FLIN: Ride The Indian Growth Story At A Low Cost (NYSEARCA:FLIN)

da-kuk

As global markets come to terms with the fallout from the banking turbulence in the US and Europe, India hasn’t been spared, with the financials-heavy Franklin FTSE India ETF (NYSEARCA:FLIN) portfolio down on the news. In contrast with the capital position of the troubled banks overseas, however, Indian banks have resilient balance sheets and, per their stress test results, maintain ample buffer in hand. Yet, Indian equities could still feel the effect of contagion from the US, with the knock-on effect of slower lending and weaker global demand likely also to weigh on overall growth. Offsetting the external headwinds is the boost from the expansionary Union budget this year, led by significantly higher capex spending, as well as a slowdown in overall inflation. Alongside the favorable long-term demographic tailwinds, India still has a long runway to grow its economy for the coming decades and should quite easily avoid a recession scenario anytime soon. As one of the lowest-cost vehicles available to access Indian equities, FLIN remains a great way to ride the growth story.

Fund Overview – One of the Lowest-Cost Vehicles for Indian Exposure

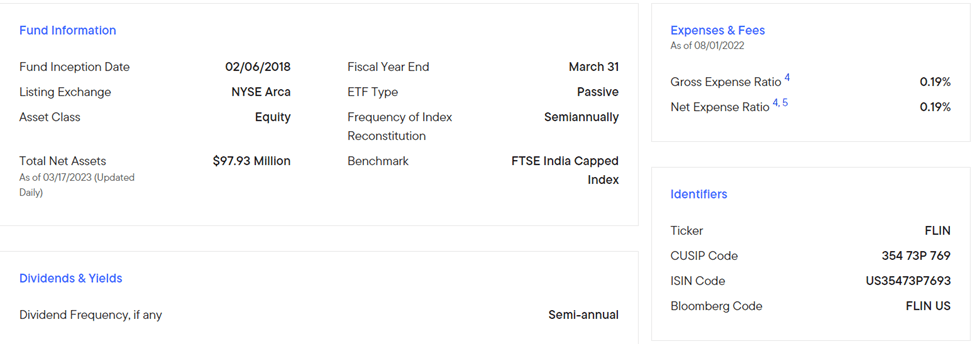

The US-listed Franklin FTSE India ETF seeks to track, before fees and expenses, the performance of the FTSE India Capped Index, a free-float adjusted market cap-weighted index that limits single-stock exposure up to 20% in line with the ‘Regulated Investment Company’ (RIC) concentration requirements for US registered funds. As a subset of the FTSE Global Equity Index Series, the fund tracks the performance of Indian large and mid-cap stocks. Per the latest disclosures, the ETF charged a 0.2% expense ratio (gross and net), making it one of the lowest-cost options available to express a single-country view on Indian equities. A summary of key facts about the ETF is listed in the graphic below:

Franklin Templeton

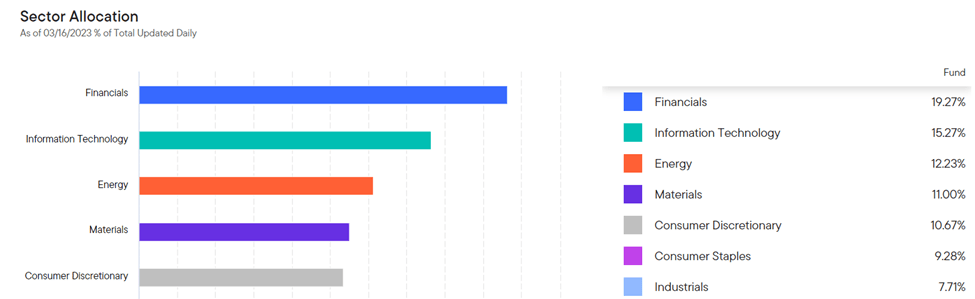

The fund’s sector allocation is well spread out, with Financials leading the way at 19.3%, followed by Information Technology at 15.3%, and Energy at 12.2%. On a cumulative basis, the top five sectors accounted for ~68% of the total portfolio.

Franklin

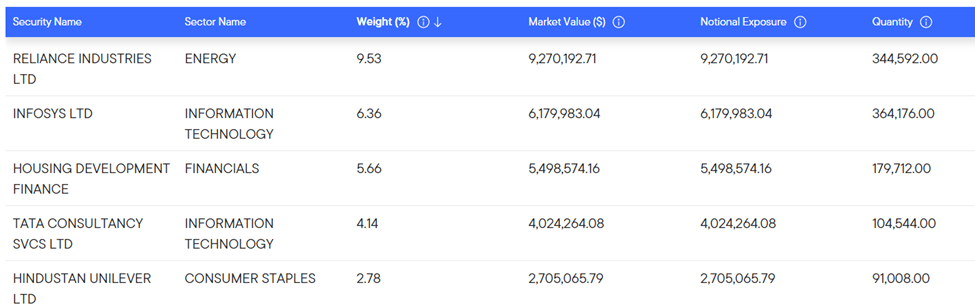

In line with the FTSE India Capped Index, the ETF is spread out across >200 holdings. The largest single-stock exposure is to Indian multinational conglomerate Reliance Industries Limited (OTC:RLNIY) at 9.5%, followed by Indian multinational information technology company Infosys Limited (INFY) at 6.4%, and Indian private development finance institution Housing Development Finance Corporation at 5.7%. The ETF also has outsized holdings in another Indian information technology services and consulting giant, Tata Consultancy Services (OTCPK:TTNQY), at 4.1%, and Indian consumer goods company Hindustan Unilever at 2.8%. The top five holdings account for ~28% of the overall portfolio, so this ETF is also well-diversified from a single-stock perspective.

Franklin Templeton

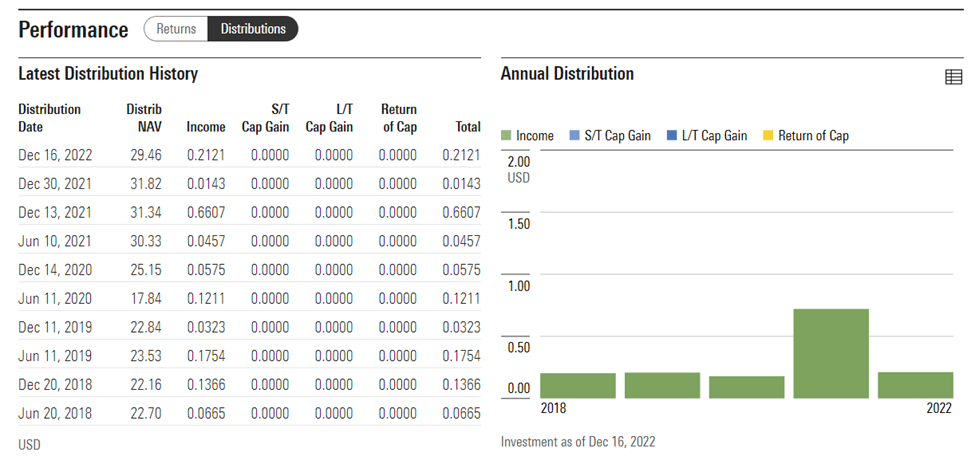

On a YTD basis, the ETF has declined by 6.9% in market price terms and 6.4% in NAV terms but has compounded at a steady ~4% pace (in market price and NAV terms) since its inception in 2018. The fund distribution runs on a semi-annual basis, with the income portion of the yield consistently running at <1%. Thus, the fund is more suited for growth growth-oriented investors looking for exposure to the Indian equity market, which typically features companies that reinvest, rather than distribute, their excess cash.

Morningstar

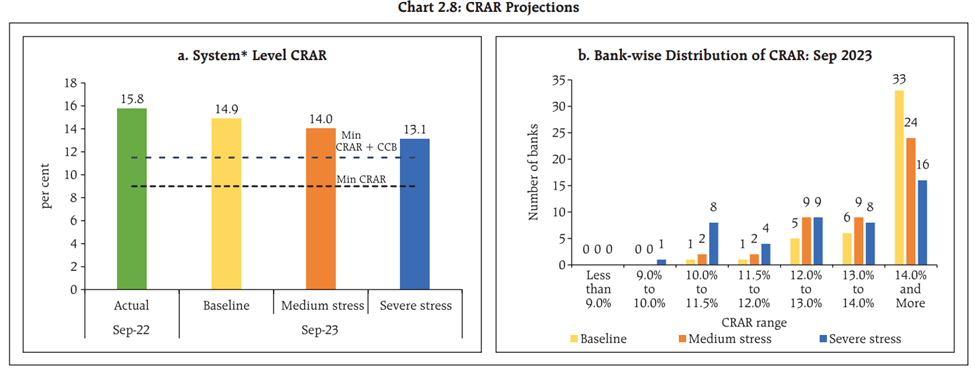

Indian Banks Sell Off but Remain in Good Health

Unlike in the US, where a handful of mid-sized banks (by assets) operate with looser regulatory restrictions, Indian banks are subject to strict regulations with regard to their capital positions and asset allocation decisions. Per the Reserve Bank of India’s latest Financial Stability Report, even under a severe stress test, major Indian banks’ capital adequacy ratios would remain well within requirements. At the system level, the capital-to-risk-weighted assets ratio (CRAR) is projected to stay at >10% under baseline, medium, and severe stress scenarios (vs. the 10% requirement). Thus, the Indian banking sector is well-insulated from any contagion effect and should remain well-capitalized even if more overseas banks fail in the coming months.

RBI

Price action in recent weeks indicates market pessimism, however, with FLIN suffering from its outsized financials exposure. Depending on the spillover effects on Indian growth from the heightened US recession risks, this presents an opportunity to buy into FLIN, in my view. On the one hand, slower lending and growth in the US will likely be a drag on global growth. But slower economic activity also raises the probability of disinflation, which should drive a looser monetary policy and global financial conditions. Plus, this year’s expansionary pre-election budget by the Indian government will see a significant rise in capex, which should support near-term GDP growth.

Added Boost from Fading Inflationary Momentum

The flip side of a lending-driven growth slowdown is the resulting disinflationary impulse, including via lower energy prices, as well as the prices of key commodity inputs throughout the global supply chain. So while India’s headline and core inflation are still running at >6%, all signs point to a continued easing in inflation this year. Barring one-offs such as a renewed heat wave or a larger-than-expected impact of El Niño on agriculture production, expect a larger disinflationary impulse going forward.

Economic Times

Thus far, the RBI has maintained a hawkish stance to address the potential stickiness of core inflationary pressures. But this was before the banking crisis; given monetary policy also works with a lag and that rates have already been hiked by a cumulative >300bps, I suspect the stance could shift to neutral to prevent an overshoot. Finally, with the core inflation momentum already easing per recent months’ reports, lower growth, and inflation, alongside tighter global financial conditions, could even accelerate a rate-cutting cycle ahead of next year’s elections. All in all, a reversion to monetary easing looks to be on the cards; in this scenario, expect a sizeable boost to equity valuations and, by extension, FLIN.

Ride the Indian Growth Story at a Low Cost

The recent turbulence in the global banking space doesn’t bode well for global growth prospects this year. There will inevitably be a knock-on effect on India’s >$3tn economy, though any impact is likely to be transitory at best given the favorable secular tailwinds underlying the country’s growth runway. Plus, the near-term uplift from this year’s pre-election budget via a step up in capex spending should help, along with the gradually fading consumer inflation. FLIN’s outsized financials exposure has been punished YTD (unjustifiably so, given the major Indian banks’ strong capital positions), and with valuations more palatable, I view current levels as a compelling entry point.