Denison Mines: Current Weakness Presents Buying Opportunity (TSX:DML:CA)

HT Ganzo

After an optimistic beginning of the year, financial markets are currently experiencing elevated volatility. While financials are hit the most, due to the adverse effects on rapidly raising interest rates on their balance sheets, most commodities were not spared as well. However, uranium is one of the exceptions.

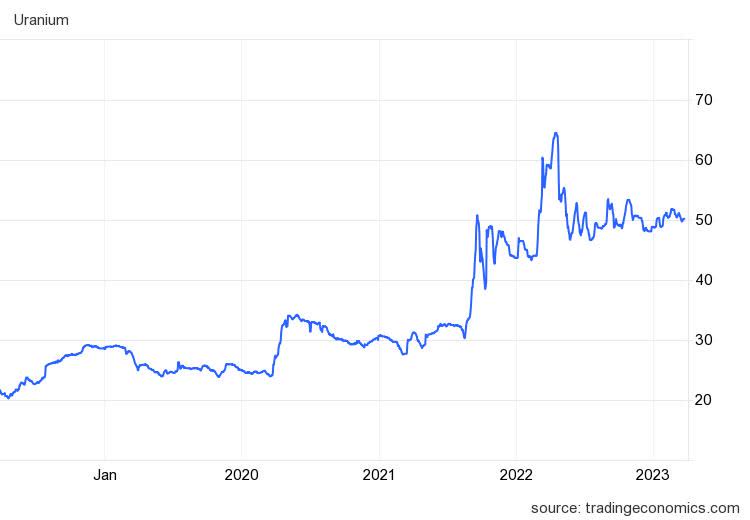

Uranium price (tradingeconomics.com)

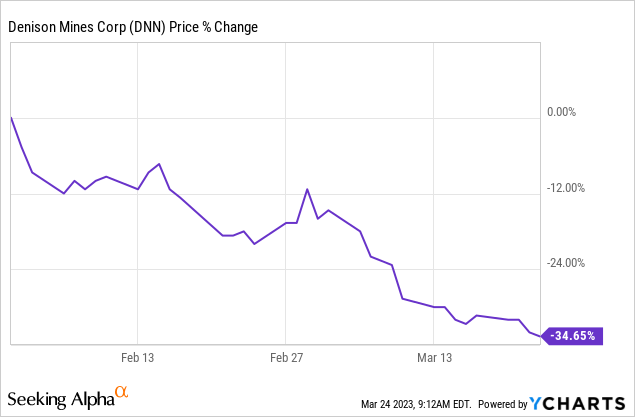

Its price has been fluctuating in a tight range around the US$50/lbs mark as its demand is generally considered insensitive to the economic cycle. On the other hand, uranium equities have suffered. While this will be understandable for companies, which are in need of capital and have to tap financial markets in the current adverse environment, others are in solid financial position with no near-term additional capital needs. One of the companies from the latter group is Denison Mines (NYSE:DNN). Its share price has tumbled more than 33% from its 2023 high, yet on the balance sheet there’s no interest-bearing debt and working capital and investments are north of CAD$200M – more than enough to meet the 2023 capital needs.

At the same time, the company is advancing its flagship Wheeler River project with Feasibility study on track to be completed in H1’23. In terms of valuation, the current decline in share price likely puts the EV of Denison around the estimated NPV of Wheeler River, without taking into account the other properties.

Progress at Wheeler River

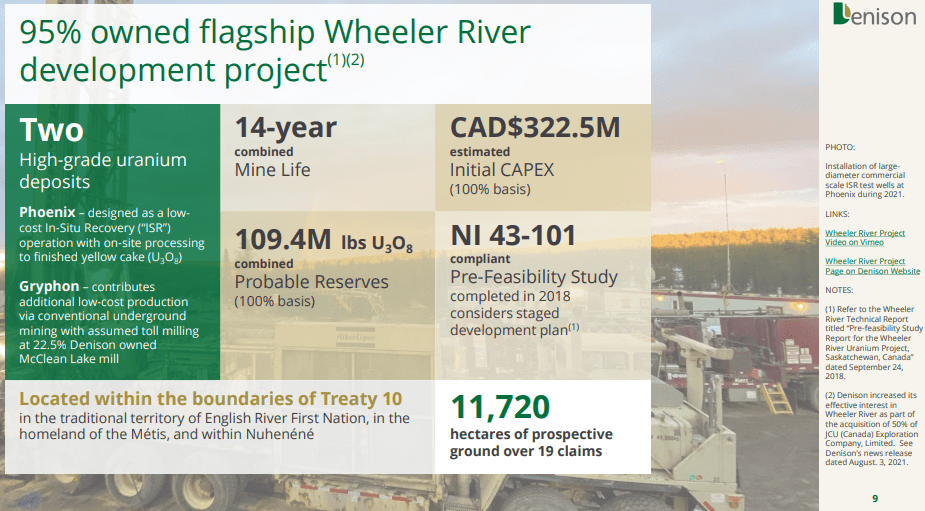

Wheeler River project (Denison mines)

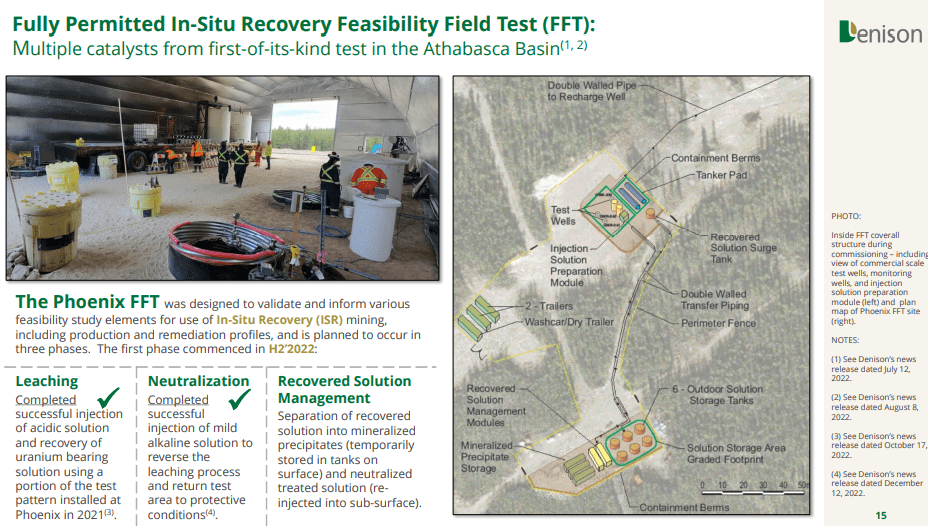

The company has achieved serious progress in 2022 towards the advancement of the Phoenix deposit, part of the Wheeler River project, located in the prolific Athabasca basin. As Denison intends to use the lower cost ISR mining method, it has to demonstrate to regulators the viability of such operations in the field. Regarding that, the feasibility field test has already made it through its first two phases – leeching and neutralization and the third part – managing the recovered solution is in progress.

Feasibility field test progress (Denison mines)

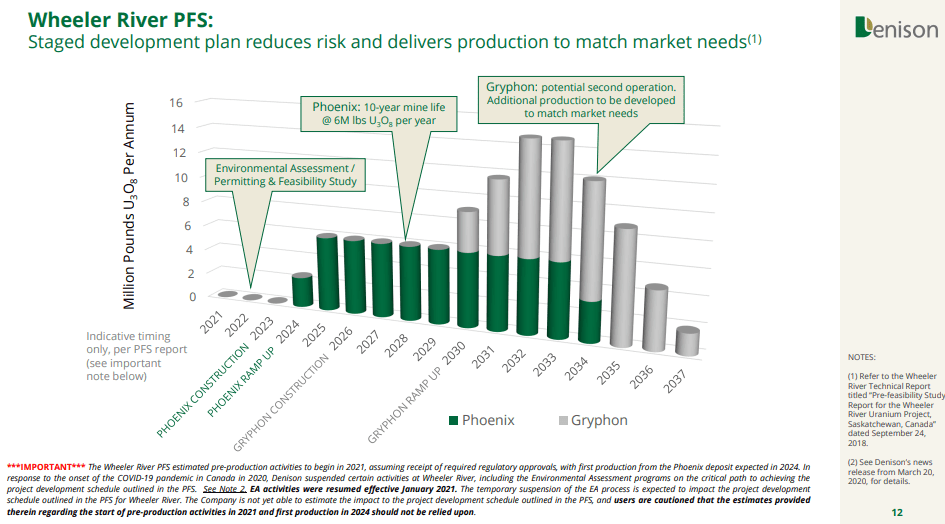

The field test will be at the core of the FS, which according to a recent interview with Denison’s CEO, is expected to be completed in H1’23. That being said, Denison still keeps in its corporate presentation illustrative timeline for the staggered development of Wheeler River, which indicates first production from Phoenix in 2024. I think that’s not very likely, given that permitting will likely push the timeline further.

Illustrative timeline of the Wheeler River project (Denison mines)

Balance sheet strength

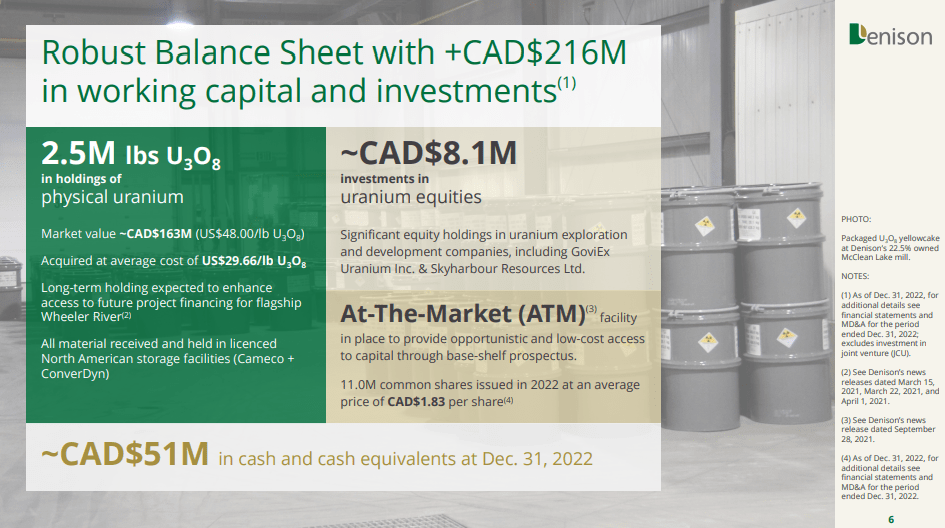

As interest rates are rising, capital becomes more expensive. For that reason, the financial condition of a company, especially in exploration/development stage, is very important as dilution risk should be considered. In the case of Denison, the company appears to be very well capitalized with over CAD$51M of cash and equivalents and 2.5Mlbs of physical uranium on its books. Total working capital is estimated at CAD$216M as of 2022 year-end, while there’s no interest bearing debt.

Liquidity position (Denison Mines)

This is more than enough to cover the CAD43.7M of projected budget for 2023, a large part of which will be spent on the completion of the Wheeler River FS. It has to be notes that the company has active ATM offering facility available at management’s discretion, but I don’t expect it to be used in the current market environment.

Additionally, there are 39.2M warrants expiring in March’23 with exercise price of US$2.25/share. Given the significant premium of the exercise price to the market price, I don’t expect any of them to be exercised, therefore no liquidity should be expected to come from them.

Valuation discussion

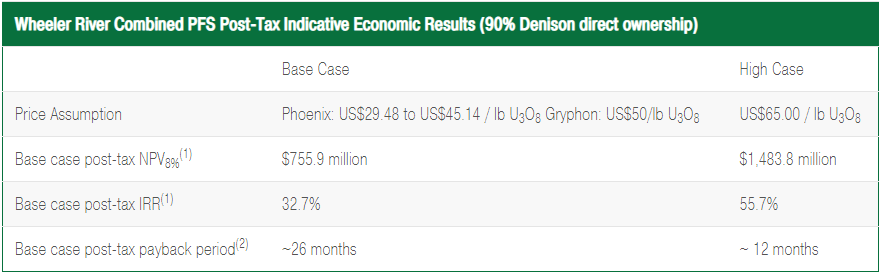

The current EV of Denison, taking into account the cash and uranium position is around CAD$900M This is a still bit higher than the after-tax estimated NPV under the base case used in the 2018 PEA of CAD$797.9M (Denison now owns 95% of the project). However, the calculations used uranium prices for Phoenix in the range of US$29.5/lbs and US$45.1/lbs. In the “high” case of US$65/lbs of uranium, the project has estimated NPV of CAD$1,566.2M (at 95% interest).

Wheeler River’s economic profile (Denison Mines)

In addition to Wheeler River, Denison has equity stakes in other, smaller projects, which could add additional value to the company by for example being sold to finance the construction at Wheeler River. So I consider the current weakness in the share price as an opportunity to potentially start a position.

Risks

Dilution risk

As a company without a producing asset, Denison can’t rely on internally generated funds to finance its Wheeler River project. At the same time, while the currently available liquidity of CAD216M seems more than enough to carry the company up to the construction of the project, it falls short of the estimated initial capital required to put the Phoenix deposit into production. According to the 2018 PEA, CAD322.5M (100% basis) is required of which Denison has to come up with CAD306.4M. Obviously, this figure is likely to go up, given the considerable inflation in the meantime. So naturally, dilution is a risk. However, I think there may be non-dilutive ways to get the project going. For example, the company may enter into off-take agreements with utilities for the uranium to be produced and then to borrow against those contracts. Another way could be to sell one or more of its other assets. Still, these sources of funding may be accompanied by a relatively small capital raise.

Geological risk

The flagship Wheeler River project is yet to go through a feasibility study, therefore there’s risk that its economics may not be attractive. With the FS expected soon, this risk may be reduced in the coming months.

Permitting risk

Denison is aiming to be the first company to bring the notorious ISR mining method to the Athabasca basin. This will likely cause regulators to be extra cautious with permitting, which may prolong the process and push out production further in time.

Conclusion

Denison mines has been hit by the current off-risk sentiment in the market. However, I don’t see fundamental reasons behind the fall – the company is well capitalized and will likely not need to seek financing up to the beginning of construction at the Wheeler River project. At the same time, uranium prices have demonstrated resilience and remained around the US$50/lbs level, despite the drop in most commodities since the beginning of the year. I see the current weakness in Denison’s share price as an opportunity to eventually initiate a position.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.