Fast Fed Rate Hikes: Are They A Risk Or A Requirement?

naphtalina/iStock via Getty Images

Do adjectives matter?

A number of economists from various backgrounds can be heard arguing that the Fed is overdoing it. The financial press warns that the Fed may be causing an “Unnecessarily Deep Downturn.” Note how this language has changed. Just a few months ago the Fed was talking about the possibility of a soft landing. Now suddenly the talk is turned not just to recession… not just to the possibility of recession… but to the possibility of an “unnecessary recession and of a deep recession.” The adjectives are certainly piling up against the Fed. But what about the facts?

Does speed matter… most?

Economists who are speaking out against Fed policy are basically warning that policy has moved too fast. They’re concerned about the speed of the Fed rate hikes. Additionally, some point to the possibility that inflation may be falling in the future, that it already has fallen to some extent. That is observation and extrapolation (opinion). To me, their conclusions seem fanciful and do not address the facts: (Inflation has barely fallen and is still very high while growth seems robust).

We already have seen about two months of oil price declines and OPEC has just decided to cut back output to try to support oil prices (fact). We can hardly be sure that we have more oil price declines or even other commodity price declines ahead of us (speculation) even though there are some declines on the books and there may be some pressure coming off inflation behind the scenes (fact- see the PPI). There is some potential for trend abatement… but it’s a complicated picture.

Comparison of the speed of rate hikes with other these cycles is a natural benchmark to be expected; however, interest rate levels in this cycle were – and still are – extremely low. Rate levels relative to inflation are astonishingly low. The Fed was extremely slow to recognize inflation and then slow to act once it was recognized. At the current time, interest rates relative to inflation rates are very far behind where they would have been in any other comparable cycle at this point of tightening. If interest rates relative to inflation really matter (real interest rates), the speed of the rate hikes is justified by the low level of rates that pre-existed. This is not Machiavelli – it ‘s monetary policy.

The potential for an onset of recession is simply ‘unfortunate.’ (not unnecessary). It’s not really because of the speed of Fed rate hikes as much as of the high level of inflation that demands action involving a super low starting interest rate.

Where is inflation going?

There is for now very little evidence that inflation is really falling, apart from in the PPI and for select commodity prices. But, with oil set to reverse on OPEC-plus action the follow through for oil prices is doubtful. Instead, most of the evidence points to inflation being stubborn – that includes wage inflation. Even so, inflation has come off in some key areas and there appears to be some let up in supply congestion.

Recession is not the objective

Some have turned-coat to say that the Fed’s objective now is to create a recession. I don’t think there’s any evidence to support that. But, if we’re to look at the facts (God forbid!), there’s some weakening in the manufacturing sector, industrial production has softened, the PMI indices for manufacturing are weaker, and there’s a crash in housing. But there also has been a rotation by consumers out of goods into services. The service sector is actually looking extremely solid. This is the job-creating sector of the economy, and if it’s not going to slow down, the economy certainly isn’t either let alone plunge into recession. The Atlanta Fed’s current GDP-Now estimate for Q3 is 2.8%. That’s not very recession-like after all that hiking – is it? Fed hiking seems justified.

Real rates are too low! Period!

One aspect that Fed critics ignore is the fact that even if the Fed were to get the funds rate up to 4% – 4 ½% (higher for some) where it seems to be aiming, it would still be – based on current inflation – about four percentage points below the current inflation rate – CPI. It’s hard to look back and find any point in history when anybody would have thought that would be a good point to stop tightening monetary policy – with Fed funds 4 percentage points below the current inflation rate!

Regime shift Vs. now toxic policy options

The Fed’s mistake, as we all know, was denying that inflation was picking up and waiting too long to hike rates. In addition to that, the Fed started from an extreme deficit position with the funds rate well below the inflation rate. Then COVID happened and the global economic condition shifted.

The question is how does the Fed deal with inflation and is it appropriate for the Fed to move rates up faster to try to get to where it should have been sooner… or is the very speed of the move in the Fed funds rate more dangerous than the low level of fed funds relative to inflation were it to linger?

Real fed funds rate – an endangered species?

Frankly, I have heard very little discussion of this at all. People who are upset at the speed of the Fed’s move wave their hands about lags and monetary policy and talk about how inflation might be coming down and they talk about global conditions and opine about other causes for inflation as though any of that really matters. There’s literally no talk whatsoever about the proper level for the real Fed funds rate – Or how to measure that. And once we get into that discussion, the question will become …and which price index do we use?

The Fed may target the PCE but if the CPI is two percentage points hotter, calling Fed funds above the PCE the real rate is not very open-minded and may not be correct. The huge gap between the PCE and the CPI makes a real Fed funds rate calculation a real adventure. I don’t see how the Fed can run policy off the PCE and ignore the CPI… but it will probably try.

Defining a neutral or restrictive rate has become challenging

Setting interest rates relative to the inflation rate used to be the way we thought about monetary policy – the “gold standard.” But not anymore. Fed Governor Lael Brainard is speaking about how the Fed should pause; she talks about how the Fed policy may have to be restrictive for a long time… a curious phrase and one the Fed has had some trouble with. Several FOMC press conferences ago, Fed Chair Powell referred to the Fed funds rate as “neutral” when what he meant was “long-term neutral” and that was true only if the inflation rate was at 2% (which it is/was not).

That was a clear gaff by Powell. Now Lael Brainard is hauling out the “long-time restrictive language” when it’s not clear when or if the Fed funds rate will be restrictive! And she does this while she urges pausing (now?). I find this strange and far from clarifying.

The notion of a neutral or restrictive Fed funds rate seems elusive to Fed officials. And this confusion is yet another reason for Fed officials to not speak of a real Fed funds rate or explain what it is.

The Fed’s approach to policy is technically confusing

Fed policy has become confusing because of the things the Fed does not want to talk about. There’s a sort of suppressed embarrassment at the Fed that inflation is so high and the Funds rate so low. The idea that the Fed might “pause here” or “soon” and that “policy would remain restrictive for some time” is said and left without any explanation. Inflation by any accepted measure lies well above the current fed funds rate. Policy does not begin to be restrictive until we get the Fed fund rate above the inflation rate. There are some exceptions, of course. Mortgage rates are high and they are creating havoc in the housing market. But, by and large, Fed policy is not restrictive causing me, at least, to have little fear about the recent rapid rise in the Fed funds rate.

An unprepared market is a vulnerable market

Markets may not have been priced for the sort of added rate hiking the Fed did. As a result the market decline is being blamed on the Fed and extrapolated to imply that the Fed is causing recession. In the end it does not matter. Markets will fall, they will rebound, they will assess prospects, they will trade. Economist Paul Samuelson cracked that the stock market had predicted nine out of the last five recessions. I don’t see any reason to enshrine market behavior or to use it to lampoon the Fed.

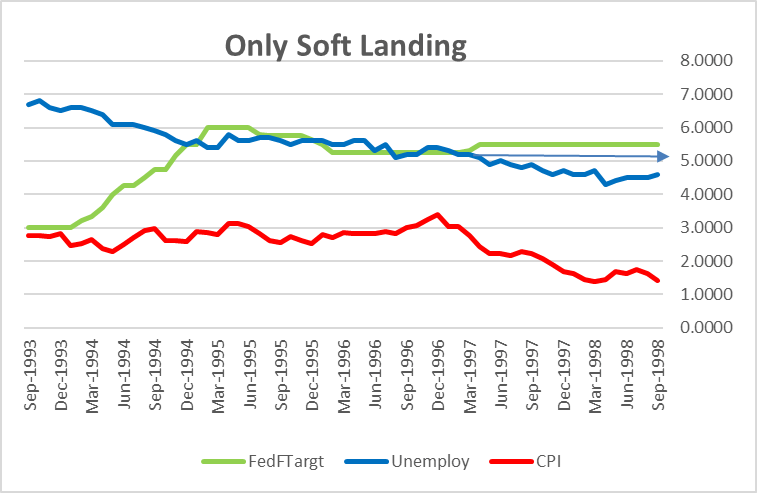

There has been only one soft landing – it was in an inflation-tranquil period.

Only Soft Landing (Haver Analytics)

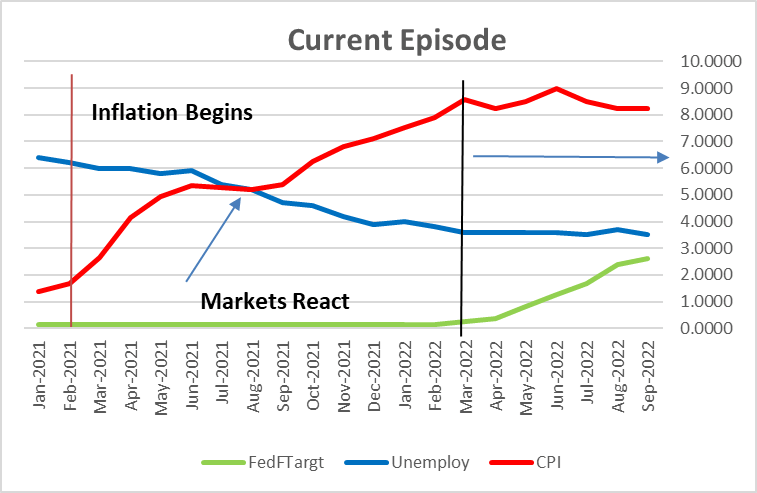

You can’t stuff this square peg into the round hole of “soft landing.”

Current Situation High Inflation; Low Fed F (Haver Analytics)

Pretending was never a good strategy

More to the point, the Fed tightening is not causing a recession. Markets are reacting to high inflation and the need to lower it. What no one admits is that, historically, inflation has never been this high and then controlled – without running a recession. Numerous voices have “weighed in” on soft landings arguing against the weight of history that Fed had achieved a number of them in the past. All that talk was a bunch of red herring hooey. The Fed never achieved an acknowledged soft landing with inflation anything like this. If the Fed were able to quell this inflation without running recession – that would be a miracle. That’s very different from saying the Fed is overdoing it and causing recession – don’t you think?

Fed policy hopes it sees the home stretch

Fed policy is still not in a good place. It’s in a better place than it was. More important, the Fed has “found its voice.” Clearly getting inflation back to 2% and doing it quickly – not letting it languish – is the best policy.

In this view, markets are more at risk because the Fed is focused and not compromised. The Fed needs to pay attention to both the CPI and the PCE. It needs to make sure it does not just take the top off inflation but that it “follows through” to control inflation back to target – as it failed to do in the late 1960s. It’s a complicated assignment that is likely to carry with it more fallout. There’s a lesson here we all should learn about urging the Fed to run a bit more inflation for this reason or that, for this group or that. It’s just not a good idea.

During deflation, the Fed bemoaned how bad that was and how different inflation was (compared to deflation) because they “knew what to do” to cure inflation. In hindsight, the Fed may know how to stop and push back inflation but doing it has not proved easy. However easy or hard it is, it’s the Fed’s job and it’s good to see the Fed is finally focused on achieving its mandate.

This means…

The Fed has more work to do and will raise rates more. Since we can’t be sure if the right actionable inflation rate is the PCE or the CPI the Fed probably will focus on the PCE and try to raise rates above that (the lower threshold) as a first approximation and bill it as a positive real interest rate that is restrictive. For that the Fed is shooting at its own expectations for PCE inflation in 2023 from the SEPs, a rate it projects at 3% by year end 2023, down from 5.5% at end 2022.

The average of those two puts PCE at 4.25% around mid 2023 and explains the Fed’s “current focus” on a 4.5% to 4.75% level for Fed funds (the market’s focus is moving higher) This “clarifies” that the Fed is ignoring the 8.2% CPI inflation (right or wrong). If that does not work, the Fed will squeeze harder and put Fed funds above the CPI pace (which should be lower than 8% in 2023). On balance, in store are higher short term rates and higher long-term yields (to a lesser extent, a flatter yield curve; likely fully inverted).

Stocks will continue to flounder. The politics will play out especially over the next month ahead of the midterm elections as some will try to demonize the Fed for trying to cause a recession to deflect political blame. But all the Fed is trying to do is to contain and reduce inflation. Beware (as in be aware) of the political affiliation of the economist or strategist you listen to. Political opinion is a bad investment advisor.

There’s more bad news ahead; the recent IMF outlook has underscored that. Short-term rates will rise and stocks will remain in trouble. There’s a significant risk that inflation will not fall as much as the Fed wants/expects especially with the revelation that OPEC+ will not go away quietly and instead seems intent on propping up oil prices as long as it can (that means until recession strikes). That creates an added risk for even higher rates next year. However, in two or three more months, the historic inflation patterns will begin to favor some drop-off in inflation pressure – but not in time for the elections. For the next two months, no asset class seems safe. Cash will remain king or will seem like a get-out-of-jail-free card because it will keep your options open and your mind clear.