CAVA Group Files For U.S. IPO To Fuel Expansion Plans (Pending:CAVA)

Mario Tama/Getty Images News

A Quick Take On CAVA Group, Inc.

CAVA Group, Inc. (CAVA) has filed to raise $100 million in an IPO of its common stock, according to an S-1 registration statement.

The firm operates a network of fast-casual Mediterranean restaurants in the United States.

CAVA has been growing quickly and reducing its operating losses, but growth may be less efficient in the future as its conversion of Zoes Kitchen locations to CAVA’s is completed.

I’ll provide a final opinion when we learn more information about the IPO from management.

CAVA Overview

Washington, D.C.-based CAVA Group, Inc. was founded to develop Mediterranean food and drink options for consumers at its 263-store-strong restaurant network in the U.S.

Management is headed by co-founder, President and CEO Brett Schulman, who has been with the firm since its inception in 2010 and was previously a Partner at Snikiddy Snacks, a snack food company, and has held various financial services industry positions prior.

The firm sources 85% of its ingredients directly from producers and growers. CAVA also has proprietary sauces and related CPG products.

As of April 16, 2023, CAVA has booked a fair market value investment of $682 million from investors, including Artal International S.C.A., T. Rowe Price, Act III, SWaN & Legend and Revolution Growth.

CAVA – Customer Acquisition

The firm locates its stores in high-traffic, high-visibility areas and advertises in various online and offline media to drive traffic.

CAVA is essentially seeking to become the ‘Chipotle’ of the Mediterranean food category and pursues an omnichannel approach to driving as much volume through each store, from in-person ordering to online as well.

General & Administrative expenses as a percentage of total revenue have trended higher as revenues have increased, as the figures below indicate:

|

General & Administrative |

Expenses vs. Revenue |

|

Period |

Percentage |

|

Sixteen Weeks Ended April 16, 2023 |

14.3% |

|

FYE Ended December 25, 2022 |

12.4% |

|

FYE Ended December 26, 2021 |

13.0% |

(Source – SEC)

The General & Administrative efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of General & Administrative expense, rose to 1.5x in the most recent reporting period, indicating increasing efficiency in this regard, as shown in the table below:

|

General & Administrative |

Efficiency Rate |

|

Period |

Multiple |

|

Sixteen Weeks Ended April 16, 2023 |

1.5 |

|

FYE Ended December 25, 2022 |

0.9 |

(Source – SEC)

CAVA’s Market & Competition

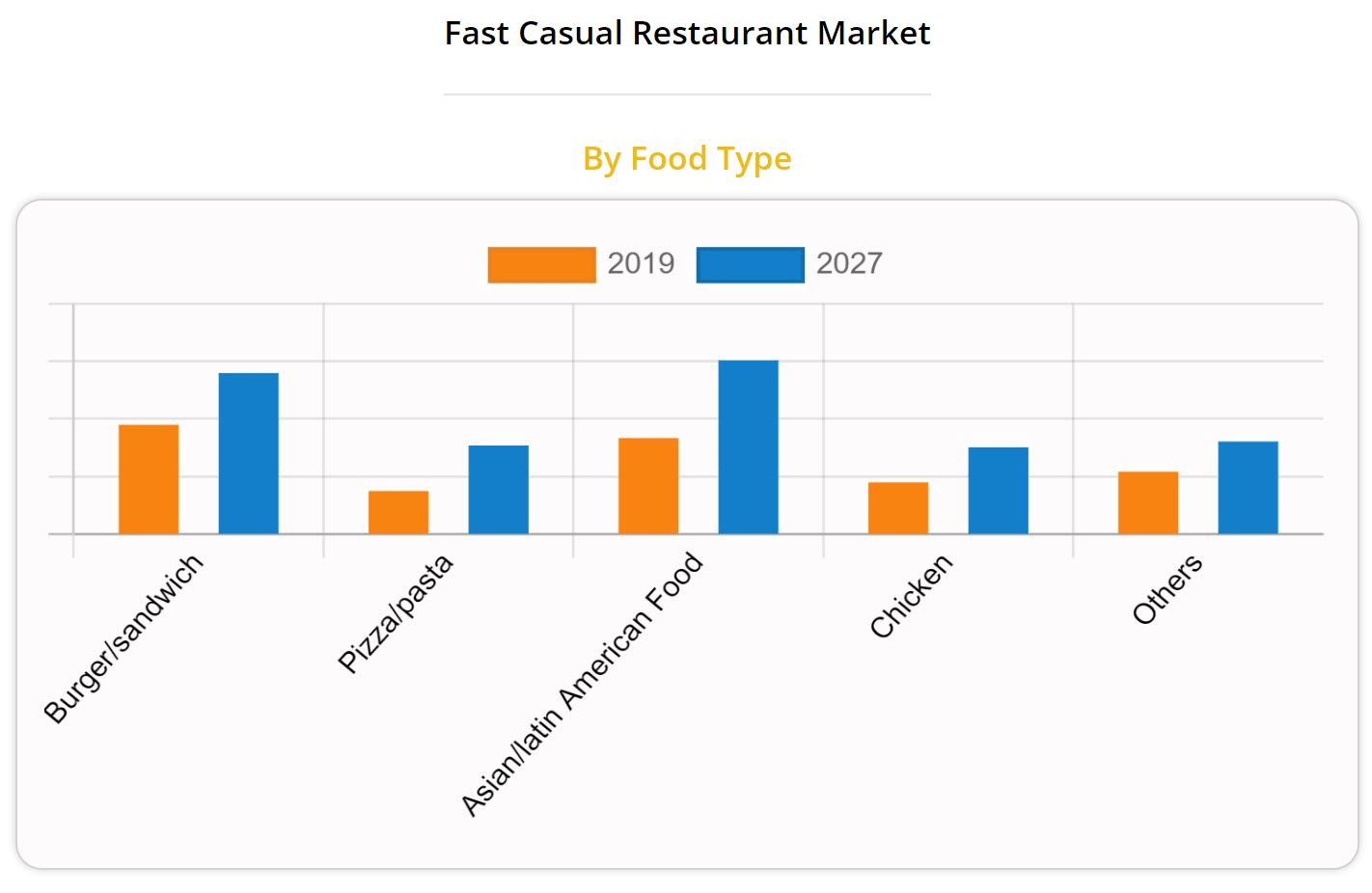

According to a 2020 market research report by Allied Market Research, the global fast-casual restaurant market size was an estimated $126 billion in 2019 and is forecast to reach $209 billion by 2027.

This represents a forecast CAGR (Compounded Annual Growth Rate) of 10.6% from 2021 to 2027.

The main drivers for this expected growth are increased automation in food preparation and the growth of delivery-to-door companies and other online digital lines.

Also, the Asian/Latin American food type is expected to grow the fastest through 2027, as the chart shows below:

Fast-Casual Restaurant Market (Allied Market Research)

The firm faces competition from numerous other fast-casual type restaurants offering various food types.

CAVA Group, Inc. Financial Performance

The company’s recent financial results can be summarized as follows:

-

Increasing topline revenue growth

-

Higher gross profit and gross margin

-

Sharply reduced operating loss

-

Substantial growth in cash flow from operations

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

Sixteen Weeks Ended April 16, 2023 |

$203,083,000 |

27.7% |

|

FYE Ended December 25, 2022 |

$564,119,000 |

12.8% |

|

FYE Ended December 26, 2021 |

$500,072,000 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

Sixteen Weeks Ended April 16, 2023 |

$50,564,000 |

128.3% |

|

FYE Ended December 25, 2022 |

$97,984,000 |

19.3% |

|

FYE Ended December 26, 2021 |

$82,153,000 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

% Variance vs. Prior |

|

Sixteen Weeks Ended April 16, 2023 |

24.90% |

11.0% |

|

FYE Ended December 25, 2022 |

17.37% |

5.7% |

|

FYE Ended December 26, 2021 |

16.43% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

Sixteen Weeks Ended April 16, 2023 |

$(2,252,000) |

-1.1% |

|

FYE Ended December 25, 2022 |

$(59,766,000) |

-10.6% |

|

FYE Ended December 26, 2021 |

$(52,752,000) |

-10.5% |

|

Net Income (Loss) |

||

|

Period |

Net Income (Loss) |

Net Margin |

|

Sixteen Weeks Ended April 16, 2023 |

$(2,141,000) |

-1.1% |

|

FYE Ended December 25, 2022 |

$(58,987,000) |

-29.0% |

|

FYE Ended December 26, 2021 |

$(37,391,000) |

-18.4% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

Sixteen Weeks Ended April 16, 2023 |

$25,679,000 |

|

|

FYE Ended December 25, 2022 |

$6,038,000 |

|

|

FYE Ended December 26, 2021 |

$3,393,000 |

|

(Source – SEC)

As of April 16, 2023, CAVA had $22.7 million in cash and $392.7 million in total liabilities.

Free cash flow during the twelve months ending April 16, 2023, was negative ($86.9 million).

CAVA Group, Inc. IPO Details

CAVA intends to raise $100 million in gross proceeds from an IPO of its common stock, although the final figure may differ.

No existing shareholders have indicated an interest in purchasing shares at the IPO price.

The firm is an ‘emerging growth company’ as defined by the 2012 JOBS Act and has elected to take advantage of reduced public company reporting requirements; prospective shareholders will receive less information for the IPO and in the future as a publicly-held company within the requirements of the Act.

Management says it will use the net proceeds from the IPO as follows:

We intend to use the net proceeds to us from this offering for new restaurant openings and for general corporate purposes.

(Source – SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, the firm is the subject of a ‘purported class action complaint relating to organic fluorine and PFAS in the packaging of its grain and salad bowls.’ The company is also subject to a false and deceptive advertising claim related to its alleged use of PFAS in its packaging.

The company is defending itself. Management states, ‘an estimate of reasonably possible losses or range of losses (if any) cannot be made and the final outcomes are uncertain.’

The listed bookrunners of the IPO are J.P. Morgan, Citigroup, and other investment banks.

Commentary About CAVA’s IPO

CAVA is seeking U.S. public capital to expand the firm in the United States via growing its network of restaurant locations.

The firm’s financials have shown higher topline revenue growth, increased gross profit and gross margin, sharply lowered operating loss and strong growth in cash flow from operations.

Free cash flow for the twelve months ending April 16, 2023, was negative ($86.9 million).

General & Administrative expenses as a percentage of total revenue have trended higher as revenue has increased; its General & Administrative efficiency multiple rose to 1.5x in the most recent reporting period, indicating greater efficiency in its cost structure.

The firm currently plans to pay no dividends and to retain near-term future earnings for its growth and working capital requirements.

CAVA’s recent capital spending history indicates it has spent heavily on capital expenditures as it continues to open new stores, which require significant capital outlays.

The market opportunity in the fast-casual restaurant industry is expected to grow at a low double-digit rate of growth in the coming years, so the firm enjoys reasonably strong industry growth dynamics.

J.P. Morgan is the lead underwriter, and IPOs led by the firm over the last 12-month period have generated an average return of 7.4% since their IPO. This is a mid-tier performance for all major underwriters during the period.

Risks to the company’s outlook as a public company include its ability to find suitable real estate locations at a reasonable cost.

Recently, its growth has been enhanced by converting a number of Zoes Kitchens locations into CAVA restaurants. Once this process is completed, its future growth rate may decline or become more expensive to maintain.

When we learn more about management’s assumptions on IPO pricing and valuation, I’ll provide an update.

Expected IPO Pricing Date: To be announced.