CrowdStrike: Premium Price, But Has The Growth To Back It Up (NASDAQ:CRWD)

Just_Super

Investment Thesis

I give CrowdStrike (NASDAQ:CRWD) a buy rating primarily due to its great retention metrics, doubling software’s longstanding “Rule of 40,” and the fact that it’s currently trading at a significant discount compared to its all-time high.

Company Overview

CrowdStrike, founded in 2011, is a cybersecurity company that focuses on providing cloud-based endpoint protection, threat intelligence, and incident response services.

At the core of CrowdStrike’s offerings is the Falcon platform, their flagship product. This cloud-native platform ensures protection across all endpoints, including laptops, desktops, servers, and mobile devices. Using AI and behavioral analysis, CrowdStrike’s platform can detect and prevent even the most sophisticated cyber-attacks. Unlike traditional antivirus solutions, Falcon goes beyond known threats and offers comprehensive protection against both known and unknown threats.

CrowdStrike caters to a diverse range of customers, including large enterprises, government agencies, and small to medium-sized businesses. Their services extend beyond mere protection, encompassing threat hunting, incident response, and threat intelligence. Through proactive threat hunting, CrowdStrike’s experts actively search for signs of malicious activities to stop attacks before they cause damage. In the event of a security incident, their incident response services provide rapid and effective mitigation strategies to minimize the impact.

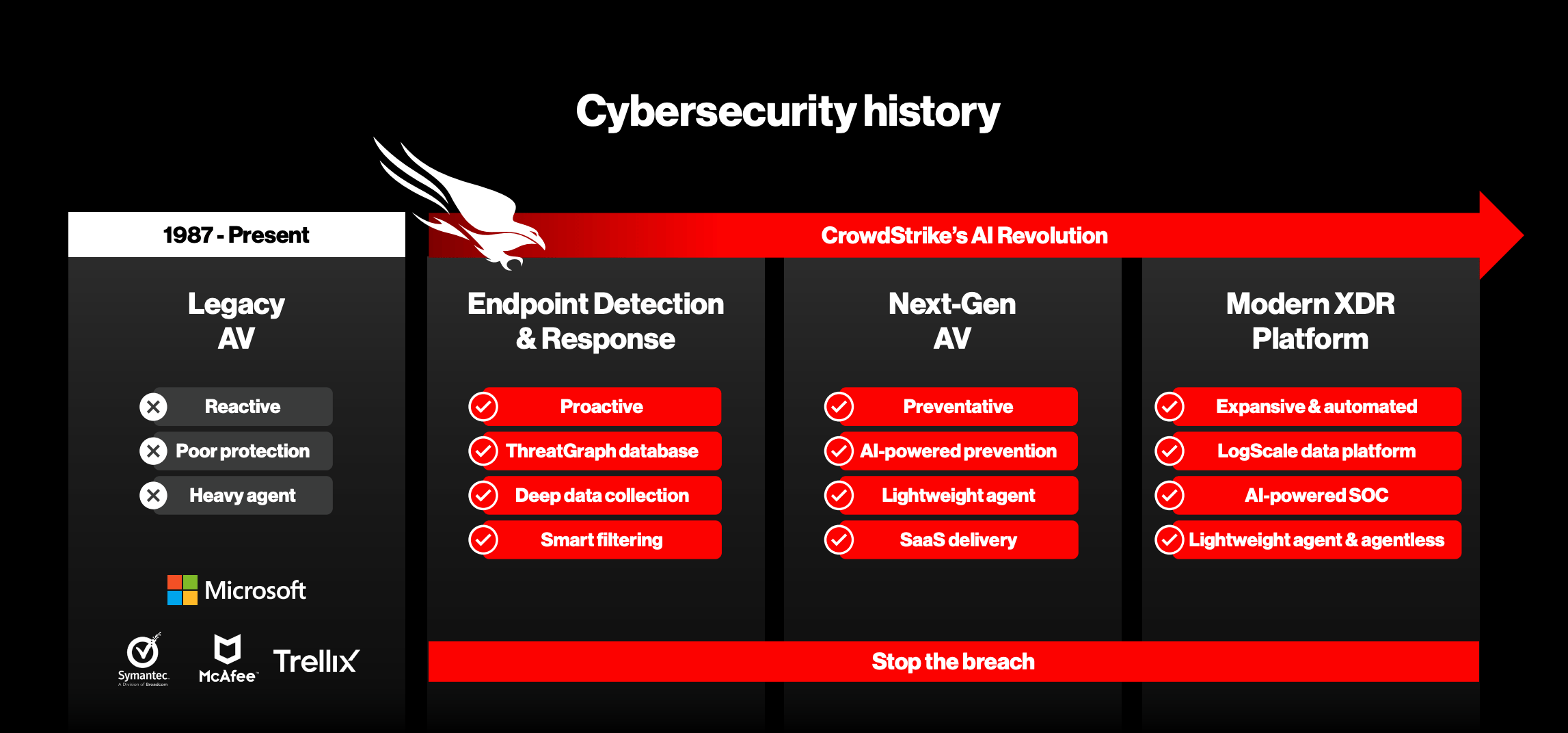

Cybersecurity Industry History (CrowdStrike April 2023 Investor Presentation)

CrowdStrike positions themselves as a “modern” solution to the ever-increasing problem of cybersecurity threats. They play against cybersecurity competitors including Microsoft’s Defender platform, as well as other companies such as Symantec (GEN), McAfee, and Trellix.

Thesis Explainer

As mentioned above, there are three key reasons why I see CrowdStrike to be an attractive buy at the moment.

1. Retention

CrowdStrike benefits from providing an extremely “sticky” service. It’s not every day that a company goes around looking to trade out its current cybersecurity software. Such software is one of those types of services where you’re most happy when you don’t hear anything from it, yet you’re happy to pay for it because of its critical value from a security standpoint.

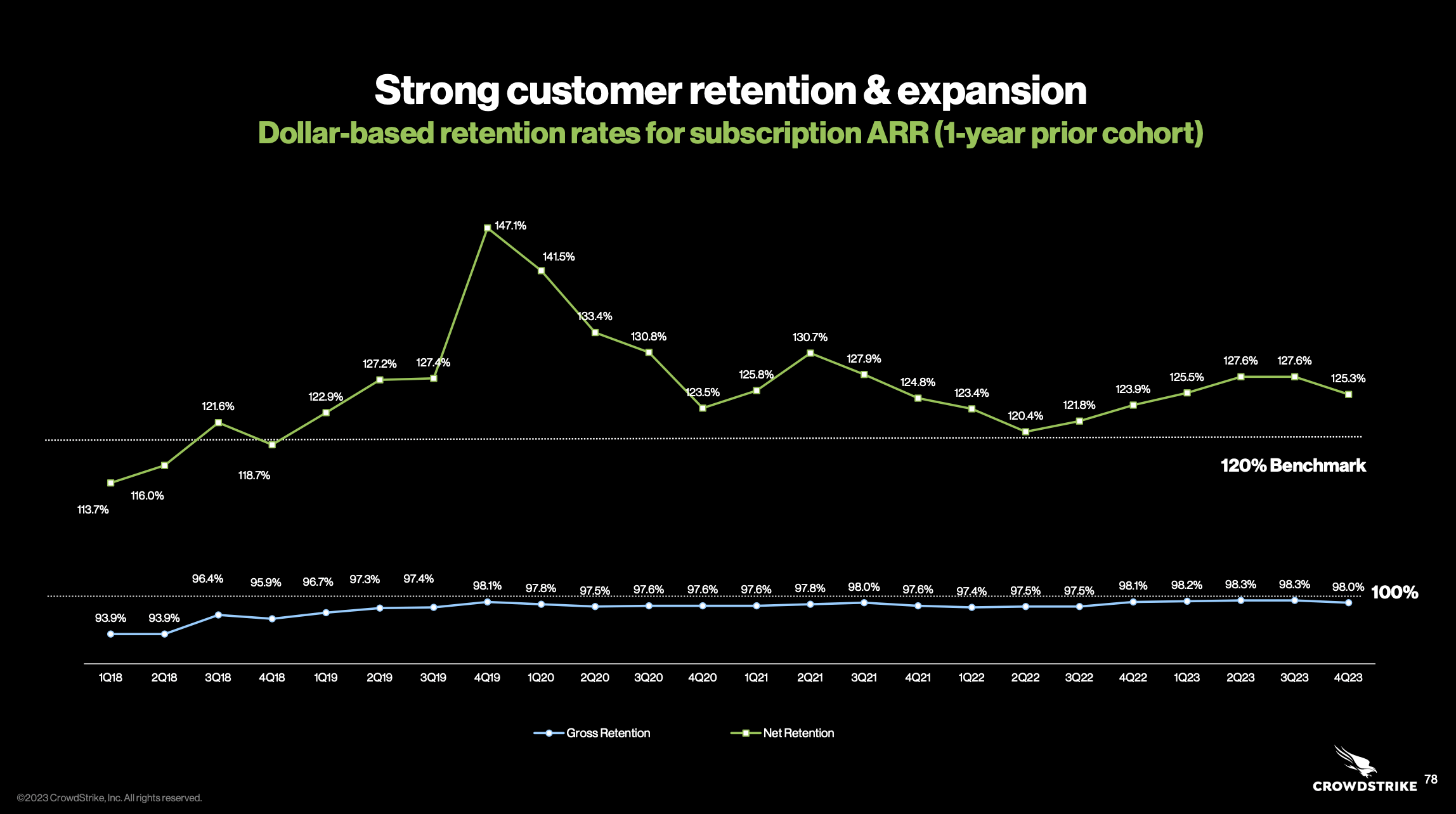

These industry characteristics, along with providing a great service, have helped CrowdStrike to enjoy incredibly high retention rates. Gross retention has exceeded 97% ever since the Q2 of 2019. Net retention has exceeded 120% every quarter since Q1 of 2019.

CrowdStrike’s gross and net retention over time. (April 2023 Investor Presentation)

These metrics illustrate just how sticky CrowdStrike’s revenue is. At such high retention rates, each new customer that is added is essentially stacking money on top of the ARR.

2. Doubling the “Rule of 40”

The Rule of 40 is a widely used financial guideline in the software industry that helps assess the overall health and growth potential of a company. It combines two key metrics: revenue growth rate and profitability. According to the Rule of 40, a company’s combined revenue growth rate and profitability should be equal to or greater than 40%. Free cash flow margin is commonly used as the profitability metric.

The concept behind this rule is that a company can prioritize either high growth or profitability, as long as the combined result remains above the threshold. For example, a company with a 20% growth rate and 20% free cash flow margin would meet the Rule of 40.

Companies that exceed the high 40% bar are generally considered to be beneficiaries of great businesses economics while simultaneously putting together rapid growth. This rule is particularly relevant for SaaS companies, where high growth is often prioritized to capture market share and gain a competitive edge.

With this in mind, CrowdStrike’s Rule of 40 score comes in at a whopping 85%. Yes, it is more than double the hurdle rate for what generally would be considered a great software business. Management touched on this in their latest conference call and investor presentation. The 85% score helps put in perspective just how healthy CrowdStrike’s margins are, while simultaneously growing at a whirlwind pace.

3. Discount from All-Time High

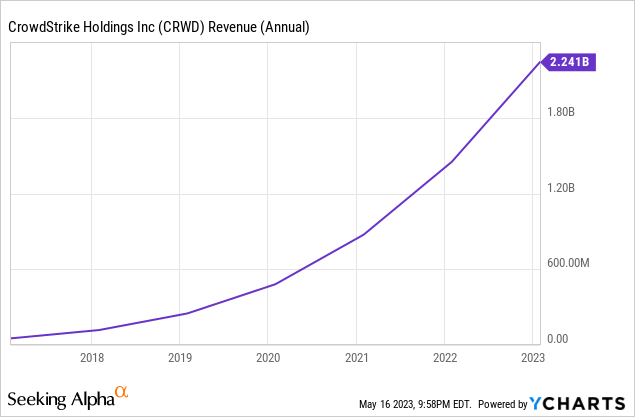

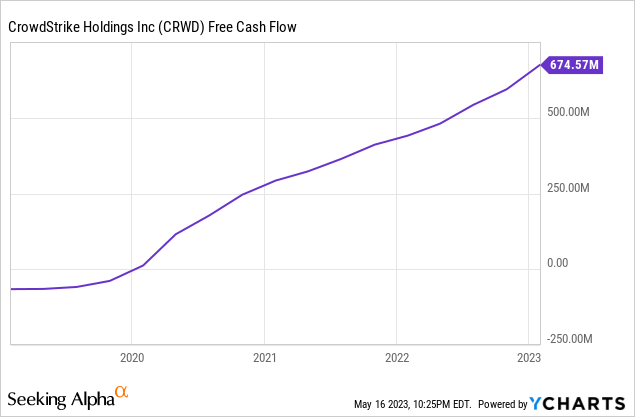

CrowdStrike’s stock price peaked at $280+ back in November of 2021. Currently, the stock is trading for ~$137, which represents a 50%+ discount from its all-time high. For context, CrowdStrike produced $874 million of revenue in all of 2021. Meanwhile, they are on track to do $2.2 billion of revenue in 2023. Furthermore, they had 2021 free cash flow totals of $293 million, but are on track to do $677 million in 2023.

Essentially, markets have created the opportunity to buy into CrowdStrike for 50% of its price from a year and a half ago, but with almost triple the revenue and more than double the free cash flow.

Financials

CrowdStrike’s financials are quite robust and impressive. They have been able to fuel substantial amounts of growth in a relatively short period of time, all while trending towards profitability. There were a couple things in particular that stood out from CrowdStrike’s financials.

Top-Line Growth

CrowdStrike has experienced rapid top-line growth ever since they IPO’d back in 2019. The company’s top-line revenue has grown at a blistering 80% CAGR, dating back to 2018.

CrowdStrike also believes that there is ample room left for growth. The company estimates a TAM of $20 billion for the endpoint security market, which is CrowdStrike’s core service. Additionally, when accounting for the rest of the company’s adjacent services, they estimate a cumulative TAM of $98 billion. Even if these estimates are optimistically over-inflated by management, they still stand to illustrate that there is plenty of room to gain market share.

Healthy Free Cash Flow Margin

CrowdStrike’s free cash flow margin exceeded 30% in both 2021 and 2022, and management expects it to remain above the 30% threshold for 2023. The company even anticipates the margin expanding above 30% over the next few years. Free cash flow for 2022 came in at a total of $442 million. Expanding free cash flow margins, coupled simultaneously with robust revenue growth, could help create significant value for investors.

The healthy margins will be key in helping CrowdStrike keep up the breakneck growth. Additionally, I wouldn’t be surprised to see CrowdStrike use some of the cash flow to invest in acquisitions to help fuel even more growth in the near future.

Valuation

Valuation is one of the few hesitations associated with CrowdStrike’s stock. By almost all traditional valuation multiples, CrowdStrike is considerably overvalued, at least when compared to the broader information technology sector. This includes multiples such as Price/Earnings (GAAP and Non-GAAP as well as TTM and FWD), Price/Sales, Price/Book, etc. Virtually the only common multiple that suggests CrowdStrike to be undervalued is the Non-GAAP Forward Price/Earnings Growth, which shouldn’t come as a surprise as CrowdStrike’s rapid growth is significant enough to offset an otherwise expensive price.

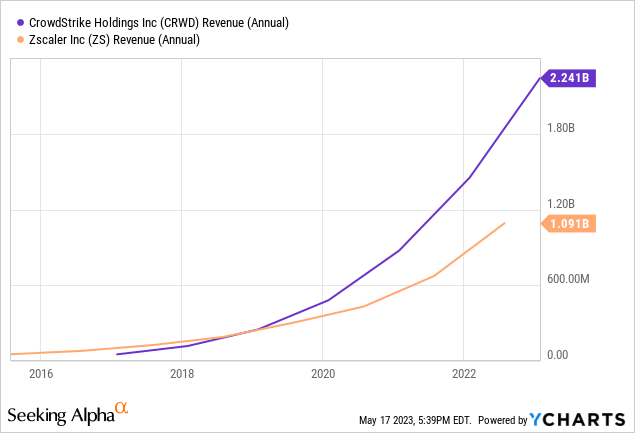

Although CrowdStrike may appear overvalued when compared to the IT sector as a whole, they don’t look quite as overvalued when compared to direct competitors. One of the best comparables for CrowdStrike would be Zscaler (ZS), another company specializing in cloud security. CrowdStrike currently has a market cap of ~$32 billion, whereas Zscaler’s is ~$17 billion.

As you can see from the graph above, revenues for the two companies were approximately equal back in 2018 and 2019. However, once CrowdStrike IPO’d in 2019, they started to pull away. Not only has CrowdStrike reached a larger scale than that of Zscaler, they also have been growing top-line at a faster rate. Couple those two factors together, and it’s going to be difficult for a company like Zscaler to catch back up to CrowdStrike.

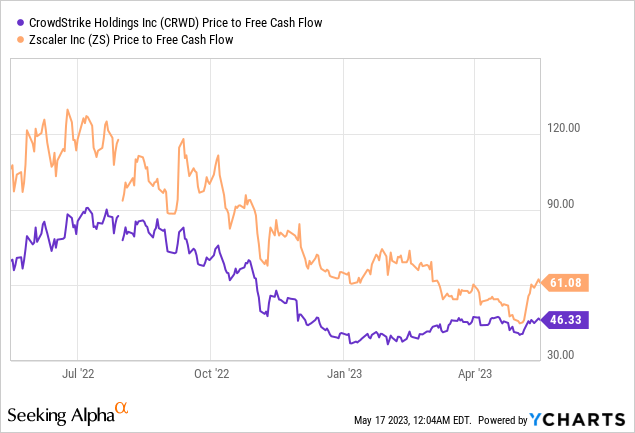

With CrowdStrike’s recent track record in mind, it’s interesting to see them currently priced cheaper than Zscaler in several multiples, such as the Price to Free Cash Flow multiple that is illustrated above. It’s worth noting as well that Zscaler also has a notably larger short interest at 9.5%, compared to CrowdStrike’s 3.4%.

Overall, CrowdStrike’s stock may initially appear expensive when compared to the broad IT sector. But upon further digging, and when compared to its direct competitors, the valuation looks much more manageable.

Catalysts

Warren Buffett once famously recommended that “if you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

CrowdStrike is a stock that I would be comfortable buying now, even if the market were to shut down and open back up in 10 years. It’s difficult to predict where the price will go in the near future, although Seeking Alpha’s momentum indicators suggest that it could be poised for a price bump, but it’s hard to imagine CrowdStrike not being incredibly valuable 10 years down the line. With the release of each quarter’s earnings, the quality of CrowdStrike’s business will become more and more apparent.

At the very least, I could see CrowdStrike’s stock experiencing a healthy jump when they begin producing positive net income by GAAP standards. The exact timeline for this is unknown, but some tentative projections suggest it may happen in 2025 or 2026.

Risks

Perhaps the greatest risk for CrowdStrike’s stock is that all of these positives that collectively make the company so attractive may already be fully priced in to the current price. There’s definitely a chance that this could be correct.

However, the markets tend to be rather erratic and short-sighted, especially for technology stocks such as CrowdStrike. By approaching the investment with a long-term horizon, investors could benefit greatly from the growth of the company over the next 5 or 10 years, and much of the short-term uncertainty will be ironed-out over time.

Conclusion

Overall, CrowdStrike stands out as an attractive investment opportunity. With exceptional retention metrics, doubling the “Rule of 40,” and a significant discount from its all-time high, CrowdStrike is well-positioned for the future. Although valuation comparisons to the broader IT sector may suggest overvaluation, when compared to direct competitors, CrowdStrike’s valuation appears more reasonable. The company’s long-term prospects and potential catalysts, coupled with its solid business fundamentals, make it an appealing long-term investment option, despite short-term market fluctuations and uncertainties.