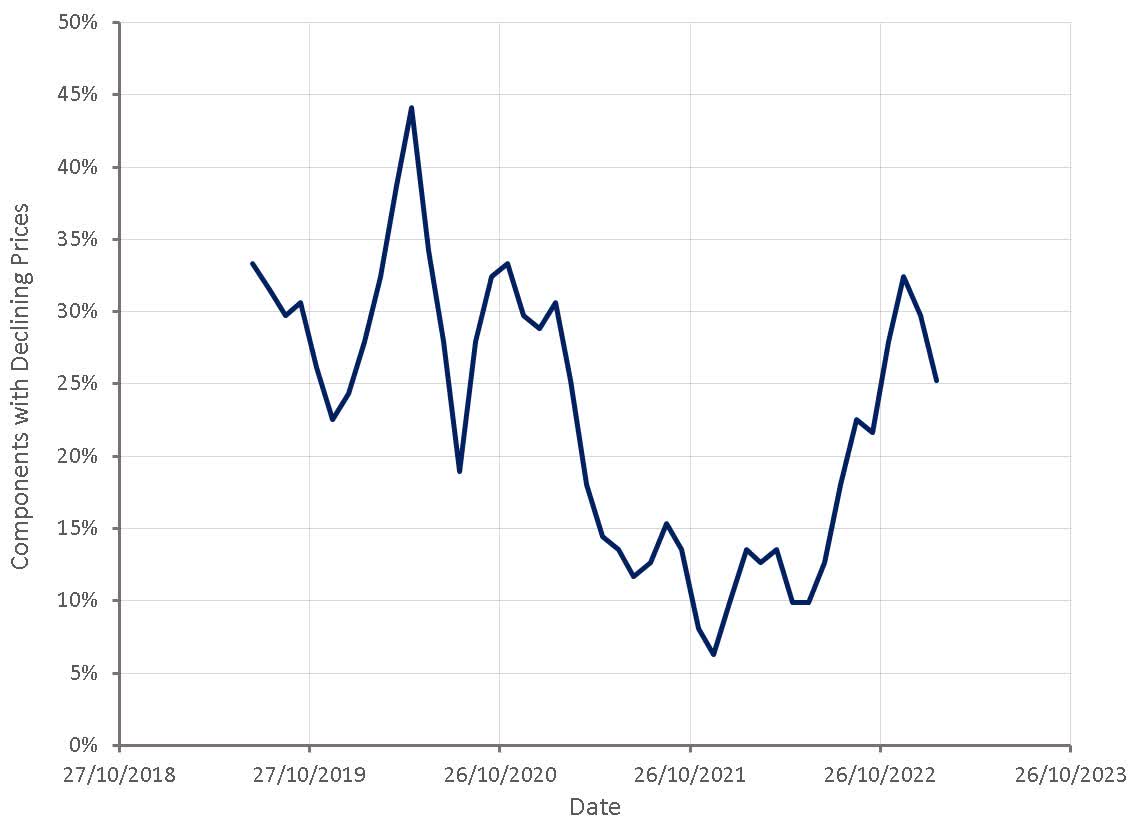

Core CPI inflation continues to be driven by the highly lagged shelter component, which is still increasing on a MoM basis. The shelter component has dominated core inflation for the past 6 months, and will likely continue to do so in coming months.

Figure 4: Shelter Inflation (source: Created by author using data from BLS)

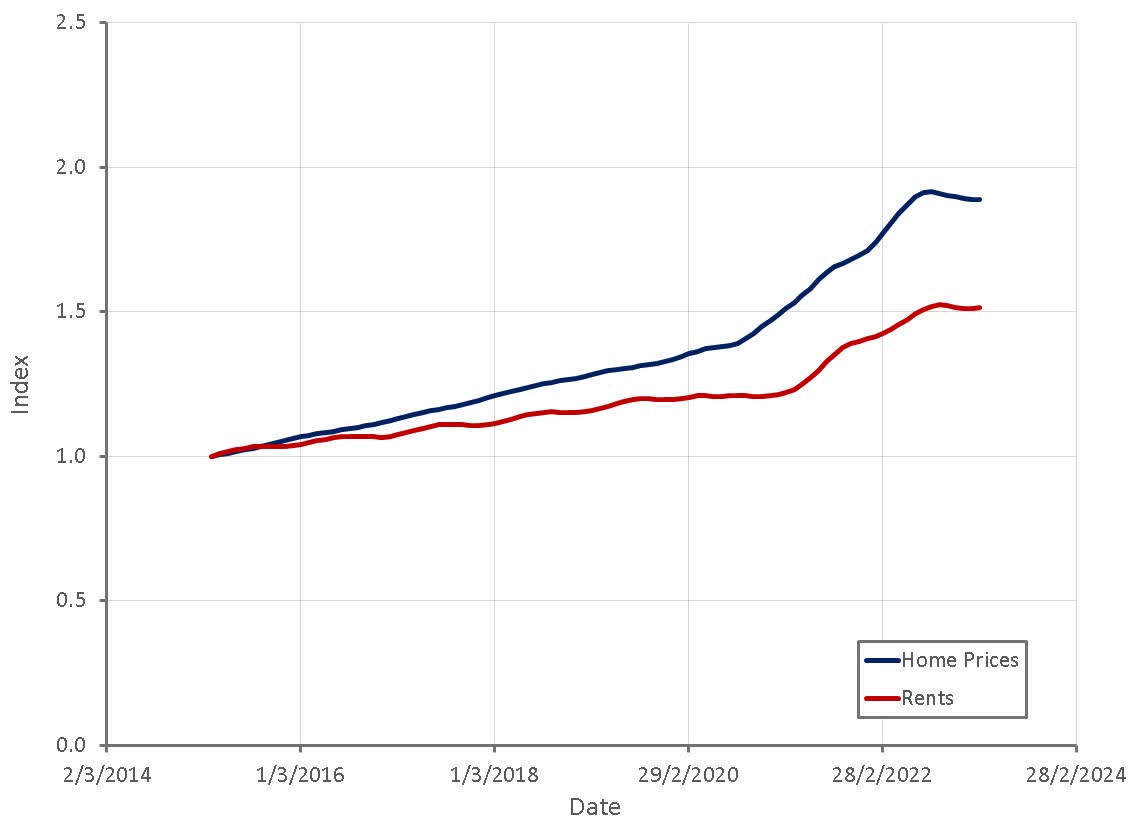

Home prices and rents have been fairly flat over the past 8 months, and are likely to remain under pressure, due to high mortgage rates and an enormous backlog of new housing units that are now finding their way onto the market. This is also important as the shelter component of CPI will likely begin to drag on inflation later in the year, and should not be used as support for overly loose monetary policy in 2024.

Figure 5: Home Prices and Rent in the US (source: Created by author using data from Zillow)

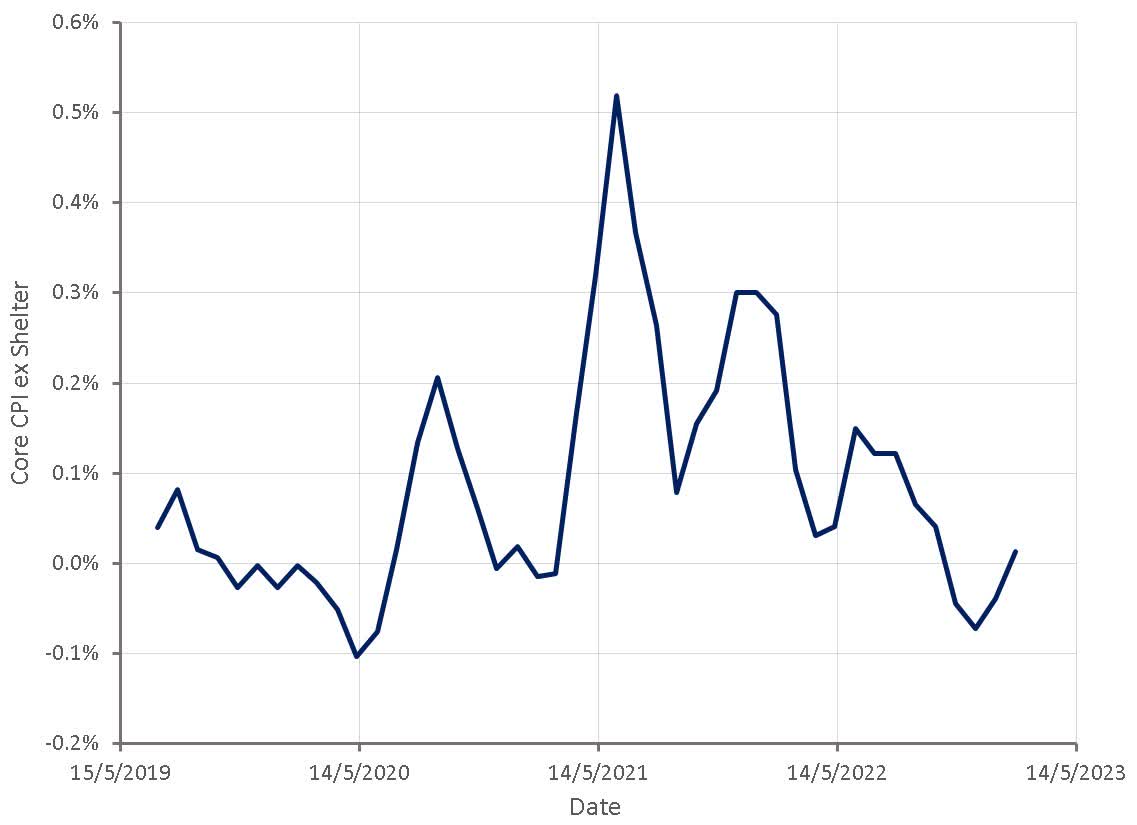

Core CPI inflation excluding shelter continues to show that inflation is not a significant problem, or at least not one that the Fed should be trying to address above all else in my view.

Figure 6: Core CPI Inflation ex Shelter (source: Created by author using data from BLS)

The latest CPI release contains data that could be used to justify further rate increases or a pause. There is little benefit to further increases in interest rates though, and it is becoming increasingly apparent that there are potentially large downsides.

Ignoring the lag in the shelter component, core CPI inflation is no longer a problem, and hasn’t been for months. The Fed may want to see shelter inflation rollover before pausing rate hikes or they may be looking for less CPI components to have high inflation. Given the growing signs of stress in the economy it would appear that the Fed will be forced to reverse course before too long in my opinion.