GDX: Extremely Overvalued Even At These High Gold Prices (NYSEARCA:GDX)

mikulas1

The VanEck Vectors Gold Miners ETF (NYSEARCA:GDX) has benefitted from the rise in gold prices over the past few weeks amid the sharp drop in interest rate expectations. However, even at current gold prices the GDX is overvalued, and gold prices face asymmetric downside risks from still-high real interest rates and falling commodity prices. The ETF remains a sell in my view until we see a sharp fall in prices or reason to believe gold prices can continue to rise.

The GDX ETF

The VanEck Vectors Gold Miners ETF tracks the performance of the NYSE Arca Gold Mining Index. Newmont (NEM) has the largest weighting on the index at 11%, followed by Barrick Gold (GOLD) which has a 9% weighting. The dominance of these two stocks has declined significantly over the past year, particularly in the case of Newmont, which has seen a sharp drop in valuation. However, the surge in Newmont’s dividend payments over recent years mean this single company is responsible for half of the dividends paid by the underlying Gold Mining Index. Even after seeing dividends rise across the sector, the GDX’s still only pays a dividend yield of 1.5%, which is slightly below the index’s 2.2%. The GDX charges an expense ratio of 0.51%, which also acts as a meaningful drag on long-term returns.

Extremely Overvalued Even At These High Gold Prices

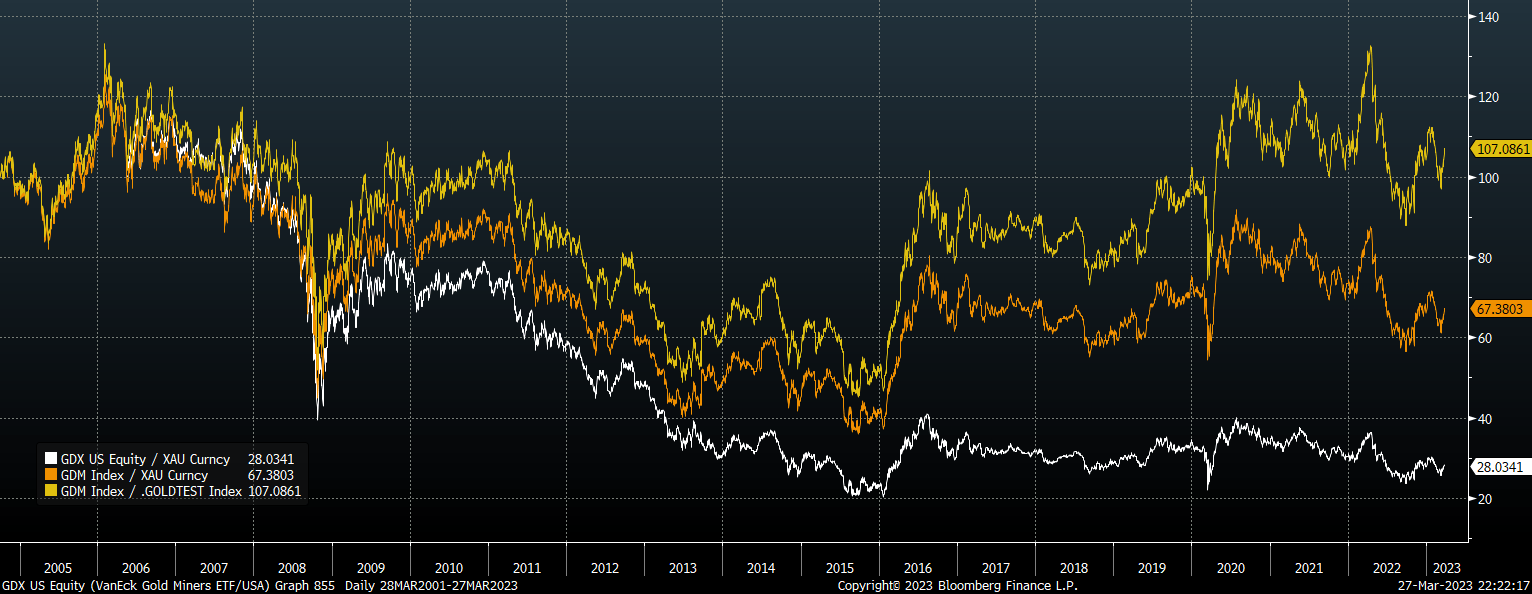

I have seen numerous charts over recent years that seek to show how the GDX is extremely undervalued relative to gold prices. Most of these show a simple ratio of the GDX over gold prices which displays a major declining trend (the white line in the chart below) and leads to the conclusion that at current elevated gold prices, gold stacks are undervalued. The problem with this analysis is that it fails to take into account the huge share issuance across the mining sector that has undermined earnings per share even as nominal earnings have risen.

White Line: GDX vs Gold; Orange Line: GDM Market Cap vs Gold; Yellow Long: GDM Market Cap vs Real Gold Price (Bloomberg)

If we instead look at the market cap of the underlying ARCA Gold Miners Index, this correlates much more closely with gold prices, and is much less undervalued based on the relationship seen over the past 18 years. If we look at the ratio between the market cap of the gold mining index to the inflation-adjusted gold prices, which takes into account the tendency of rising wages and input costs to depress gold miners’ earnings, the undervaluation disappears entirely as shown in the yellow line above.

This overvaluation is also reflected in the PE ratio of the index, which has risen to 28.9x following the recent rally. Even with an expected earnings increase of 28% over the next 12 months the forward PE ratio is still a lofty 22.5x. These ratios actually paint a rosy picture of the mining sector’s true valuation. When we adjust trailing earnings for extraordinary items, the PE ratio rises to 39.9x, and when we look at free cash flows, the ratio rises to a shocking 59.3x. Capital expenditure has far outstripped operating cashflow growth over the past four-year gold price rally, causing free cash flows per share to stagnate.

Gold Price Reversal In The Offing

If gold prices remain at current levels in real terms, we should expect the GDX to underperform gold prices by a few percentage points per year as has been the long-term story for this ETF. The main risk, however, comes from a sharp reversal in gold prices, which could cause a major drop in gold mining stocks.

As I recently argued in ‘Deflation Risks Suggest Gold Is No Safe Haven‘, the price of gold is extremely detached from its main historical driver – US10-year inflation-linked bond yields. This can be seen in the chart below which compares the real gold price with 10-year real yields. Even as rising inflation has put persistent downside pressure on real gold prices, the metal is trading far above where its correlation with real yields would suggest.

Inflation-Adjusted Gold Price Vs 10-Year TIP Yield (Bloomberg)

We can draw a similar conclusion about gold when comparing the ratio of the industrial metals index over gold with 10-year bond yields. Based on current yields, the industrial/precious metal index should be trading around half current levels. Of course, this decoupling could re-emerge in the form of higher industrial metals prices and lower bond yields, but gold should face significant headwinds in their absence.

Ratio Of Industrial Metals Over Gold Price Vs 10-Year UST Yield (Bloomberg)

I have received a number of comments asking whether it is reasonable to expect the correlation between the price of gold and real yields that was in place between 2006 to 2020 to re-establish itself. It could be the case that other factors such as central bank gold demand or fears over the safety of inflation-linked bonds due to official inflation underreporting cause the gap to remain in place over the long term.

While central bank buying was the largest on record last year, it amounted to just 6% of the entire global gold market according to the World Gold Council. Central bank purchasing has rarely had an impact on the price of gold. Banks sold gold persistently during the 2000s as gold prices surged higher, and have been net buyers amid the decline in real gold prices since 2011. Regarding the underreporting of inflation, it is hard to believe that official CPI figures are overreported to any meaningful degree. Proponents of this view argue that if we used the same CPI methodology today as we did in the 1980s, inflation would have come in around 5-7pp per year higher for the past 30 years. The problem here is that double-digit average inflation over this period would mean actual US real GDP is lower now than it was in 1990, which is obviously not true.

My view is that the elevated gold price relative to its fundamentals reflects nothing more than speculative buying by investors with weak conviction reacting to the dovish shift in monetary policy. In the absence of a sharp fall in real bond yields or a surge in commodity prices generally, we are likely to see gold prices reverse their recent gains amid the increasingly deflationary macroeconomic environment.

Summary

The GDX is far from the undervalued asset that many gold bulls see it as despite its long-term underperformance versus gold prices. The ETF is extremely expensive at current gold prices and should continue their long-term underperformance. A downside reversal in gold prices, meanwhile, poses an imminent risk of a sharp drop.