Google Q3 2022 Earnings Indicate Hold (NASDAQ:GOOG)

JHVEPhoto

Growing up in North Jersey, from time-to-time I used to hear my parents, aunts and uncles use the phrase, “Wise up!” It was both encouragement and admonishment.

Within this context, I offer my current thoughts to you regarding Alphabet Inc. (NASDAQ:GOOGL) (NASDAQ:GOOG), the company and the stock.

Opening Premise

Alphabet is an outstanding corporation, enriched by brilliant management, staff, and intellectual property. However, this does not mean the business can defy the law of gravity.

In recent quarterly earnings reports, especially the 3Q2022 release, I came away thinking, “Management doesn’t seem to get it.”

Having a 40-years’ experience in the energy business, it is well understood ours is a cyclical industry. During times of economic uncertainty, management pulls in its horns and hunkers down to weather the storm.

During these periods, reducing opex, capex, and headcounts is normal. Afterwards, as the storm subsides, things return to a more normal run-rate, selected investments pay off, and profitability rises smartly.

I have to wonder how much direct experience Alphabet’s management has had when times get tough. From looking at the numbers and senior leadership’s the question is called.

Let’s Look at Some Numbers

First, The Top Line

Here’s a FUN Graph illustrating FY2017 to 2021 total revenue growth.

FAST Graphs

Revenue growth averaged just under 24 percent a year. That’s very good for a mega-cap company like Alphabet.

We see revenue growth decelerated a bit in 2020 (pandemic related) but bounced back in 2021. If we combine 2020 and 2021, it smooths out to nearly the same 20-something percent growth rate for 2017 through 2019.

How are things going in 2022?

Through the first three quarters, Alphabet generated $206.8 billion top line revenue. That’s a 13.4 percent improvement versus the same period in 2021.

Given 2021 was an exceptional year, and the fact Alphabet is facing currency headwinds in 2022 (management expects these to get worse in Q4), the top line is acceptable. Low-to-mid teens sales growth seems pretty solid.

What About the Bottom Line?

Let’s run through the same exercise for net operating income. Alphabet management has long touted operating income growth. That’s their call, their go-to metric, and I’m onboard with it.

Here’s another FUN Graph illustrating FY2017 to 2021 operating income (EBIT) alongside revenue growth from the earlier chart.

FAST Graphs

Note how operating income grew even faster than revenue. That’s very good. It means management was leveraging incremental revenue into higher EBIT margins.

What about this year?

Through 3Q2022, total operating income totaled $56.7 billion. That’s FLAT versus the same period in 2021. Zero growth.

So, we have acceptable YoY sales growth opposed to flat operating income.

To put an exclamation point on it, operating income has declined in each of the three succeeding quarters of 2022.

That’s not good.

Question: What’s Causing the Problem?

Answer: opex and headcount. Management has a say in each of these components.

Here are some data points.

Alphabet Inc — Operating Expenses and Headcount

|

1Q2022 |

2Q2022 |

3Q2022 |

2022 v 2021 |

|

|

Opex |

18.3 |

20.1 |

20.8 |

Up 24% |

|

Headcount |

163.9 |

174.0 |

186.8 |

Up 25% |

source: Alphabet quarterly earnings reports

Operating expenses include research and development, sales and marketing, and general and administrative. Headcount in self-explanatory.

These growth rates are higher than the years’ 2017 to 2020.

What we are seeing is a management team that despite revenue growth deceleration, a difficult macro-economic climate, and QvQ advertising revenue decline; continues to keep pedal-to-the-metal re opex and headcount.

Wise up.

Cash Flow Isn’t Any Better

It’s fair to say Alphabet may be better measured on cash generation than profits. But the cash generation story isn’t any good, either.

Through the first three quarters of 2022, operating cash flow is less than two percent better than 2021.

To make matters worse, free cash flow DECLINED 9 percent.

Why has FCF gone into the red? Same old story.

Alphabet Inc — Capital Expenditures

|

1Q2022 |

2Q2022 |

3Q2022 |

2022 v 2021 |

|

|

Capex |

9.8 |

6.8 |

7.3 |

Up 29% |

Pedal to the metal. Operating cash flow barely moving yet full-press capex spend.

Would you be surprised to know year-over-year stock-based compensation is up 16 percent? Or balance sheet cash and securities are down 17 percent?

Wise up.

What Did Management Have to Say?

Now the narrative gets more interesting. I offer several excerpts for your perusal; though I encourage you to read the entire 3Q2022 transcript for additional perspective.

Remarks by CEO Sundar Pichai

Our Q4 headcount additions will be significantly lower than Q3. And as we plan for 2023, we’ll continue to make important trade-offs where needed and are focused on moderating operating expense growth. Obviously, as a company, over time, we’ve had periods of extraordinary growth, and then there are periods where I viewed it as a moment where you take the time to optimize the Company to make sure we are set up for the next decade of growth ahead. I view this as one of those moments. It gives us a chance to make sure we are with clarity identifying what are the most important areas and making sure we are directing our incremental investments towards those and as well as where we can realign.

Author comment: headcount additions will be lower? Moderating expense growth? It appears heading into 2023 the approach is to reduce the rate of spending growth (of which little to no restraint is yet evident in 2022). There was no dialogue about when operating income and free cash flow will return to growth.

Remarks by CFO Ruth Porat

With respect to Alphabet headcount, we added 12,765 people in the third quarter, including more than 2,600 of those joining Google Cloud as part of our acquisition of Mandiant. As in prior quarters, the majority of hires were for technical roles. In the fourth quarter, we expect headcount additions will slow to less than half the number added in Q3. Within this slower headcount growth, next year, we will continue hiring for critical roles, particularly focused on top engineering and technical talent. Turning to CapEx, we continue to make significant investments in technical infrastructure with servers as the largest component.

Author comment: Alphabet added 12,765 people in the third quarter. In the current quarter, the new hires will be reduced to about 6,000 (sans any Mandiant acquisition). Should I feel good about that? And turning to capex: there will be ongoing “significant” investment? Sounds like they’re putting the hammer down.

Conference Call Q&A

Here are 3 selected conference call questions and answers between analysts and Alphabet management:

Q. Sundar [Pichai], just to go back to the comment about earlier in the quarter, becoming 20% more efficient. I thought tonight, your comment on investing responsibly over the long term of being responsive to the environment is helpful. If I look at sort of the Excel sheet, I think you’ll have added about 51,000 new people to the company since the start of last year. Can you give us some examples of internal KPIs or quantifiable analysis you’re running just to ensure you’re generating ROI for investors from all your hiring as you sort of run through these analyses?

A. Brian, I think — look, I think we gave some — we’ve been clear that we are going to moderate our pace of hiring going into Q4 as well as 2023. I think we are seeing a lot of opportunities across a whole set of areas. And every time, talent is the most precious resource, so we are constantly working to make sure everyone we’ve brought in is working on the most important things….

Author comment: That’s a non-answer.

Q. And then Ruth [Porat], on the cost side, I understand the comments. I understand the comments about the headcount adds and what you plan to do in the fourth quarter. But could you talk about non-headcount-related costs and the opportunity you see or the need you see for managing those down? And do you see that there are significant opportunities to do that as well. So again, non-headcount costs. Thank you very much.

A. There are, obviously, to your question, non-payroll-associated expenses that also then attach. And so an operating environment like this adds urgency to prioritization. We want to make sure we’re using all resources as effectively and efficiently as possible. At the same time, as we’ve tried to be very clear, there are very exciting areas that we will continue to invest in.

Author comment: Sounds like full tilt; we’re plowing ahead come hell or high water.

Here’s another question fielded by CEO Ruth Porat:

Q. Capex is up 31% year-over-year. Can you talk about a little bit what’s driving that and can that be pulled back a bit? Is that Cloud or really building out the AI capabilities?

A. The majority of CapEx does continue to be for our technical infrastructure. And as we’ve talked about on prior calls, servers really has been the largest driver of the investment dollars. The technical infrastructure team has consistently focused on levers to improve utilization and efficiency and they continue to do so. We are investing, to Sundar’s comments, in building out the compute in support of all that we’re doing with our AI teams and are excited about that. And obviously, you had seen some more activity earlier in the year regarding real estate. We feel good about where we are. We’re continuing to fit out our offices, et cetera, for utilization in this new return to hybrid work environment, but we’re trying to make sure that we’re doing that at an appropriate measured pace, and that’s really it.

Author comment: Ruth Porat is a remarkable manager. Yet frankly, her answers appear tone-deaf. Management is being asked directly about reducing costs and the answer appears to be, “No.” And there’s no follow-on about when profits or cash flows will return to growth.

Wise up.

Summary and Observations

IMHO, the numbers and associated management commentary implies they do not see the need to reduce or reset costs, expenses, or hiring.

I could find no commentary or guidance about how or when management expects operating income or cash flow to return to growth.

Alphabet stock has no yield support.

SBC (stock-based compensation) continues to climb.

Two of Alphabet’s three business segments (Cloud and Other Bets) are losing money.

Readers, from my experience, during times of economic uncertainty and rising interest rates, I believe it’s prudent to pull back a bit, re-evaluate, and enact course corrections as appropriate for the situation.

Alphabet management appears unwilling to do so; even in the face of point-blank queries. I am disappointed with what appears to be management hubris. Stockholders often pay the price.

Most industries recognize when the macro turns, it’s time to pull in your horns and explain how you’re going to cut spending and run for cash flow / profits in the face of it.

Given the backdrop to date, can Alphabet defy gravity? I haven’t seen many businesses that do.

As a long-term GOOGL stockholder, I plan to hold the stock, but do not see the recent share price drop as an opportunity. Indeed, given management’s remarks coupled with recent financial results, I see more of a threat.

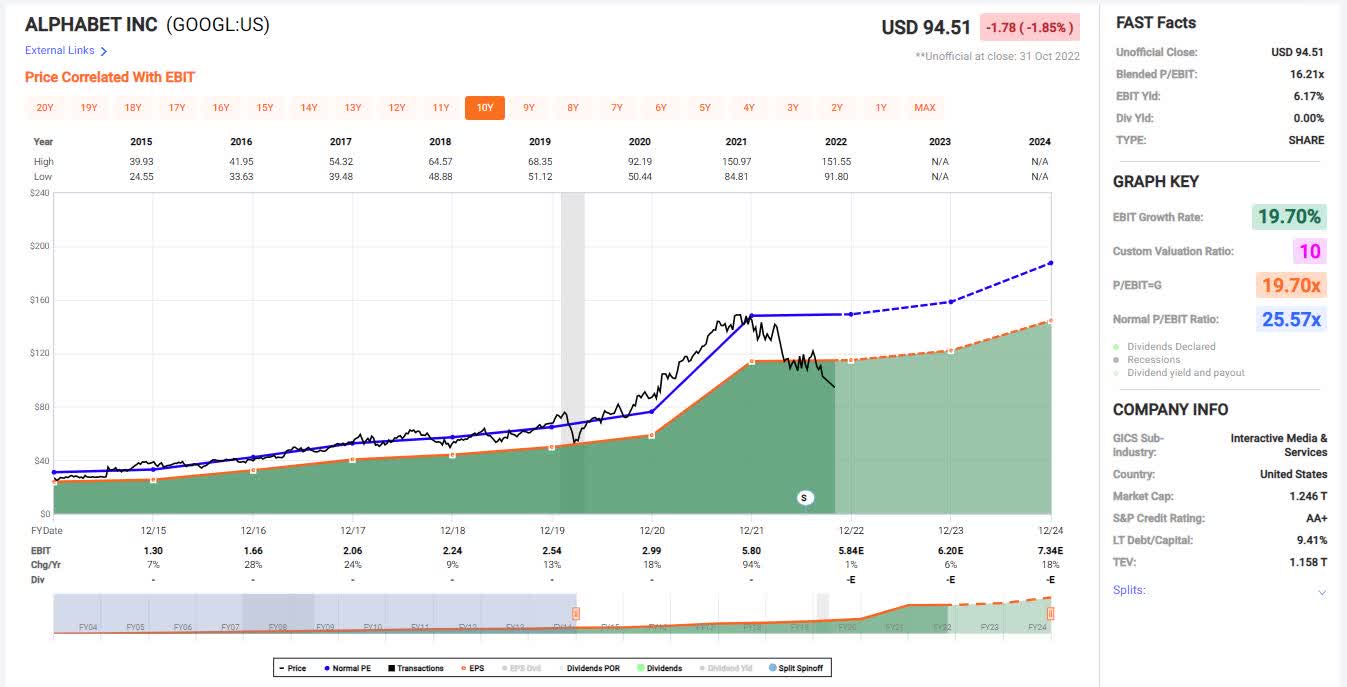

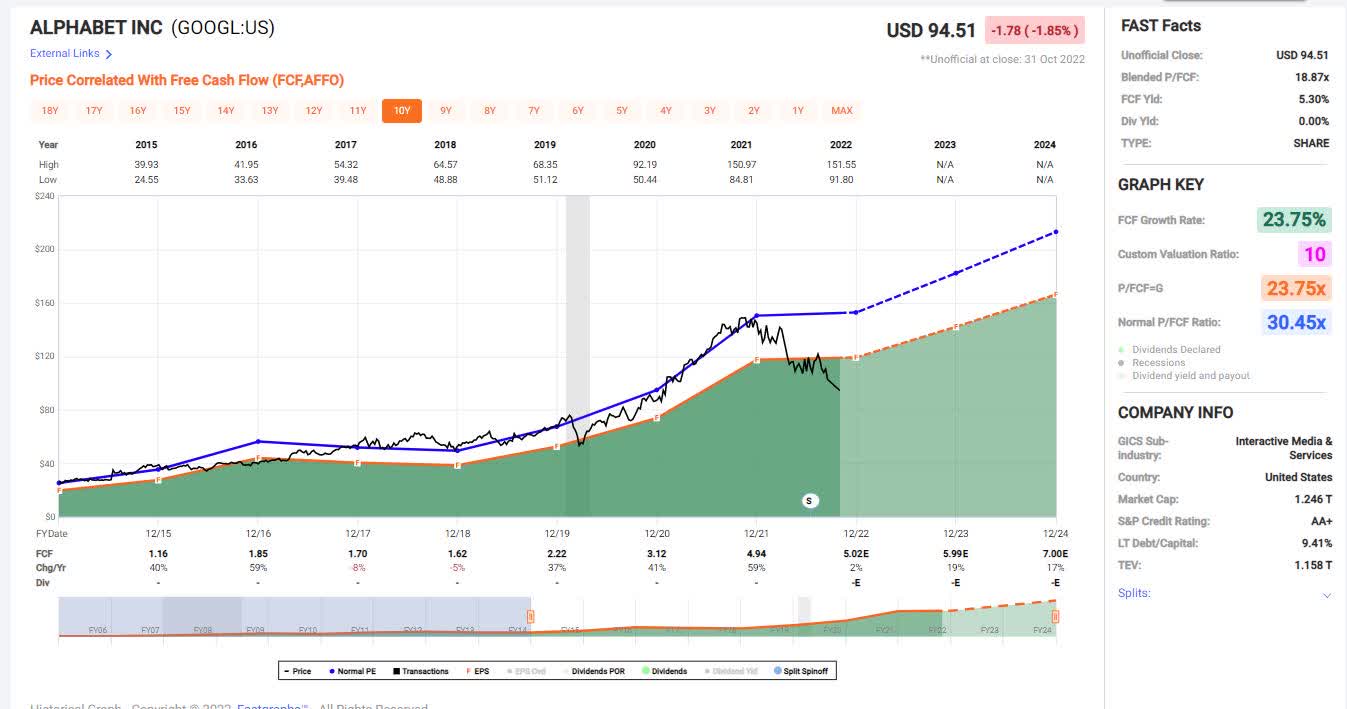

Please see the two FAST Graphs below. The first reflects a long-term relationship between price-and-EBIT and the second chart price-and-free cash flow.

FAST Graphs FAST Graphs

Despite the charts suggesting Alphabet stock is undervalued, I question whether Mr. Market’s previously generous valuation multiples (26x and 30x for EBIT and FCF, respectively) will remain intact until management demonstrates a return to historical growth rates. Prior long-term growth rates for these key metrics were 20 percent and 24 percent.

During choppy or outright bear markets, investors often elect to compress valuation multiples; sometimes significantly and sometimes for an extended period of time. Indeed, the longer it takes to right the ship, oftentimes the more the Street gets into a “show me” mode.

Alphabet is blessed with some of the best and most brilliant management on the planet. But do they have a blind spot? If not, senior leadership needs to get some old-time religion and get it fast.

Warning to other mega-cap Big Tech firms like Amazon.com, Inc. (AMZN) and Meta Platforms (META): take heed. You’re in the same church, just a different pew.

Please do your own careful due diligence before making any investment decision. This article is not a recommendation to buy or sell any stock. Good luck with all your 2022 investments.