HubSpot Stock: SMB Extraordinaire (NYSE:HUBS)

da-kuk

Cloud software is one of the best business models in the market. Companies are generally able to automate much of the customer touchpoints and onboarding, there is very little increased expense as the company scales, and the margins are incredible. Many companies choose to sacrifice short-term profits by maximizing sales and marketing spend, although many also poorly allocate capital in other expense lines. It’s a luxury the space affords, considering the premium investors are willing to pay for revenue growth, and the promise of future profits. The best-in-class are able to scale while maintaining GAAP profitability and with a keen eye to expense management. I’ve written about several of these, but today I want to focus on HubSpot (NYSE:HUBS), a multi-hub cloud provider born from marketing automation which has spread across CRM, Service, and other offerings in the SMB cohort and built itself a strong niche.

Secret Sauce

Company Presentation

HubSpot’s secret sauce is difficult to understand, at first. The company operates in the swim lanes of many larger and more well-capitalized companies, like Salesforce (NYSE:CRM), Microsoft (NYSE:MSFT), Adobe (NYSE:ADBE), and others like Zendesk (NYSE:ZEN). There’s no lack of possible competition. However, they’ve continued to chug away with massive revenue growth.

Company Presentation

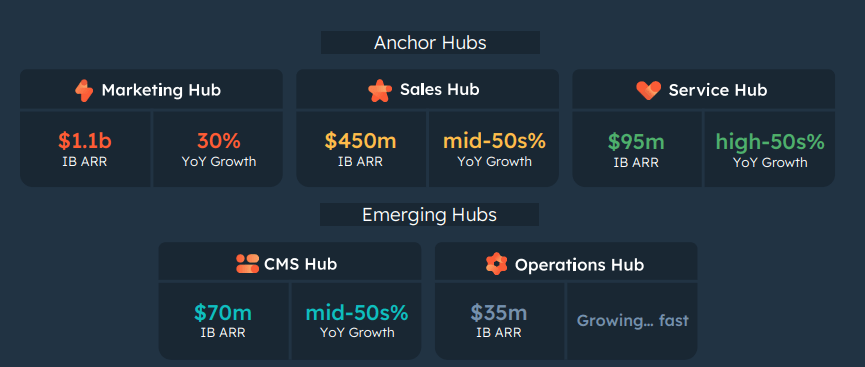

The key here is serving the SMB segment (2-2,000 employees) is a spot where they can effectively tailor their offering specifically to a certain sized business. With free tiers and then ramped spend options depending on feature needs, they offer low-friction onboarding and sufficient offerings to serve as nearly a one-stop shop. HubSpot ends up being the best answer for many of the SMB’s which have traditionally been underserved by cloud software. Their ability to continuously churn out additional high-quality offerings to allow for land-and-expand to work is a key competitive advantage for the company.

HubSpot offers a self-guided demo along with its free offering, which builds out the sales funnel to the Starter tier, which the company recently automated to lower services expense. The company was launched initially off its marketing offering, but the Starter CRM is typically where new customers begin. Around 2/3 of annual recurring revenue gets its start in the free tier, which has proven to be one of HubSpot’s smartest strategies. As the company proves its value, customers grow with them and deliver increasing revenue over time with headcount growth as well as increased business complexity necessitating additional offerings.

Company Presentation

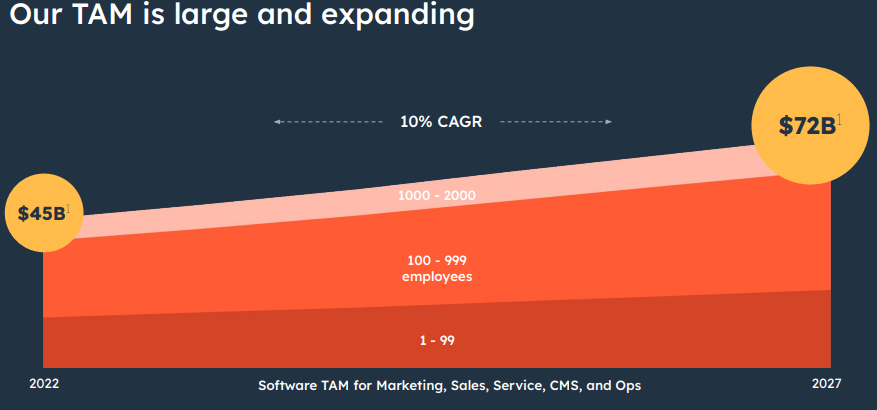

Although some TAM projections out there are laughable, enterprise software really does maintain massive potential. Bringing legacy systems into the cloud is a huge opportunity for software companies, and represents a tax on doing business across nearly every business size.

The company sells its products directly in transparently priced, tiered offerings, and also sells through partner channels. These partners represent 33% of customers, but 45% of revenues brought in, which shows they are responsible for an outsized amount of the medium-sized business onboarding.

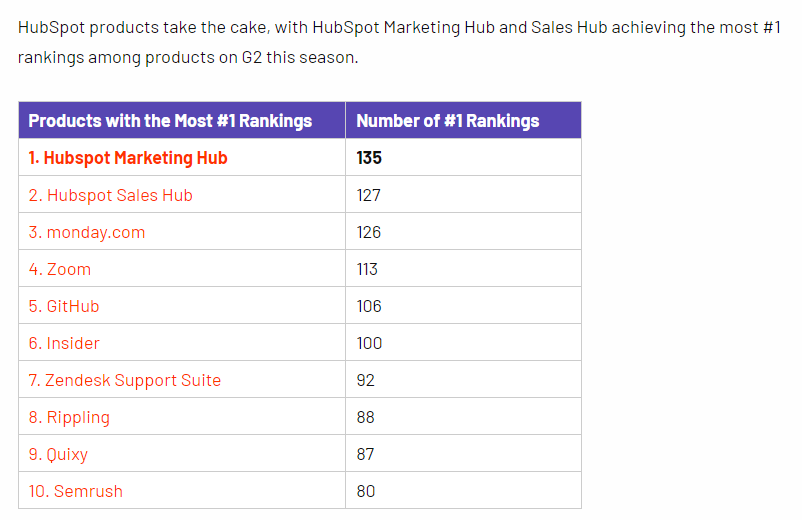

G2

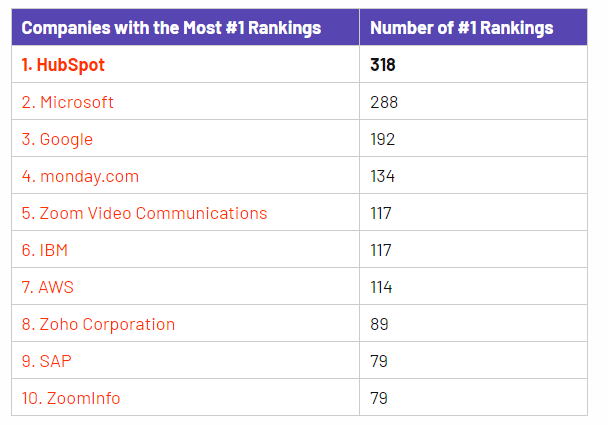

As far as customer satisfaction, any SMB focused business will have higher churn. Despite HubSpot’s leadership in the market, its gross retention is only in the high-80’s% range historically. This shouldn’t distract from some of the impressive accolades the company has achieved. It was the #1 ranked CRM by G2 last year, the #1 ranked content management system, the #1 global software company, and the most total #1 industry rankings in the G2 report.

G2

G2 gathers customer reviews from its site and other sources and applies an algorithm which ranks the data based on public versus anonymous, recency, amount of data in the review, and other factors to determine its scores. You can read more here, it’s an interesting way to see how software offerings are faring in the market.

With that, despite the lower gross retention rate, net revenue retention was around 107% last year. This won’t compete with the top companies in the space, and it likely never will. However, managing to continue increasing overall customer spend despite the inherently higher churn is a bright spot for the company.

Recent Results and Projections

Company Presentation

Recent earnings came back surprisingly strong. Management cited longer deal-cycle times and macroeconomic pressure, but that didn’t keep them from increasing customers 24% to over 167,000. With those customer adds, there was an uptick in 3 and 5 hub deals, and increasingly more traction in upmarket deals (deals closer to the 2,000 employee level). Revenues grew 35% constant currency, or 39% for the full year, average subscription revenue per customer rose 9% to $11,200, and International outpaced domestic. HubSpot’s revenue split today actually leans 53% international, which exposes the company to currency fluctuations but shows the widespread success of its offerings.

Management is guiding for $2.05-2.06B in revenues in 2023, or 19% growth at the mid-point, and improving operating margins through the year off some cost-saving initiatives. I think they are set to under-promise and overdeliver, however. Some commentary in the Q&A phase of the earnings call showed guidance was set to be reached even if the environment worsens, so even just stable pressures could keep the company in the 20%+ growth range.

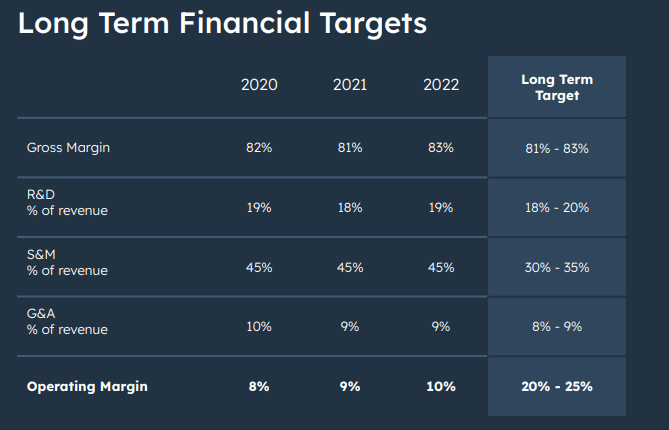

Longer-term, the company is working to develop traction in B2B commerce with HubSpot Payments, and continuing to expand offerings. Operating margin targets in the 20-25% range appear achievable as growth slows down and the company can scale back S&M spend. I expect growth to continue well into the medium-term before the company hits saturation. However, the difficulty will lie in any attempts to move upmarket to the Enterprise level in the longer-term. The major competition faced in that cohort would be difficult to break into.

Margins and Cash Flows

Company Presentation

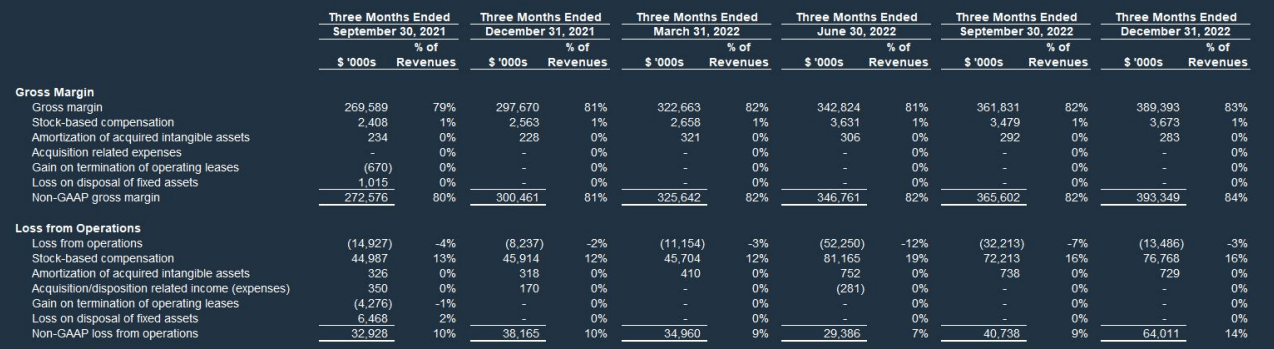

Operating margins have moved in the right direction, but we are still in non-GAAP land. Adding in share-based compensation at 16% of revenues, and it’s well into the red. This is commonplace, and it does allow for these companies to be cash-positive as they dilute the share base through employee pay. However, from an economic standpoint, it’s still a business expense and shareholders should look at is as such. That SBC figure has grown right along with revenues and actually creeped up from 13% to 16% over the past several quarters.

Based on the macro environment, however, the company is taking actions to right-size expenses. Headcount grew faster than revenues (makes sense looking at SBC/Rev) and HubSpot initiated a 7% workforce reduction (around 500 employees). Additionally, considering the hybrid work environment, the Cambridge headquarters will be consolidated to save on office costs. Although the restructuring will cost between $72-105M this next year, it’s good to see the company paring back expenses and I look forward to real profitability in the future.

The frustration is in the excessive spending in the first place. Cloud software companies in general are not excellent stewards of capital, and excessively increasing the workforce just to cut 500 jobs is value destructive, disregarding the human element. Because the majority of the charges will be booked in the first quarter, operating margins are projected to increase into the back half of the year to the high teens on a non-GAAP basis.

With $1.5B in cash on the balance sheet and positive free cash flow, the financial position is sound for HubSpot to continue investing where appropriate.

Valuation and Operating Metrics

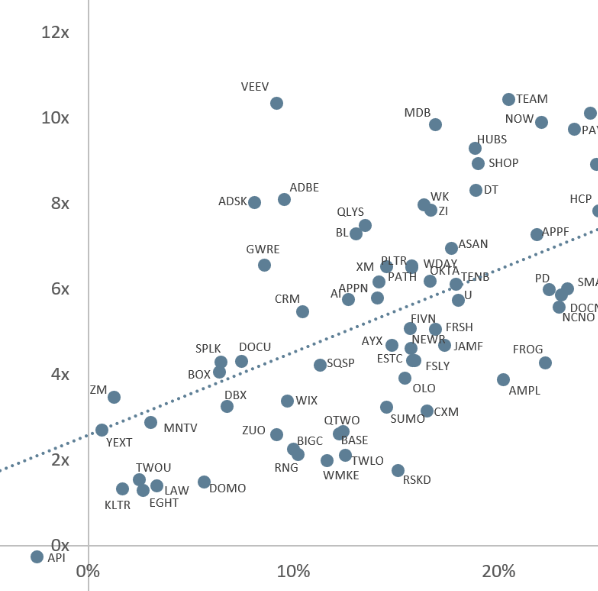

Clouded Judgement Substack

The graph above shows the EV/next 12 months revenues multiple on the Y-axis and expected revenue growth percentage on the X-axis. This displays where the companies across the cloud sector fall out in valuation compared to growth. Typically, I’ve favored the more expensive companies as nearly any truly profitable cloud company is assigned a premium. Looking above, HubSpot is growing at about the same rate as Shopify and is trading in a similar range, as well. It’s not cheap, by any means, at around 9X forward sales.

Clouded Judgement Substack

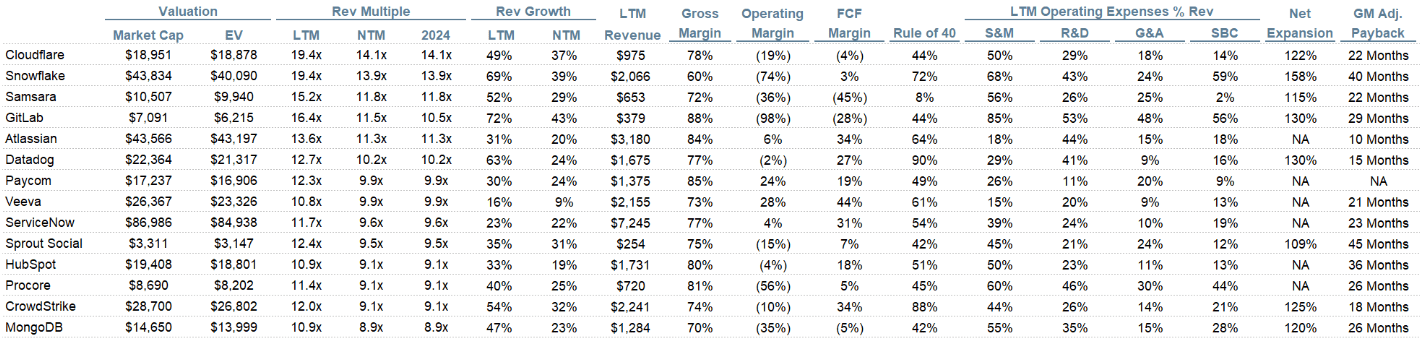

S&M expenses at 50% of revenues are on the higher side of average, but not out of the box. G&A is in a great spot, which is good to see considering it doesn’t typically add value to the company’s growth. Lastly, R&D is low compared to many other companies in the sector, despite HubSpot’s ability to churn out new organic offerings every few years. This solidifies to me the company has nurtured an innovative culture.

They easily hit the rule of 40 at 51%, and the GAAP operating margin at -4% is actually in a pretty good spot looking across the sector. SBC is also well in-line with the average.

In all, HubSpot has built itself a remarkable niche in the SMB cohort. The company will always face higher churn, but its products are differentiated and continuously improving and expanding. Revenue growth remains strong despite the difficult macro environment, management is taking steps to reduce expenses, and the future is bright. Despite a few warts, I think HubSpot has cultivated an innovative culture that should propel it forward to continue gaining share. Maybe the big dogs should fear HubSpot vice the other way around. HUBS stock is a buy.