Emergent BioSolutions (EBS): Positive NARCAN FDA Panel, Divesting Travel Health

Spencer Platt/Getty Images News

Singular Research

Investment Thesis

Emergent BioSolutions (NYSE:EBS) announced that the FDA’s Nonprescription Drugs Advisory Committee has unanimously voted in favor of approving NARCAN nasal spray for over-the-counter use. While the FDA is not bound by the committee’s guidance, we believe, based on the type of product and urgent utility of this product in the over-the-counter channel, FDA approval is imminent. The PDUFA date for the product is March 29, 2023, when the FDA will announce its final decision on NARCAN nasal over-the-counter use. Though we believe the approval is imminent, the label with which the FDA approves and if the agency requires post-marketing studies remains uncertain.

NARCAN nasal spray is a nasal naloxone product for the emergency treatment of opioid overdose. This product is available as a prescription medicine, but an over-the-counter approval will dramatically broaden access to and use of the NARCAN nasal spray for those who may be at risk of an opioid overdose.

If approved, EBS’s NARCAN will be the first over-the-counter opioid overdose product. According to the CDC, the number of drug overdose deaths have accelerated recently. The deaths are currently growing at 30%/year and have quintupled since 1999. Nearly 75% of the 91,799 drug overdose deaths in 2020 involved an opioid.

Growing at an even higher rate, 38%/ year, opioid-involved death has attained an epidemic status, as shown in Exhibit 1. Even more alarming are synthetic opioid overdose deaths, which are growing even faster at 56%/year.

Strategic Restructuring and Travel Health Divestment

The Company recently announced that it has entered into an agreement to sell its Travel Health business to Bavarian Nordic for $270 million. The deal could earn EBS an additional $110 million in future milestone payments, bringing the total value of the deal up to $380 million.

While financial details of the deal, beyond the purchase price, were not disclosed by the Company, we expect it to be accretive to EBS. Therefore, though we would not be able to comment on the valuation of the deal, we can provide a few estimates on how this deal might affect the Company’s financials. First, we believe that this deal will help EBS’s operating margins, as we believe Travel Health consumes a significant amount of Selling & Marketing expense. Second, with 280 current EBS employees switching to Bavarian Nordic as part of the deal, about $56 million/year will be shaved off the Company’s SG&A expenses. Third, if the Company chooses to reduce its debt by the $270 million in cash its balance sheet will be receiving, EBS will reduce its interest expense by $6.1 million/year. In conclusion, though the revenues and operating income part of the Travel Health segment are undisclosed, we believe that an estimated savings of over $60 million/year in operating and financial costs will make this deal accretive.

Risk

EBS’s business model is focused on public health biodefense threats, a niche industry where revenue streams are exposed to the uncertainty associated with government contracts.

Valuation

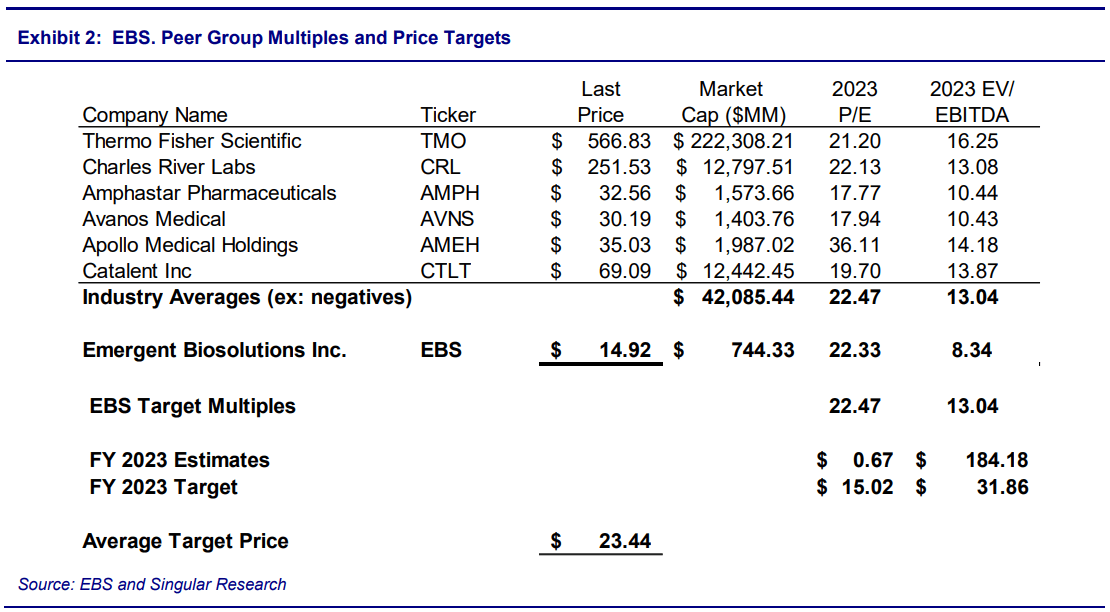

As a specialist in public health and medical countermeasures, EBS has few direct competitors. The table below compares EBS’s valuation to that of two competitors, Thermo Fisher Scientific (TMO) and Charles River Labs (CRL), and four pharmaceutical companies of comparable market values, Amphastar (AMPH), Avanos Medical (AVNS), Catalent (CTLT), and Apollo Medical (AMEH). As shown below, though the Company trades in line with peers based in terms of forward P/E, and it trades at a deep discount on the forward EV/EBITDA metric.

We derive our $36 price target for EBS stock by using a 50/50 blend of the price targets obtained from our DCF model and a multiple-based (P/E and EV/EBITDA) valuation. We value EBS at 22.5x FY:23 EPS and 13.0x FY:23 adjusted EBITDA. Our EV/EBITDA and P/E multiples are in line with the peer group average multiples. Our P/E and EV/EBITDA-based analysis generates a $23.44 price target, as shown in Exhibit 2.

Our DCF model uses our forecasted free cash flow to the firm over the first two years and then grows EBIT at a 50% rate for year 3, 30% for year 4, 20% for year 5, and at 6% thereafter. We apply a weighted average cost of capital of 6.52%. Our DCF produces a value of $48.14.

By equally weighting and blending the price targets obtained from our P/E and EV/EBITDA analysis and DCF model, we derive our $36 price target for EBS shares.