Elme Communities: Delivering Results But Richly Valued (NYSE:ELME)

MarekUsz/iStock Editorial via Getty Images

Elme Communities (NYSE:ELME) is a multifamily-focused real estate investment trust (“REIT”) that owns and operates nearly 9K homes in the DC Metro and the Sunbelt region of the U.S. In addition, they own approximately 300K square feet (“SF”) of commercial space.

The company’s communities are principally value-oriented and are in both urban and suburban environments. On average, renters save about $500/month by living at an Elme community instead of at a new Class-A community within the same neighborhood.

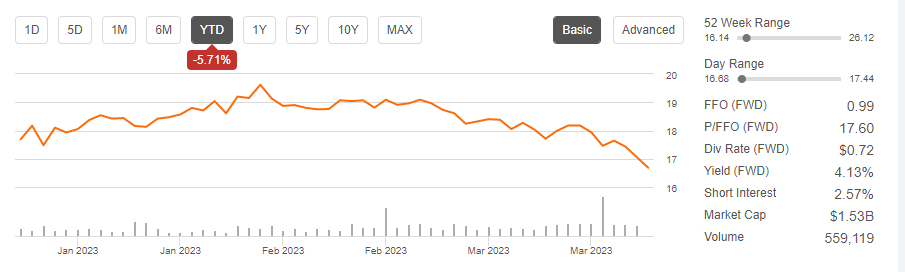

YTD, shares are down about 6%. And they are down about 8% since a prior update on the stock.

Seeking Alpha – Basic Trading Data Of ELME

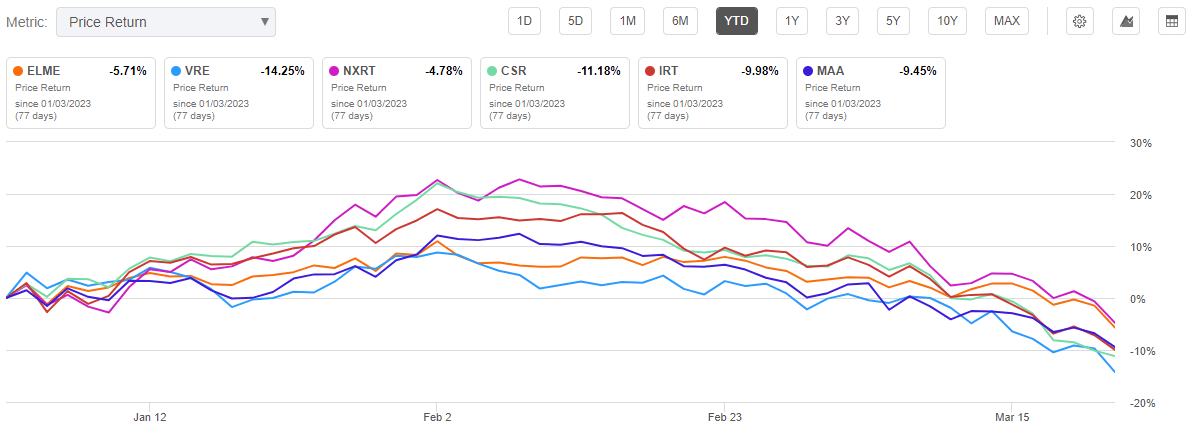

While shares are underperforming broader markets, they have remained more stable than related peers within the sector.

Seeking Alpha – YTD Returns Of ELME Compared To Peers

In 2022, ELME turned in solid operating results, especially towards the back half of the year. They are also off to a good start to the new year. Strong operating results also enabled one of their first dividend hikes in recent periods. Despite the positive fundamentals, I view the upside potential as limited due to their current valuation, which is presently well above related peers in the sector.

Recent Performance and Current Portfolio Metrics

In Q4, ELME’s same-store (“SS”) average occupancy came in at 95%. While this is in-line with their targeted range, it is down 90 basis points (“bps”) from last year. Retention, however, improved 2% from the prior quarter to 62%.

Quarterly SS net operating income (“NOI”) grew 11.6% YOY. Prime contributors include effective blended lease growth of 5.7%, with renewal spreads up 10.1%. In addition, effective monthly rents were up 9.7%.

For the full year, overall average occupancy was up 30bps from the prior year to 95.6%. In addition, SS retention improved 3% to 63%. Together, this contributed to SS NOI growth of 8.8% and a blended lease growth rate of 9.4%. The lease growth is notable, considering they realized just 1.3% growth in the prior year.

Overall, ELME reported core funds from operations (“FFO”) of $0.88/share in 2022. While this was down on a YOY basis, it was in-line with the midpoint of their guidance range. Additionally, core FFO was up over 40% for the quarter due to favorable rental rate growth and full deployment of their commercial portfolio sale proceeds.

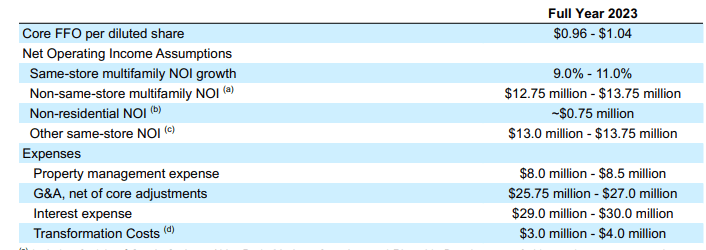

For 2023, management is expecting core FFO to settle at a midpoint of $1.00/share, implying double-digit growth over 2022 levels. This would be on SS NOI growth of 10%, which would be 120bps improved from 2022.

Q4FY22 Investor Supplement – Summary Of 2023 Guidance

Subsequent to year end, ELME reported effective rate growth of 4.5%, with renewals up 8.8%. This is a step down from the growth rates logged in the final quarter of the year.

But through the date of their release, management noted favorable blended growth of 5.8%, with renewals up 9.1%. In addition, they are currently signing new leases at effective spreads that are over 4% on average. This would be a significant improvement over prior growth rates.

While rate growth is expected to moderate from the current high single-digit levels, the rate environment is likely to be favorable at least through the first half of the year, as it was noted that renewals offers for April lease expirations are currently quoting increases of 7% on average.

Liquidity and Debt Profile

ELME generated +$73.2M in operating cash flows in 2022. And they had about +$36.5M in capital outlays, leaving approximately +$36M for dividends and other priorities. Supplementing their reoccurring positive cash flows is full availability on their revolving credit facility, which totaled +$650M at the end of 2022.

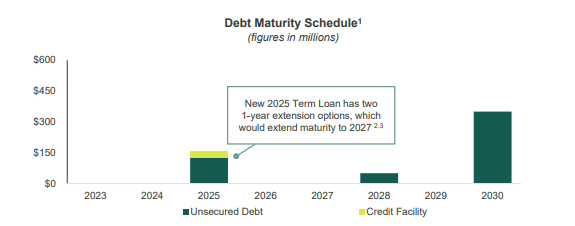

While they already had a favorable debt stack, they made it even more so subsequent to year end. In January, they secured a new 2-year term loan and used the proceeds to pay down prior balances. As such, they have no scheduled maturities until 2025 at the earliest.

March 2023 Investor Presentation – Debt Maturity Schedule

The new loan is, however, variable rate, which exposes them to greater interest rate risk. But their forward guidance accounts for this. At current projections, management sees 2023 interest expense landing around +$30M. This would be an increase of about 18% from 2022 levels. Yet, even with the additional interest burden, core FFO is still expected to be up double-digits.

In addition, ELME currently has capacity within their current covenants and coverage ratios to absorb the additional interest expense. And at current leverage levels of 4.8x, they are presently running below their targeted range, providing them with sufficient breathing room to handle a higher load, if necessary.

Dividend Safety

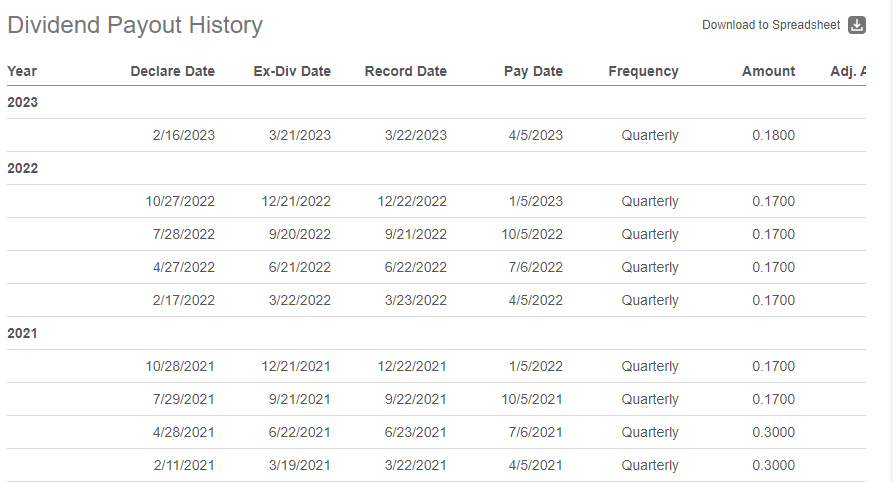

ELME recently increased their quarterly dividend by nearly 6% to its current payout of $0.18/share. At current pricing, this represents a yield of just over 4%.

The increase was a first in recent periods, after having settled at $0.17/share through the entirety of 2022 and through the middle half of 2021.

Seeking Alpha – Recent Dividend Payout History

At the midpoint of 2023’s core FFO guidance, the current payout represents a ratio of 72%. This is generally on par with sector averages. Recent management commentary also indicated that the payout would remain at or below their mid-70s target for 2023.

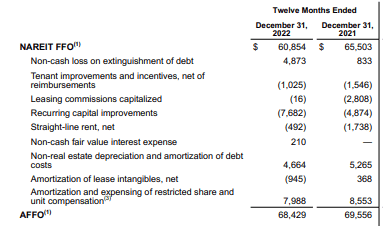

One should, however, consider their recurring capital commitments for their renovations. In 2022, they spent +$7.7M on these improvements. Taking that into account would translate to a payout ratio closer to 90% based on an $0.18/share quarterly payment and AFFO/share of $0.78/share.

Q4FY22 Investor Supplement – Snapshot Of Comparative AFFO

Final Thoughts

ELME finished on a strong note in 2022. Despite pushing rents higher, occupancy was down just 90bps in Q4. And offsetting this was improved retention rates, which grew on a sequential basis and ended the year up 3% YOY.

2023 also appears to be off to a good start, with rate growth on track for sequential improvement over the winter lull in Q4. While growth rates are expected to moderate through the back half of the year, the company is still expecting double-digit growth in core FFO.

The fundamentals of their markets provide confidence that ELME could hit their targets for the year. For one, new resident incomes in the Washington and Atlanta metros were up approximately 8% and 14% YOY in Q4FY22. This compares favorably to the national average. In addition, employment, wage, and population growth in ELME’s markets are all expected to continue outpacing national averages through 2027.

While the threat of rising supply may be on the mind of some, most of the nearby supply coming online are located outside of ELME’s submarkets. In the Washington metro, for example, 84% of development is occurring within the Capital Beltway. ELME’s core presence, on the other hand, is in more suburban districts.

ELME’s communities are also more affordable than alternatives due to the Class-B nature of the properties. On average, their residents are saving nearly $6K a year by living in their communities as opposed to a nearby Class-A community. A sizeable renovation pipeline on approximately 3K homes also provides an attractive value-add opportunity for future earnings growth.

Despite ELME’s positive fundamentals, shares provide little value to investors seeking upside potential. At over 17x forward FFO, the stock trades at a premium to most of its multifamily peers. Independence Realty Trust (IRT), for example, currently commands just 13.4x. Granted, IRT’s debt load is considerably higher. But this is offset by their stronger renovation pipeline.

NexPoint Residential (NXRT) is another similar-sized peer that also trades in the 13x range. In my view, ELME needs to significantly outperform their peers to warrant new or further initiation. Though recent results have been strong, I maintain a “hold” view on ELME stock.