Immersion: Solid Fundamentals; Valuations Suggest Waiting (NASDAQ:IMMR)

AntonioSolano

Company Snapshot

Immersion Corporation (NASDAQ:IMMR) is a licensing company that provides haptic technology solutions for a range of industries, particularly mobile and consumer electronics (~60% of group revenue), gaming and VR (~21% of group revenue), and automotive (~13% of group revenue), amongst others. As far as geographies go, only 28% of the group revenue comes from the North American region; the bulk of the revenue comes from Asia (62%), with Europe accounting for the rest. The company generates revenue via three different modes- a) Fixed fee licensing agreements (~31% of group revenue), b) Per-unit royalty revenue (~68% of group revenue), and c) Development, services, and other revenue (~1% of group revenue).

What’s To Like?

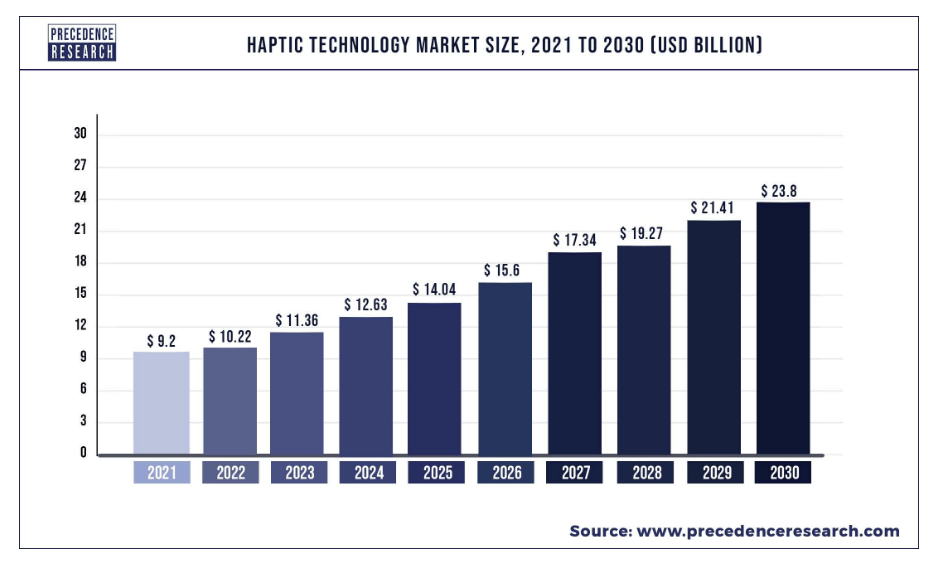

A market poised to witness increased adoption

For the uninitiated, haptics technology can play a key role in enhancing the quality of engagement with digital experiences and 3D communication by enabling humans to use their sense of touch. This can lead to a more heightened sensory and immersive experience, in keeping with the real world. You can imagine how tantalizing this tech could be, particularly for mobile or consumer electronic entities that are constantly trying to reinvent and deepen the end-user experience. Potentially greater adoption of haptics tech is reflected in the superior growth potential of this market, which looks poised to grow at a double-digit CAGR of 11% through 2026, a far cry from the overall mobile smartphone market which will likely only grow at ~2% CAGR during the same period.

Precedence Research

Compelling IP Makes IMMR An Ideal Acquisition Candidate

It’s fair to say that Immersion Corp is something of an authority in the field of haptic technology, as it has been developing IP in this field for close to three decades now. Most of its vast patent portfolio (1200 issued or pending patents as of FY23) focuses on the foundational aspects and the commercial applications of haptic technology, giving it solid coverage and credibility in this field.

In fact, quite a few large entities such as Xiaomi, Apple, and Meta have tried to bypass IMMR’s wide-reaching haptic expertise and churn out products in this space, only to come up against patent infringement lawsuits, which IMMR typically tends to win (or settled via future licensing or royalty agreements).

IMMR is also well-placed to take up a leadership role and set up established and common standards that could drive further adoption and integration of haptic technology across various applications.

Currently, IMMR has a rather small team of just 19 full-time employees, and it also does not look like they are deepening their engagement in R&D (in FY22 R&D expenses were down by 67%). In many ways, it feels like IMMR is standing still, waiting for a bigger entity to come along and leverage its IP and licensing qualities. Going forward, I wouldn’t be surprised to see IMMR get taken over by one of the big-tech players looking to deepen haptic adoption in the metaverse.

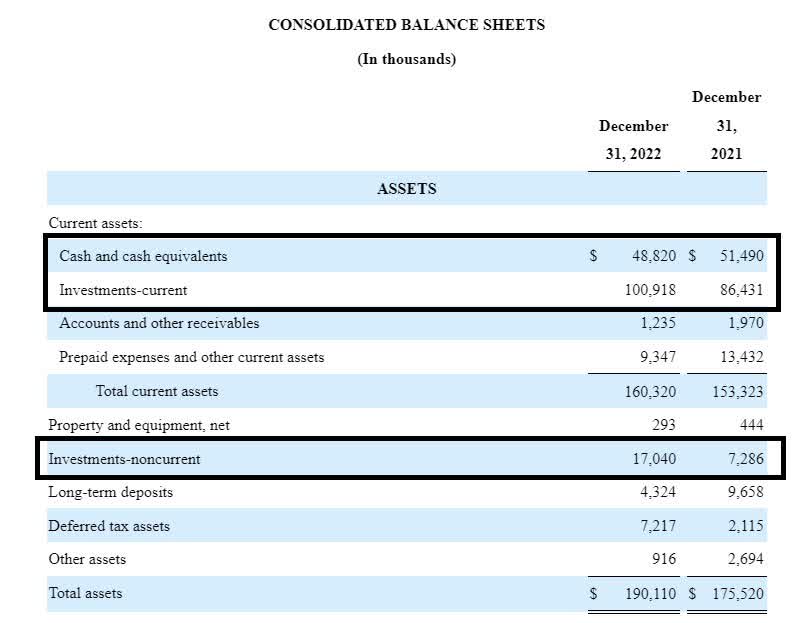

Solid Balance Sheet

A potential acquirer will also likely be buoyed by the quality of IMMR’s balance sheet. Firstly, the company does not have any debt. Secondly, if you look at its asset base of $190m, you’d note that 62% of the asset base comes from investments, with the bulk of this accounting for short-term marketable debt and equity securities (53% of the asset base, the largest share of assets). Besides that, it also has a healthy cash portfolio of $49m. At a time when most small-cap stocks are being punished for being excessively financially levered, IMMR stands out.

10-K

Burgeoning Theme of Shareholder Returns

An alluring theme of IMMR which has only cropped up recently is that it’s become more generous with sharing its largesse with its shareholders. The company recently initiated a quarterly dividend of $0.03 a share (it was first announced in November, followed by another one in February) which one can expect to persist for the foreseeable future. In addition to that, late last year, the company also pushed through a special dividend of $0.10 a share.

Besides the dividends, the share price could also get further support from increased buyback momentum. Late last year, the company announced a $50m buyback program with an expiration period of 12 months; this is not a small number, as it accounts for almost 20% of the company’s total market cap.

Closing Thoughts

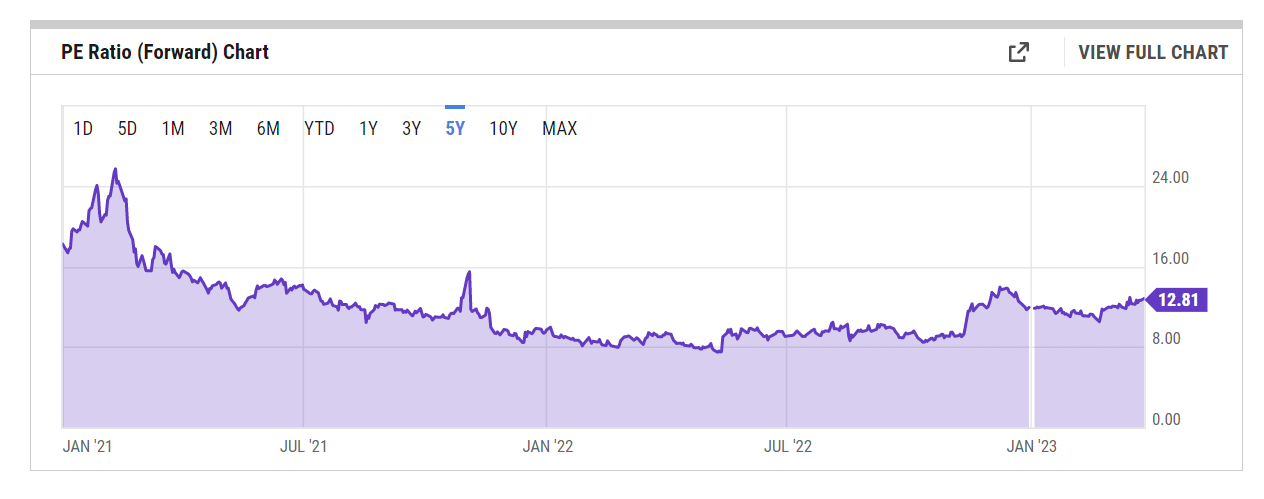

For all its useful qualities, I’m not sufficiently convinced that an entry at this point in the IMMR stock will prove to be too rewarding. Firstly, valuations are no longer cheap; consensus estimates for FY23 point to a 27% decline in the annual EPS (estimated figure of $0.64). At the current share price, that would translate to a pricey forward P/E of 12.8x, ~10% higher than the 5-year average multiple of 11.7x.

YCharts

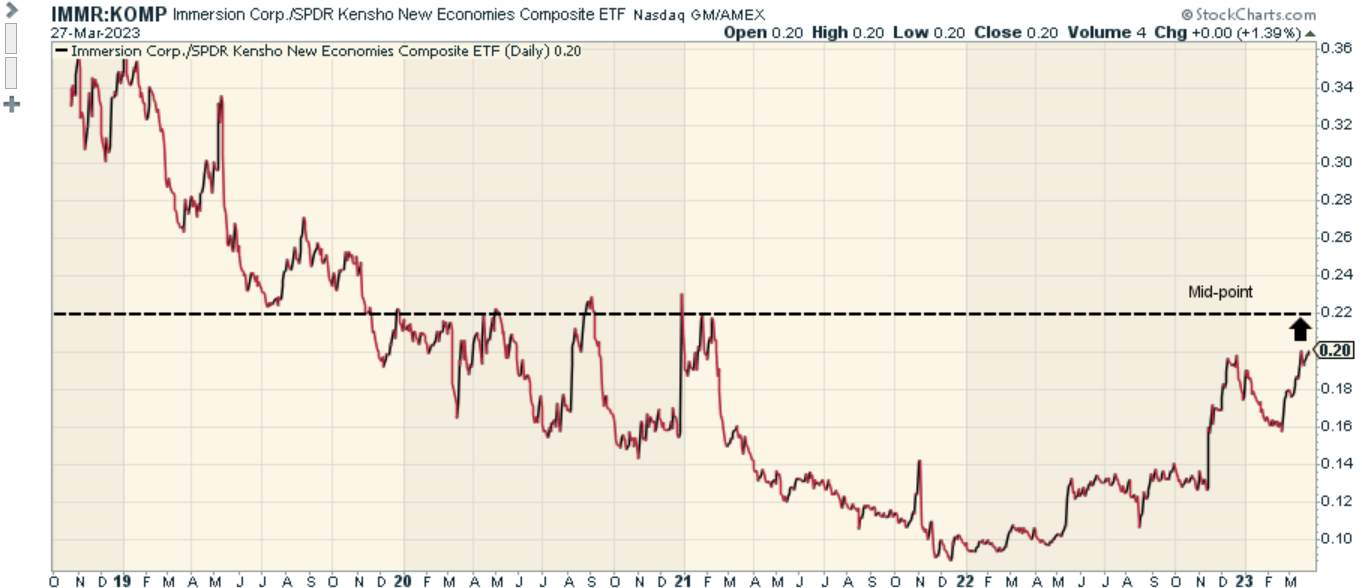

IMMR has also had a good run over the past year (57% returns), and at this juncture, it’s difficult to see scope for further potential mean-reversion momentum, in relation to other new economy stocks that have the potential to disrupt traditional industries (as captured by the SPDR S&P Kensho New Economies Composite ETF (KOMP)). From the image below, we can see that the relative strength ratio of IMMR and KOMP is now on the cusp of hitting the mid-point of its range.

StockCharts Investing

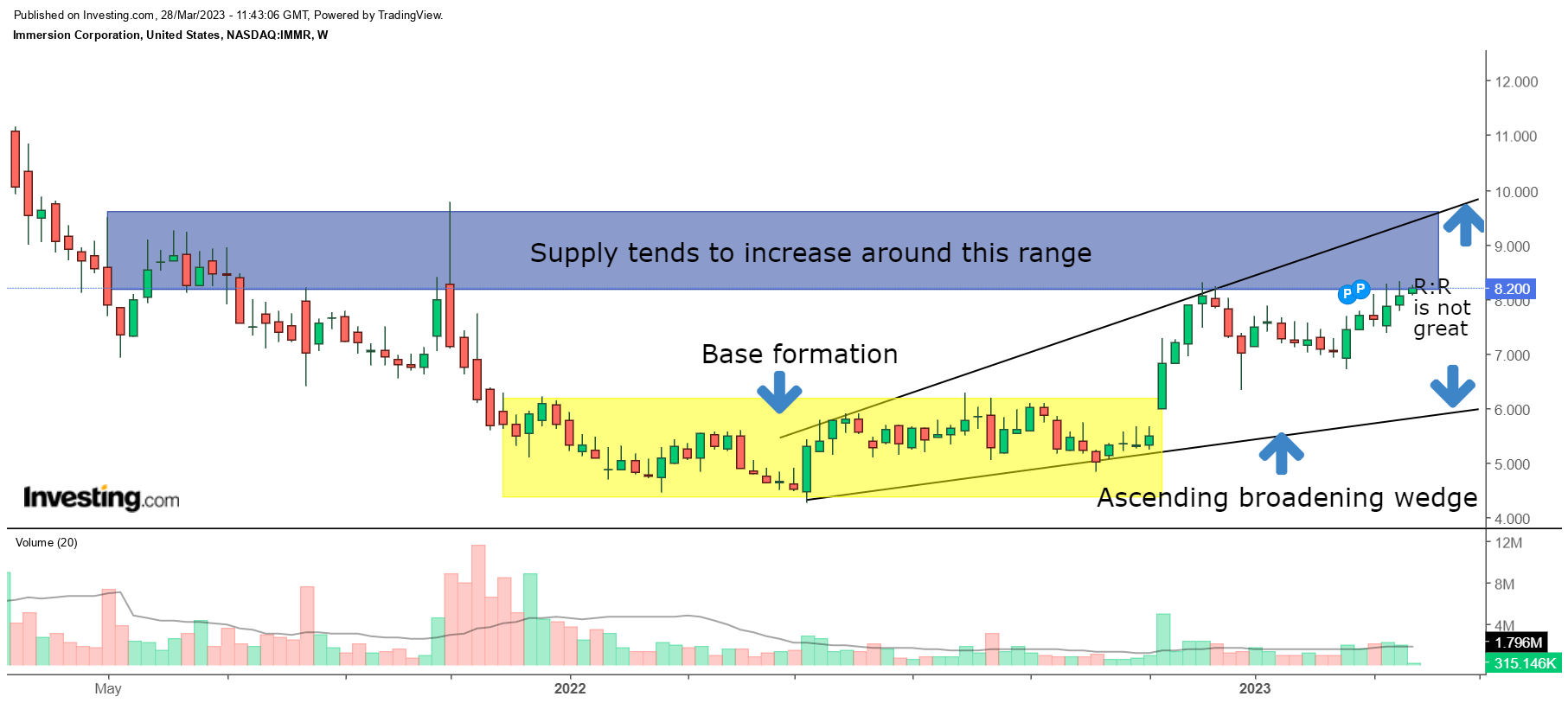

Then, on the standalone chart, the IMMR stock did well to build a nice base for much of 2022 between the $4.20-$6.00 levels (that would have represented a good point to build a position), after which we saw the stock spike up in late 2022 (although there wasn’t a commensurate spike in volumes). Since mid-May, the stock has been trending in the shape of an ascending broadening wedge pattern, and a long position at the current price point would represent a sub-optimal risk-reward of 0.8x. Also note that the stock is not too far away from a zone that has previously seen a lot of supply come in, thus potentially limiting further upside.