FOMC Minutes: No Sign Of Rate Cuts Yet (SP500)

DNY59

The Federal Reserve released the minutes from its January 31/February 1 st meeting yesterday. The release seemed more anticipated than previous meeting minutes as investors awaited a hint at the Fed’s next move on interest rates. Markets finished the day mixed with little reaction to the minutes. Despite muted equity markets, the fixed income markets, along with a couple of Federal Reserve Board members seem poised to push interest rates above market expectations.

The Fed continues to center its policy around data related to growth, employment, and inflation; with inflation being the most important. In terms of growth, the economy continues to outperform the committee’s expectations, as noted by staff comments on page 8:

Although recent data indicated that real GDP growth in the fourth quarter of 2022 was stronger than expected, real PDFP growth was weaker than previously forecast, and the large, unexpected boost to GDP growth from inventory investment was not projected to persist. In part reflecting the lagged effects of previous monetary policy tightening, the staff still projected real GDP growth to slow markedly this year and the labor market to soften.”

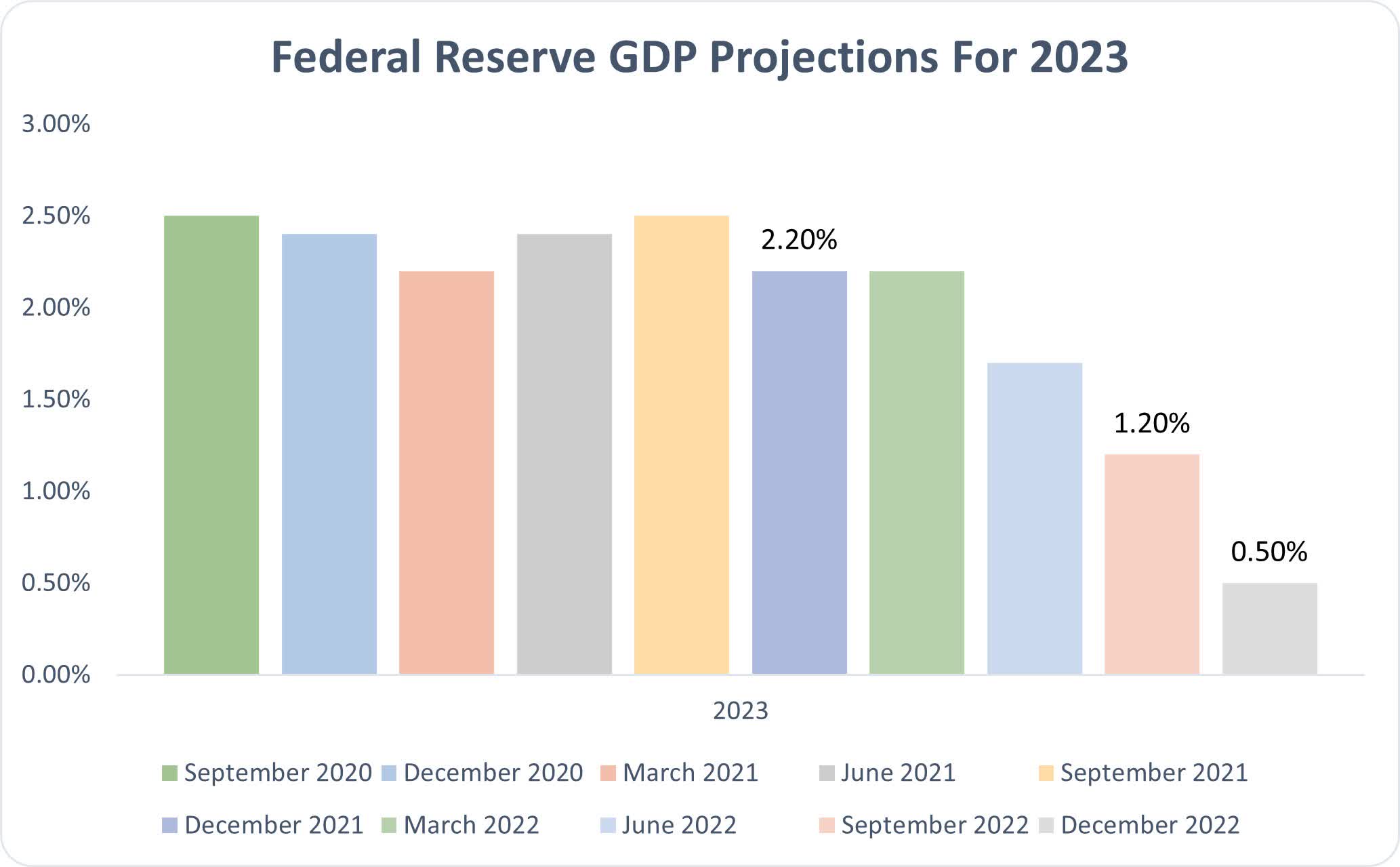

The committee is expecting economic growth to slow quickly, as indicated by December’s data points survey. In December, the Fed projected a real growth rate of 0.5% for 2023. Therefore, even if real growth hovers around 2%, the Fed’s projections indicate that it would tolerate higher interest rates in exchange for lower growth. Currently there is nothing on the data front relating to growth showing the Fed is nearly the end to its inflation fight and should Q1 GDP data not reflect the reversal of inventory investment in the economy, investors should begin to anticipate the possibility of a Fed funds rate greater than 5.5%.

Federal Reserve Estimates

For employment, a key comment stood out that showed the unemployment rate may end becoming a lagging indicator of this business cycle:

A few participants remarked that some business contacts appeared keen to retain workers even in the face of slowing demand for output because of their recent experiences of labor shortages and hiring challenges.”

If true across the economy, the idea of keeping employees for fear of facing the labor force shortage would represent a fundamental shift in the employment market. This shift would make it harder for wage increases to mitigate towards historical norms and keep upward pressure on prices.

For inflation, the committee made what I found to be the most difficult statement in the 13-page document:

Participants agreed that they had observed less evidence of a slowdown in the rate of increase of prices for core services excluding housing, a category that accounts for more than half of the core PCE price index.”

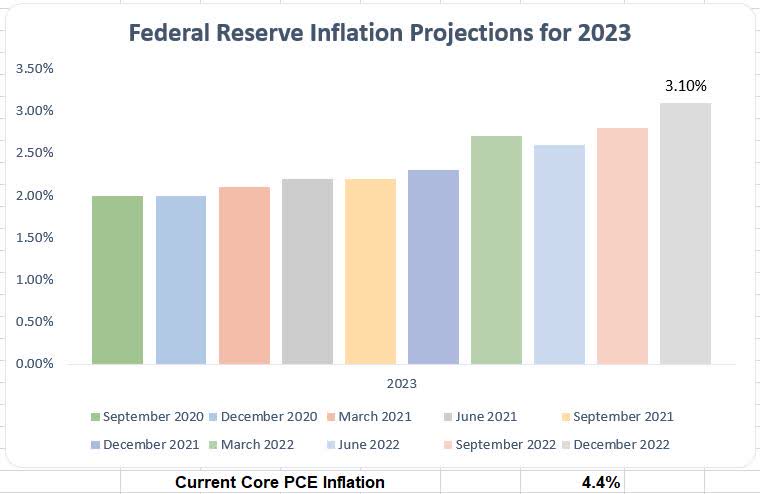

The core PCE (personal consumption expenditures) growth is the stat used by the Fed to gauge inflation. Currently, core PCE stands at 4.4% (January’s data has not been released yet), down 100 basis points from a cycle high of 5.4%, but 240 basis points shy of the Fed’s 2% target. If service pricing cannot decline, there’s no way core PCE will fall to the Fed’s projection of 3.1% in 2023 followed by 2.5% in 2024. Further rate hikes may be needed to accomplish this.

Federal Reserve Estimates Federal Reserve Estimates

While the committee opted to raise the Fed funds rate by 25 basis points, the discussion of a 50 basis point hike did occur:

The participants favoring a 50-basis point increase noted that a larger increase would more quickly bring the target range close to the levels they believed would achieve a sufficiently restrictive stance, taking into account their views of the risks to achieving price stability in a timely way.”

These sentiments were shared publicly by a couple of Fed officials. The morning prior to the release of the minutes, James Bullard told CNBC that he felt faster rate hikes were more warranted and that by doing so, the Fed had an opportunity to defeat inflation in 2023. Last week, Cleveland Fed President Loretta Mester stated there was an economic case for raising Fed funds rates by 50 basis on February 1 st, but she did not want to surprise the markets. Since the Fed does not exist to appease equity markets, if more members become impatient with the progress, a surprise may be coming.

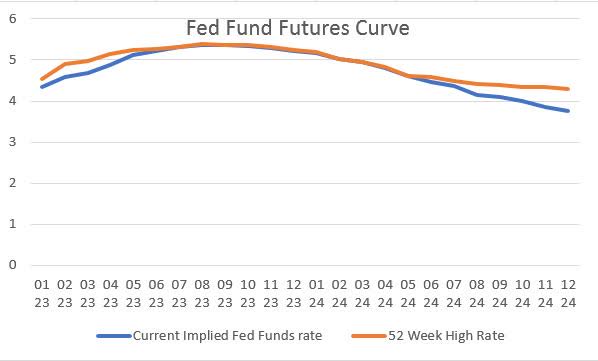

While equity markets have had one day of selling and a mixed day this week, the fixed income side appears poised to price in additional Fed increases. Fed funds futures from this July through May 2024 priced all-time highs on Tuesday and Wednesday, pointing to a terminal Fed funds rate of 5.36% in August and September of this year. The Fed funds futures curve is also closer resembling the December projections released by the Fed for rates in 2023 and 2024.

Barchart Barchart and Federal Reserve Estimates

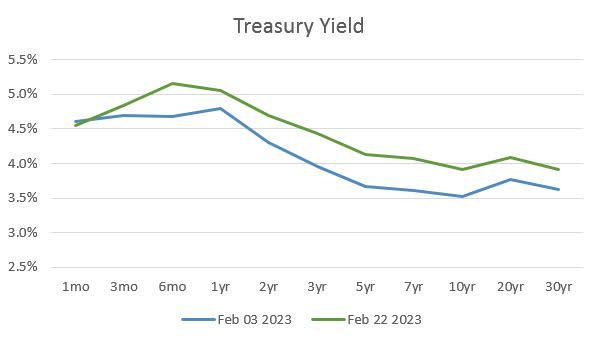

Additionally, the Treasury yield curve has seen broad interest rate increased since February 3 rd. In that short time frame, most durations of Treasury bonds have seen their yields increase between 30 and 50 basis points. Interestingly, the front end of the yield curve has seen a pronounced steepening, with the difference between 1-month and 6-month Treasury yields widening from 7 basis points to 60 basis points in 19 days.

FRED FRED

Overall, there’s nothing in the Fed minutes that states we’ve reached the terminal Fed funds rate or that the end of the inflationary battle is here. In fact, public comments from Fed officials discussing 50 basis point rate hikes show that the March surprise may be that versus no changes. The March meeting now looms large as it represents an uncertainty in immediate policy decisions and an update in Fed economic projections. I’m continuing to find high-quality credit with a short term duration to store my cash away until a larger re-pricing event happens.