EQT Corporation Stock: Here Come The Results (NYSE:EQT)

imaginima

EQT Corporation (NYSE:EQT) is a management that “hit the ground running,” because the new management at the time believed this company needed a lot of work to avoid a big crash in the future. Little did any of us know that the pandemic was on the way. Had this management not stepped in when they did, there could have been some real carnage with this stock.

But avoiding carnage is something that is not readily apparent to a lot of shareholders. So sometimes management does not get the credit it deserves for turning a situation around before that brick wall is in your face. But what often gets credit later is the common share outperformance from the superior management.

Quick History

The current EQT management took over from a “good enough” management. I have often warned that this is a very dangerous industry for “good enough” management because oftentimes that “good enough” management turns out to be insufficient when something unexpected happens.

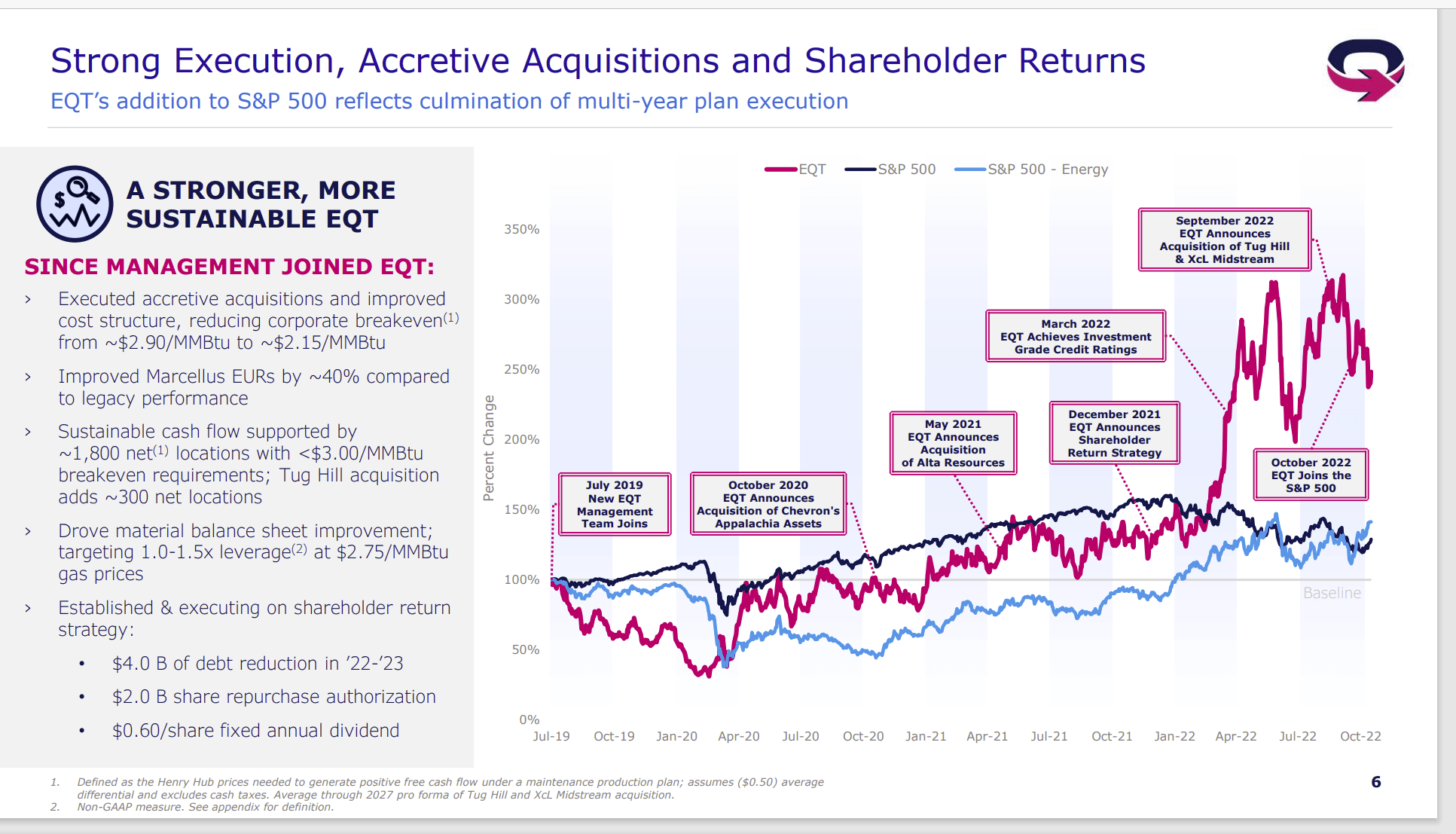

EQT Corporation Management Review Of Accomplishments Since Taking Over (EQT Corporation Third Quarter 2022, Earnings Conference Call Slides)

As is often the case with good management, the above really is only part of what was accomplished. EQT Corporation faced an impressive debt due schedule that management had to refinance as the pandemic was arising. As a whole, lot of commenters were stating that the industry had no money available, but this management refinanced the debt due schedule into something far more palatable.

Management then carefully acquired properties in such a way with a combination of cash and stock that financial strength increased right through the pandemic until the company reached the investment grade status shown above. Notice the acquisitions made at a time when supposedly money was not available to the industry. This company was busy proving that wrong.

In the meantime, EQT Corporation management dropped the corporate breakeven while picking up properties that also produced liquids. Liquids production generally has higher costs along with a more valuable income stream to produce a wider margin. Yet this management reduced costs even with that higher cost acquisition.

It should be noted that management acquired more dry gas production as well. But what is different now is that liquids are slowly changing the average price a little bit (as that production increases in significance), whereas before liquids production was insufficient to change the average price received from the natural gas price.

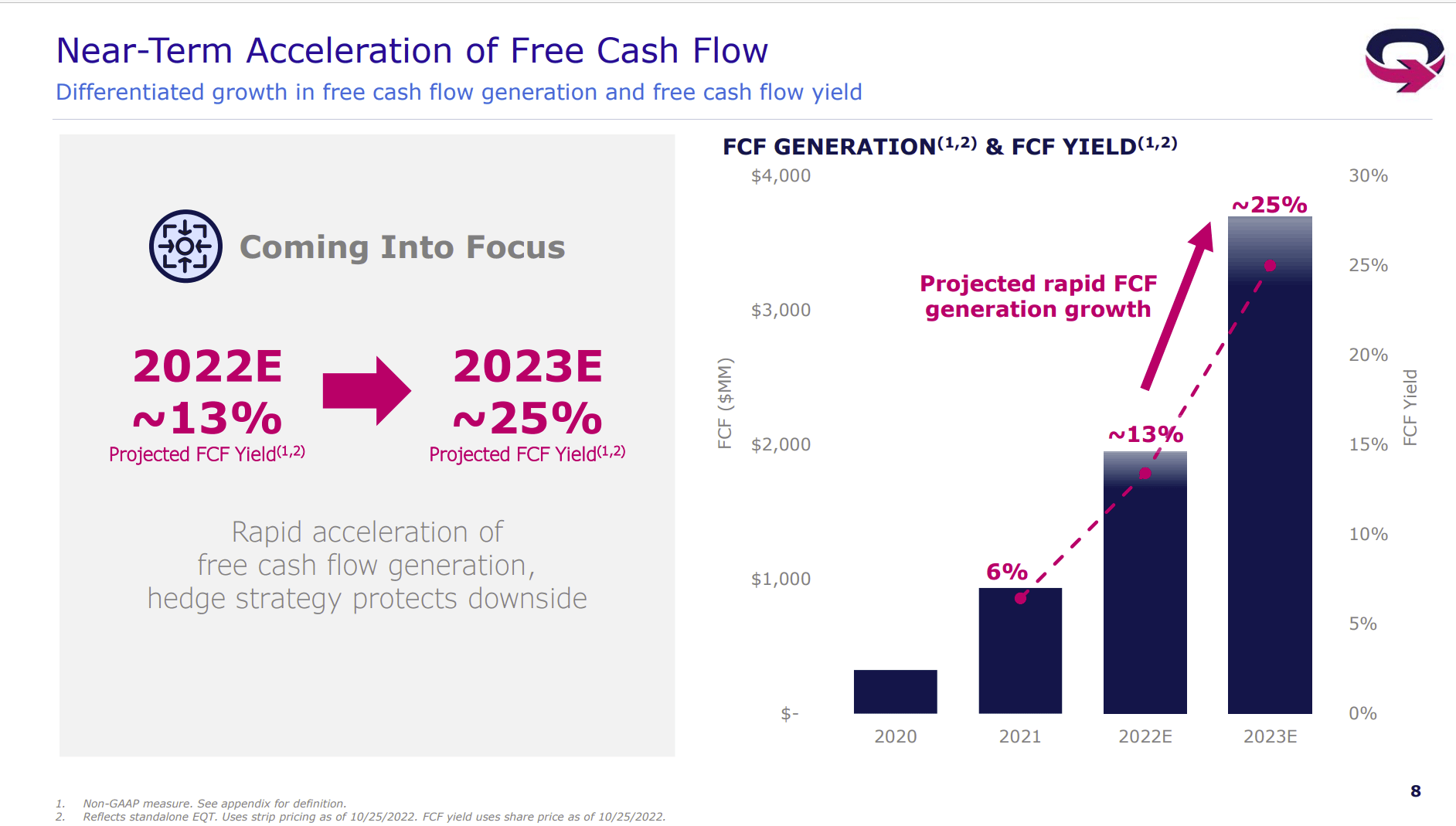

Free Cash Flow Generation

Management now has the company in a position to generate quite a bit of free cash flow (“FCF”).

EQT Free Cash Flow Guidance For 2023 (EQT Third Quarter 2022, Earnings Conference Call Slides)

This growth comes as a result of two decisions.

The first decision was the one made to hedge the production to guarantee a cash flow back when the financial structure was far less than what it is now. While that is a very typical industry practice, far stronger than anticipated commodity prices led to a lot of “mark-to-market” losses that really did not impact the cash flow. What those hedges really represented instead was a forward sale of natural gas prices at what turned out to be below market pricing.

The second decision that EQT Corporation management noted with the latest acquisition was a decision by management to diversify the markets in which the natural gas is sold. The good enough previous management basically sold the production to basin customers. Then when the basin became oversupplied, the price of course dropped relative to benchmarks.

Fixing that issue will take a while as midstream transportation contracts are long-term. But management has already found some transportation to export locations where the prices are much better than the basin. Management has also picked up some midstream capacity with the latest acquisition to places with stronger commodity prices.

Sometimes investors do not find out what a mediocre management does for years because the information is just not available. In this case, the company is still paying for some less-than-optimal decisions by a “good enough” management. Nonetheless, the periodic expiration of transportation agreements combined with the commitment of management to back new projects should provide a steady stream of cash flow improvements in the future (even if those improvements are “lumpy” because contracts expire on an irregular basis).

Moving Forward

The stock price is now clearly headed in the right direction. I am constantly asked about a price target. My own idea about that is this management sold their company before when they saw a good enough price. So, I am very likely to stay invested as long as they are managing the company unless the stock price becomes so incredibly overpriced that it would be hard to go wrong to sell.

The first chart shows that market overperformance began early in the tenure of this management. That market overperformance is likely to continue long-term. So, I am not likely to try to time that market overperformance as you never know when management will overperform in the short-term.

Good management tends to surprise to the upside. I happen to want to be there for those surprises.

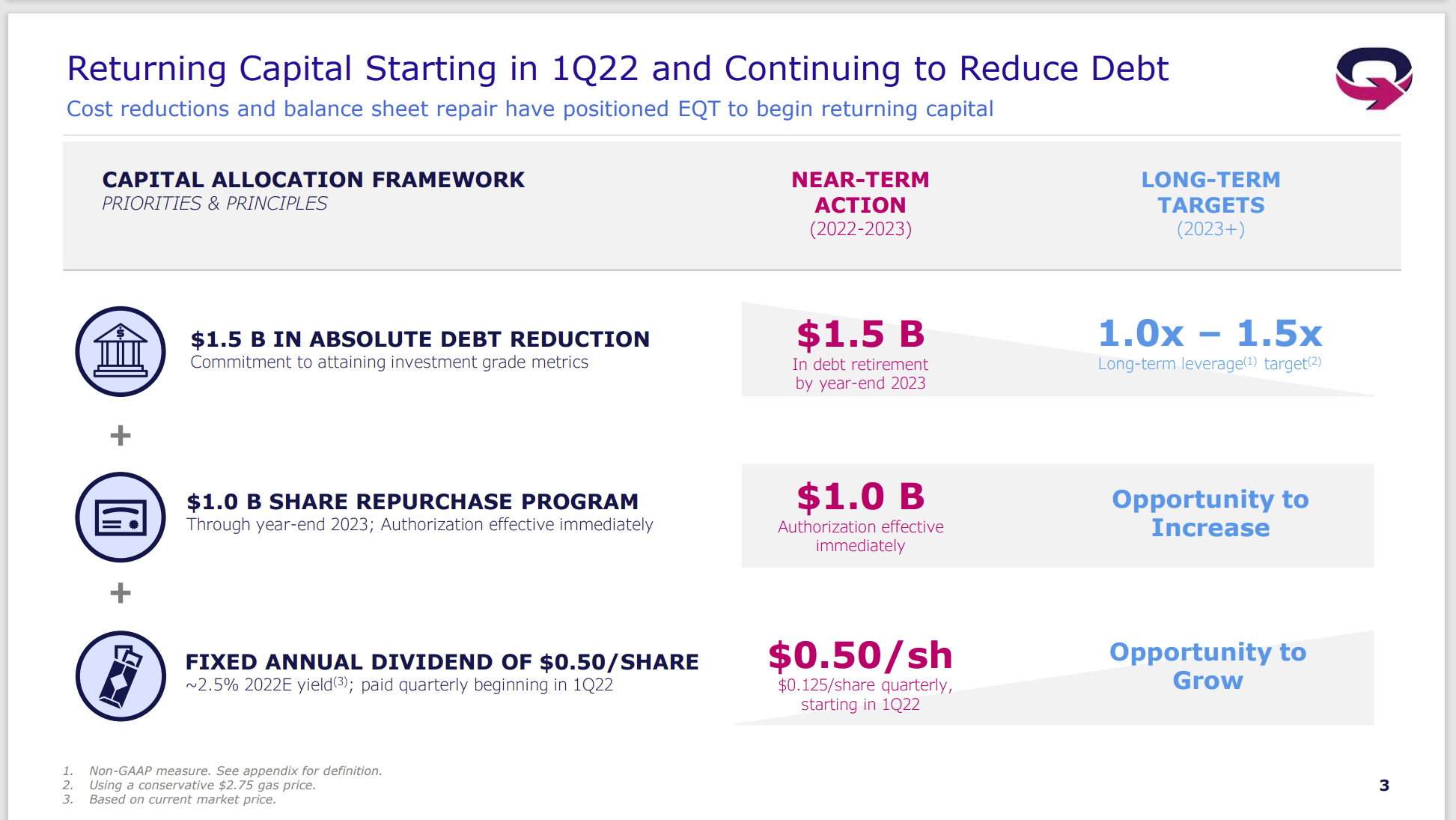

EQT Shareholder Return Guidance (EQT December 2021, Shareholder Presentation)

As an investor, evaluating the original goal is something that is worth doing from time to time. Management has actually raised the repurchase program since then when another acquisition was made. But the key to looking back at this is that management actions have improved upon the original guidance in a very tangible way. For example, that dividend has increased above the original guidance. So this management is really not sitting on past accomplishments.

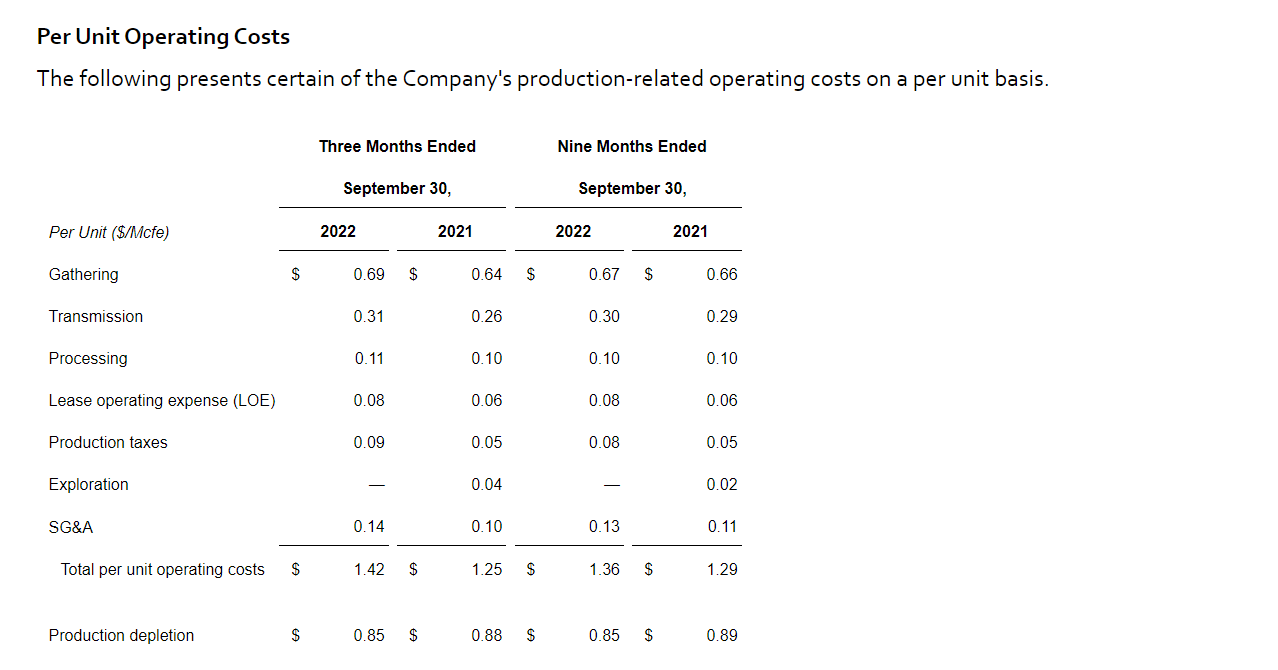

EQT Third Quarter 2022, Per MCF Operating Costs (EQT Third Quarter 2022, Earnings Press Release)

There were some unexpected lower volumes impacting the results. However, the big part of Gathering cost increases was due to calculations based upon the price of natural gas. Meanwhile administrative costs edged up due to performance awards based upon the stock price.

Transmission is another largely contracted price that can move somewhat was the commodity sales prices. Basically, though the prices that management can control were very well controlled. The depletion is a very controllable costs that represents the capitalized well costs.

The lower operating costs mean that the company is better able to cash flow during the industry downcycle. The lower depreciation means that the company is more profitable at various commodity pricing points.

Currently, the effect of liquids is pretty small. But the acreage is available for management to increase that effect should industry conditions so dictate. That likewise gives EQT Corporation flexibility for profitability under a wider variety of industry conditions.

Summary

This EQT Corporation management has done a lot to improve the company performance since it took over. There is likely to be a lot more good news in the future, because managements like this one tend to not sit on accomplishments, but instead tend to set new goals.

The kind of detail that management has shown since taking over EQT Corporation is the kind of detail needed in this industry. The average profit margin in the total business cycle is not that great. So, attention to low costs as well as the latest technology improvements is essential. This management is very likely to keep ahead of the competition in the future. So rising dividends and more stock repurchases are likely in the future along with some unexpected, good news from time to time.