Fisker Stock: Inflection Point (NYSE:FSR)

Mario Tama

Shares of Fisker (NYSE:FSR) soared more than 30% on Monday after the electric vehicle start-up made the announcement that deliveries of its first-ever production car, the Fisker Ocean sport utility, are about to commence in the short term. The EV maker is also seeing continual momentum in Fisker Ocean reservations and Fisker submitted a strong production target for FY 2023. The start of deliveries marks an inflection point for the electric vehicle company and the announcement that deliveries for its flagship SUV will soon begin has cleared a lot of negative sentiment overhang. With deliveries commencing in spring, I believe Fisker is an attractive rebound stock considering that the firm’s valuation lags its rivals in the EV industry! My previous coverage on the stock was in April 2022.

Update about Fisker’s reservation status

Fisker reported approximately 65,000 reservations for its Ocean Fisker EV model as of February 24, 2023. The EV company had 56,000 reservations for its first-ever production car as of August 1, 2022, so Fisker is seeing strong pre-order and reservation growth. Since its last earnings report, Fisker added approximately three thousand reservations. This is good news because there have been concerns over headwinds for the EV sector due to slowing consumer demand. Also, Tesla (TSLA)’s recent pricing actions — which saw prices for key models come down as much as 14% in some regions — were meant to stimulate demand… which may be seen as a warning sign that growth in the EV market is slowing. However, Fisker’s CEO said he is expecting the company’s reservation book to grow to 80,000 by the end of the year, so slowing consumer demand is clearly not an issue for Fisker, at least not right now.

Fisker’s reservation growth is especially impressive considering that Lucid (LCID), as an example, reported a drop-off in reservations.

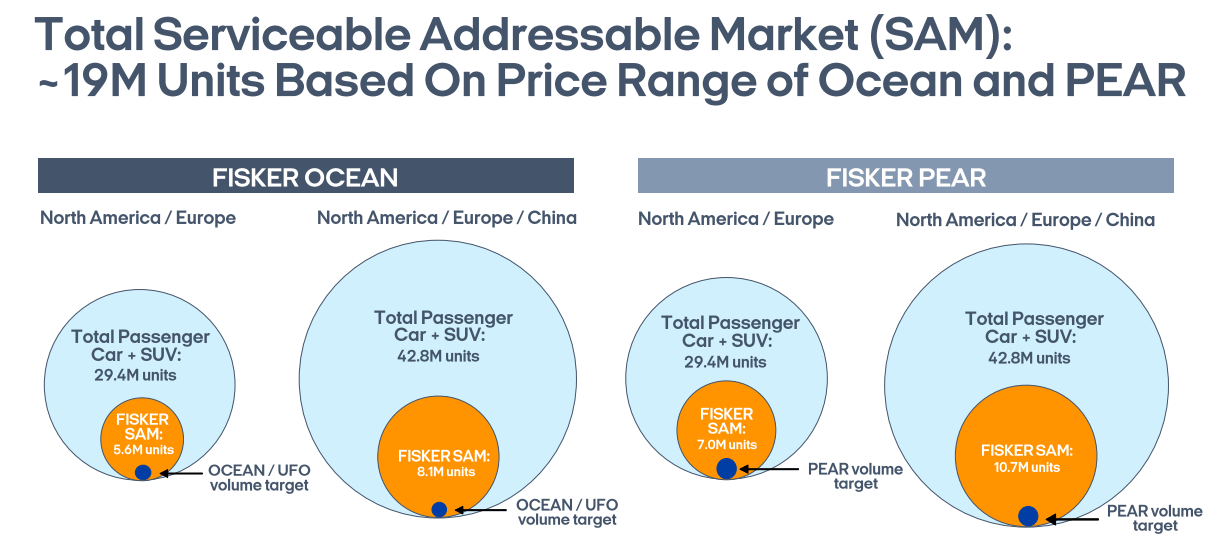

By commencing deliveries for its first-ever production car, Fisker is tapping into an expanding market for electric vehicles in the US. Fisker has said that it plans to debut four different EV products by 2025 and the Fisker Ocean SUV is only the first to make it to market in the US. For the Fisker Ocean, the EV company sees a global addressable market of 8.1M units. Including the Fisker Pear, a smaller SUV choice which is expected to see the start of production in the second half of 2024, the global addressable market for Fisker’s first two EV products encompasses 19M units.

Source: Fisker

Very strong production outlook for FY 2023

Fisker guided for a FY 2023 production volume of 42,400 electric vehicles, assuming that the supply chain is not deteriorating. The outlook is impressive considering that many other EV companies including Rivian Automotive (RIVN) and Lucid Group didn’t exactly impress with their forecasts. Both companies are about one year ahead of Lucid regarding their production ramps and both companies have run into supply chain challenges last year. Lucid produced 7,180 electric vehicles in its first full year of production and Rivian saw a production volume of 24,337 electric vehicles. I believe Fisker’s outlook was one of the strongest in the market and the stock has considerable surprise potential.

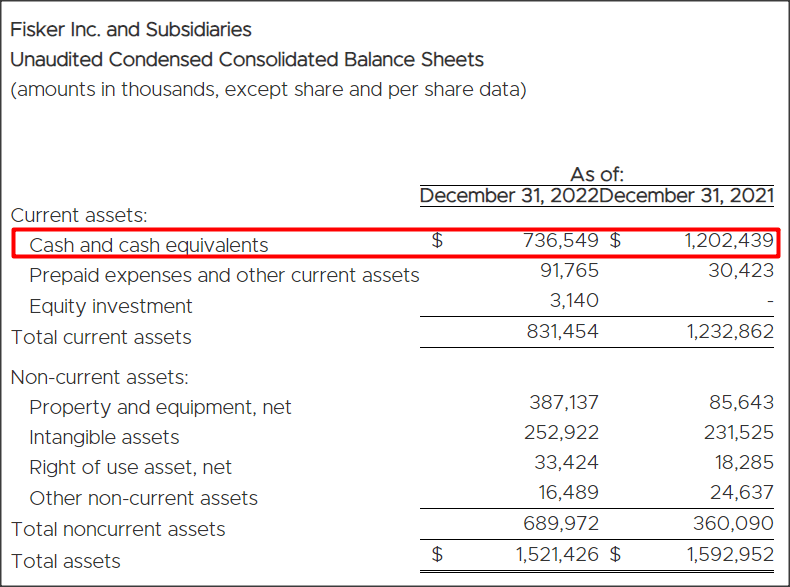

One weak point for Fisker is the balance sheet

Fisker had cash of $736.5M on its balance sheets at the end of the December-quarter which I believe is sufficient to fund operations for 16-18 months, assuming an average monthly cash burn of around $45M. Fisker doesn’t have the balance sheets of Rivian or Lucid which collected billions of dollars from rich investors to fund their production ramps. Lucid is supported and financed by Saudi Arabia’s sovereign wealth fund PIF while Rivian has been backed by Amazon and Ford. Although Fisker has not as well a capitalized balance sheet as the two other companies, I believe Fisker has enough liquidity to finance the production ramp of the Ocean and Pear SUVs.

Source: Fisker

Fisker’s valuation

Fisker is just about to ramp up production so the company has a very small revenue base. In FY 2022, the electric vehicle start-up generated just $342 thousand in revenues, but the real ramp is going to happen in FY 2023 and FY 2024. In the next two years, Fisker is projected to see its annual revenues grow from less than half a million dollars to $3.83B.

Source: Fisker

Based off of forward (2024) revenues, Fisker is currently valued at a P/S ratio of 0.61 X which makes FSR the cheapest and possibly most underrated US-based EV company in the industry. Rivian and Lucid both achieve much higher revenue-based multiplier factors with P/S ratios of 1.7 X and 4.6 X.

Risks with Fisker

Fisker obviously has production and ramp up risks that every electric vehicle start-up has to deal with. Additionally, Fisker may have higher risks than its rivals simply because the EV company does not have Lucid or Rivian-like balance sheets that resulted in billions of dollars in immediately available liquidity. What would change my mind about Fisker is if the company saw a slowdown in its reservation growth or if it burned through more cash and therefore faced a shorter liquidity runway.

Final thoughts

I believe Fisker is at an inflection point: the company is just about to commence deliveries for its first flagship Fisker Ocean SUV. Fisker is proving to investors that it has a viable product and with the beginning of the customer deliveries, I expect investor sentiment to further improve.

While Fisker still has a long road to travel regarding profitability and reaching mass production scale, Fisker really surprised to the upside with its FY 2023 production outlook. With Fisker Ocean EV reservations expected to grow to 80 thousand by the end of the year, I believe FSR is an attractive EV stock to buy for speculative investors!