Helix Energy: Market Banking On Strong Demand To Continue In 2023. (NYSE:HLX)

Dilok Klaisataporn

Intro

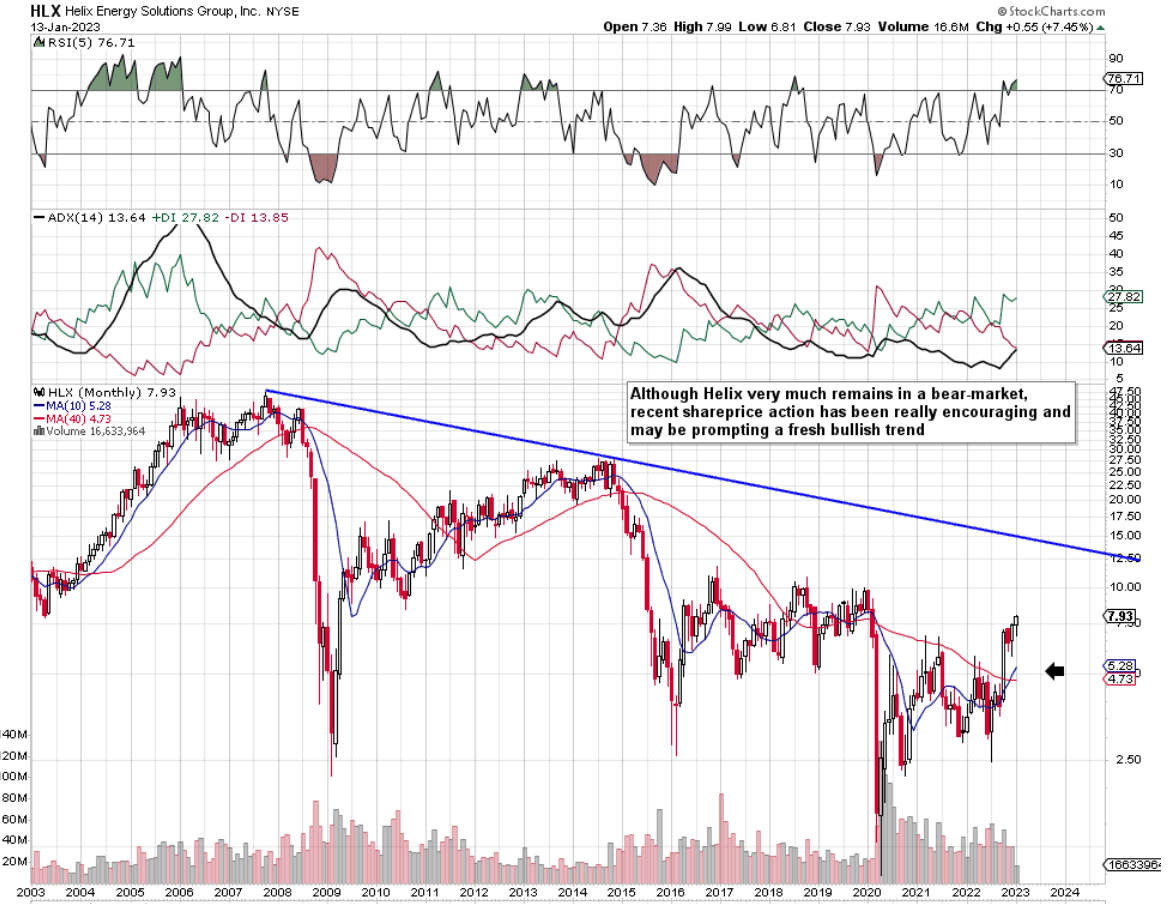

If we pull up a long-term chart of Helix Energy Solutions Group (NYSE:HLX) (Oil & Gas Equipment & Services), we can see that shares have definitely underperformed over the past 15 years. The pattern of sustained lower lows and lower highs have been par for the course for well over a decade resulting in very poor shareholder returns. This can be seen by the deterioration of bottom-line profits where the present net profit actually comes in at a negative $116 million over the past four quarters. Suffice it to say, shares of Helix Energy remain in a bear market and will remain so until the stock’s down-cycle long-term trendline gets taken out with conviction to the upside.

The encouraging news however from a technical standpoint is, due to the 200%+ move in Helix stock over the past 6 months or so, the company’s 10-month moving average has crossed above its corresponding 40-month average and is now trading near its 52-week highs. Suffice it to say, if momentum can continue here, there is a distinct possibility that shares can rally back up to at least test overhead long-term resistance. To decipher whether this is a possibility, the relationship between the company’s profitability (with an emphasis on forward-looking earnings growth), as well as its valuation, can provide us insights into the upside potential of Helix at this present moment in time.

Helix Energy Technical Chart (Stockcharts.com)

Profitability

Although Helix missed its GAAP estimate in its most recent third quarter (EPS of -$0.12 per share), profitability metrics are definitely improving when we look at adjusted numbers or free cash flow for that matter. Adjusted EBITDA almost hit $53 million in Q3 with free cash flow almost reaching $22 million. That negative GAAP number however resulted in a net loss of -$18.8 million for the quarter. Although profitability is improving (where a positive net profit number is finally expected in Q4), we like our stocks to have trailing profits for the following reason.

Significant cash flow can be generated in a myriad of ways even when starting off a standing start with negative net income. The biggest addition invariably to Helix’s net profit on the cash flow statement is depreciation which essentially is a non-cash cost. However, when we see a company that can consistently generate solid cash flow off negative earnings in an environment of declining debt and a solid float, it usually means equity on the balance sheet has been dialed down and that seems to be the picture here. Over the past four quarters, Helix’s shareholder equity has dropped from $1.669 billion to $1.481 billion as retained earnings have declined and liabilities have increased at the firm.

Obviously, bulls will argue that strong earnings growth will stop the company’s declining book value in its tracks and this may very well be so. GAAP earnings next year are expected to come in at $0.25 per share which if met would be a significant $0.77 per share increase over what is expected in fiscal 2022. However, the CEO said the following on the company’s recent third-quarter earnings call. Notice how he implied that there were no guarantees that the insatiable demand which is currently present in the marketplace will continue indefinitely.

The rate that demand rose in 2022 was dramatic, but we all know that the market can collapse just as rapidly. Our strategic goal remains to manage the balance sheet, maintaining the capacity to cash settle our 2026 converts should the capital markets warrant. For the foreseeable future, we anticipate Helix will be meaningfully free cash flow positive. Ahead of this ongoing demand increase, it’s our intent to add incrementally to the 3 legs of our energy transition model of, number one, maximizing remaining reserves; two decommissioning; and three, renewables, specifically offshore wind.

Valuation

Helix Energy Solutions Group presently trades with a book multiple of 0.81, a sales multiple of 1.59, and a cash flow multiple of 59.42. Although these multiples may look low on the surface, the company’s assets as well as its sales still come in more expensive over the stock’s 5-year averages (0.59 & 1.19, respectively). Remember assets and sales are essentially what causes earnings and cash flow growth which means investors need to size up whether Helix Energy’s current profitability justifies the stock’s valuation.

Conclusion

Therefore, to sum up, shares of Helix Energy Solutions Group have been on the rampage since July of last year as forward-looking earnings revisions continue to impress. With equity though on the wane and shares looking only fairly valued, Helix Energy Solutions needs sustained demand to continue for its services to keep shares rallying higher. We look forward to continued coverage.