C3.ai: Bear With This Company As It Executes A Turnaround (NYSE:AI)

hapabapa

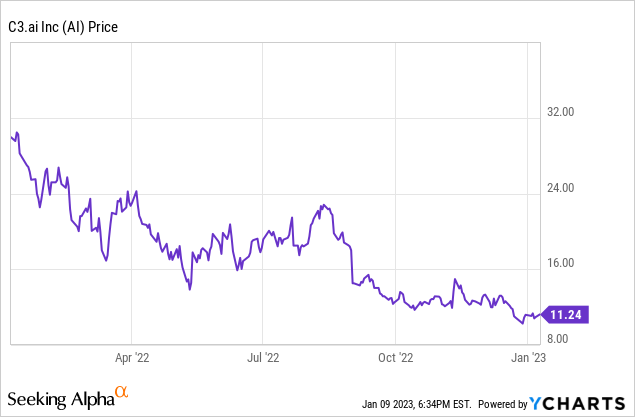

It’s truly surprising how quickly some high-flying tech stocks went from being Wall Street favorites to dumpster stocks. Such is the case for C3.ai (NYSE:AI), a platform software company that helps organizations build and deploy AI applications. Originally a hot recent IPO that traded at double-digit revenue multiples, C3.ai has largely been forgotten – especially as the pandemic brought on execution challenges and a slowdown in growth.

Over the past twelve months, shares of C3.ai have lost more than 60% of their value. It’s a great time, in my view, for investors to survey the damage and look at this company with fresh eyes.

I remain bullish on C3.ai, and I believe that the company makes for a strong rebound play (the only reason I am not at very bullish as in my prior outlook is solely for the fact that so many other SaaS companies have seen tremendous falls in valuation recently, and on a relative basis C3.ai is no longer a stark standout among bargain plays).

Recall that C3.ai just switched over its business model to bill customers based on usage/consumption rather than subscriptions. Though this transition will mean a near-term impact to revenue growth, there are two benefits with this transition: 1) in the long run, large customers who rely heavily on C3.ai’s platform will generate more revenue (i.e., high net revenue retention rates), 2) consumption-based pricing can lower the barrier to entry for smaller customers who want to deploy C3.ai for specific applications and use cases, which will help C3.ai’s goal of expanding its customer base – something that investors have called for since the company’s IPO.

Yes, this does mean that investing in C3.ai requires a little bit of faith in the company’s execution as it tries something new – but so far, we’ve seen encouraging results, as we’ll review in the company’s Q2 highlights in the next section.

Here are all the reasons to be bullish on C3.ai in the long run:

- Industry diversification. AI is a “horizontal” technology, meaning it can be equally applied and benefited from by companies in any industry. Historically, C3.ai has concentrated in heavy manufacturing and oil, due to its relationship with Baker Hughes. More recently, however, the company has expanded applications in production to cover customers in financial services, healthcare, and other expansion industries for C3.ai.

- Solid partnerships. C3.ai is well-embedded with Amazon AWS, Google Cloud, and Microsoft Azure, with specific enterprise applications that are optimized for different cloud environments. C3.ai’s cloud-agnostic approach gives it broader reach across all potential customers.

- Powerful technology. C3.ai is one of the best-recognized names in enterprise AI transformation, which is an area that will only continue to receive more corporate investment as businesses look to modernize and automate their operations.

- Rich cash balances. C3.ai has just shy of $1 billion in cash on its most recent balance sheet, unencumbered of debt – giving it plenty of financial flexibility as it works toward its goal of hitting pro forma breakeven by the end of FY24.

- Star leadership. C3.ai’s CEO, Tom Siebel, is a well-known software industry veteran, best known for selling his startup Siebel Systems to Oracle for $5.8 billion.

From a valuation standpoint: at current share prices near $11, C3.ai trades at a market cap of $1.24 billion. After we net off the $858.8 million of cash on the company’s most recent balance sheet, C3.ai’s resulting enterprise value is just $382 million – essentially, the majority of C3.ai’s market value sits in cash!

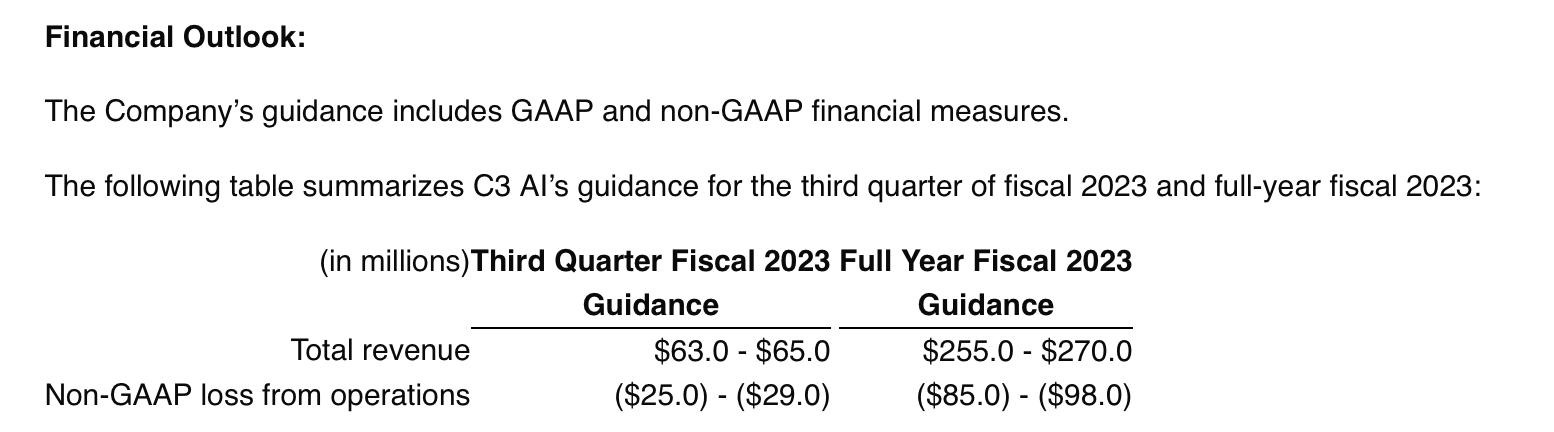

Meanwhile, for the current fiscal year FY23, C3.ai has guided to revenue of $255-$270 million, representing 1-7% y/y growth (recall again that this is held down by the near-term impact of the consumption business model change).

C3.ai outlook (C3.ai Q2 earnings release)

At the midpoint of this range, C3.ai trades at just 1.5x EV/FY23 revenue – which to me is quite undervalued for a software company with ~70% pro forma gross margins and a base of blue-chip enterprise customers. Stay long here and use the dip as a buying opportunity.

Q2 download

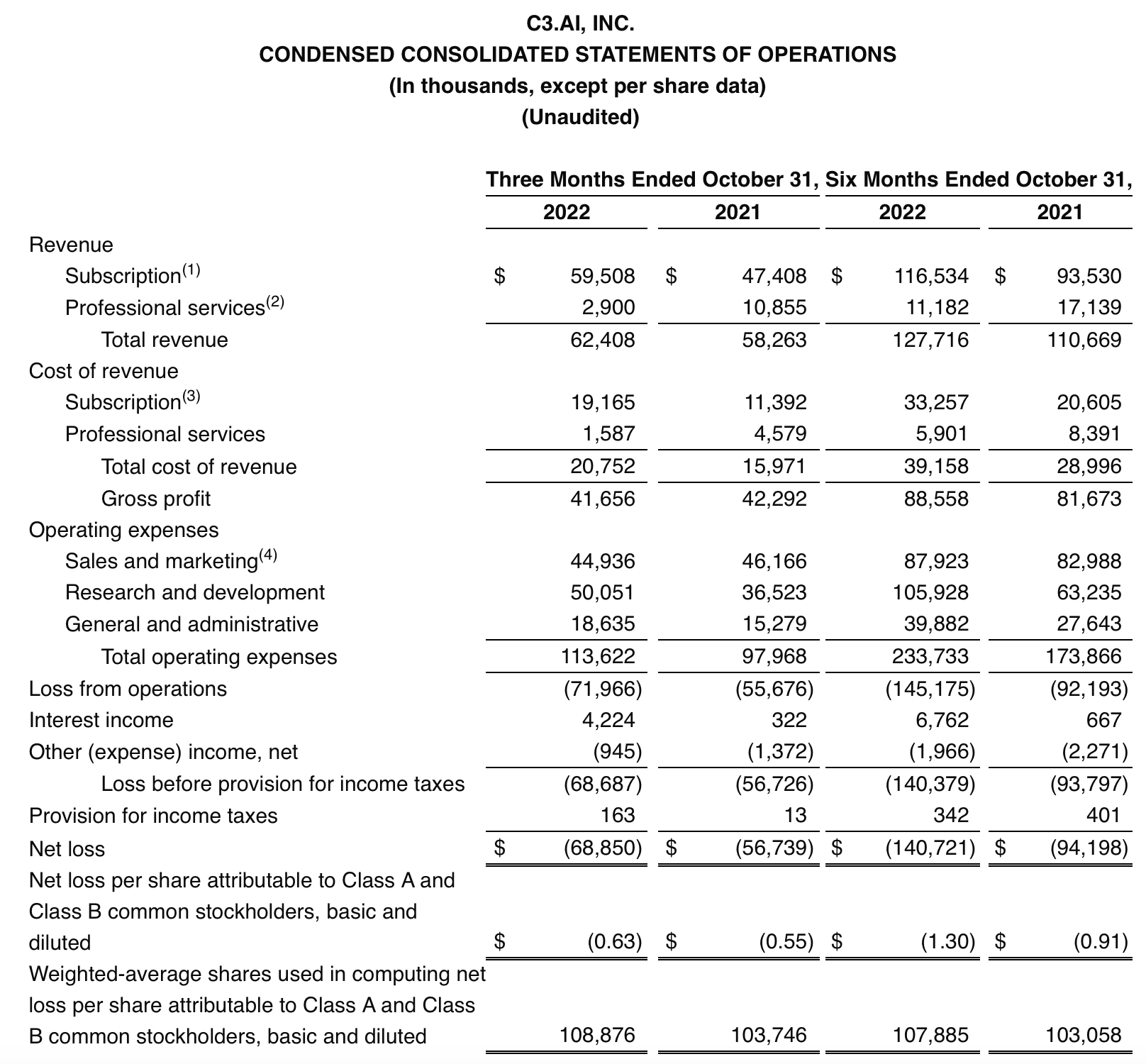

Let’s now go through C3.ai’s latest quarterly results in greater detail. The Q2 earnings summary is shown below:

C3.ai Q2 results (C3.ai Q2 earnings release)

C3.ai’s revenue grew 7% y/y to $62.4 million, beating Wall Street’s expectations of $60.8 million (+4% y/y) by a three-point margin. Revenue growth decelerated sharply from 25% y/y growth in Q1, owing to the change to a consumption-based model which will recognize more revenue on a pay-as-you-go basis.

The company notes that its business model transition has been successful so far at bringing in more deals. Per CEO Tom Siebel’s remarks on the Q2 earnings call:

In the last earnings call, we described two strategic initiatives to spur faster growth. One was to recompose our sales team with an emphasis on technical and domain expertise. The second was to shift our pricing model from a subscription-based pricing model to a consumption-based pricing model. I’m happy to report these initiatives have been successfully completed in the second quarter […]

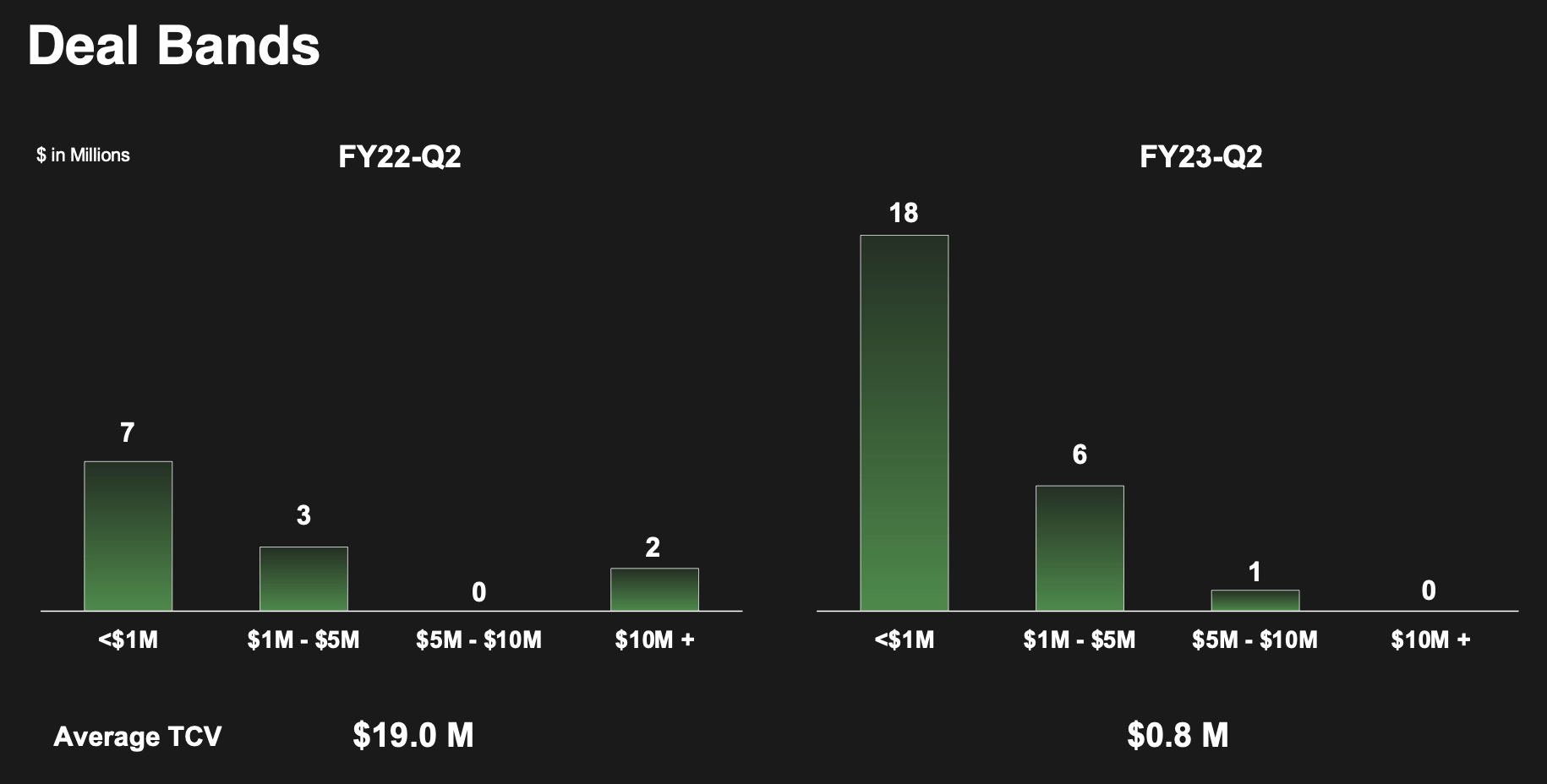

The number of completed contracts in the quarter increased to 25, approximately a 100% increase year-over-year. Our average contract value in the second quarter was just over $800,000, down from $19 million a year earlier. This reduction in contract value was a direct result of our new pricing model. We believe the new pricing model will result in a substantially increased number of smaller transactions, providing greater forward visibility in both revenue and bookings.

Our new consumption-based pricing model was well-received by our customers, our prospects, our partners and by our sales organization. We expect this new model to increase the number of customers with which we engage in any given quarter by an order of magnitude. As these customers continually increase their usage over time, we expect the compound effect on revenue growth to be quite significant.”

To illustrate the point above, see the slide below: total deals completed in the quarter grew, but most of them are sitting in the <$1 million space. The hope is that these customers will expand their usage and billings over time:

C3.ai deal metrics (C3.ai Q2 earnings release)

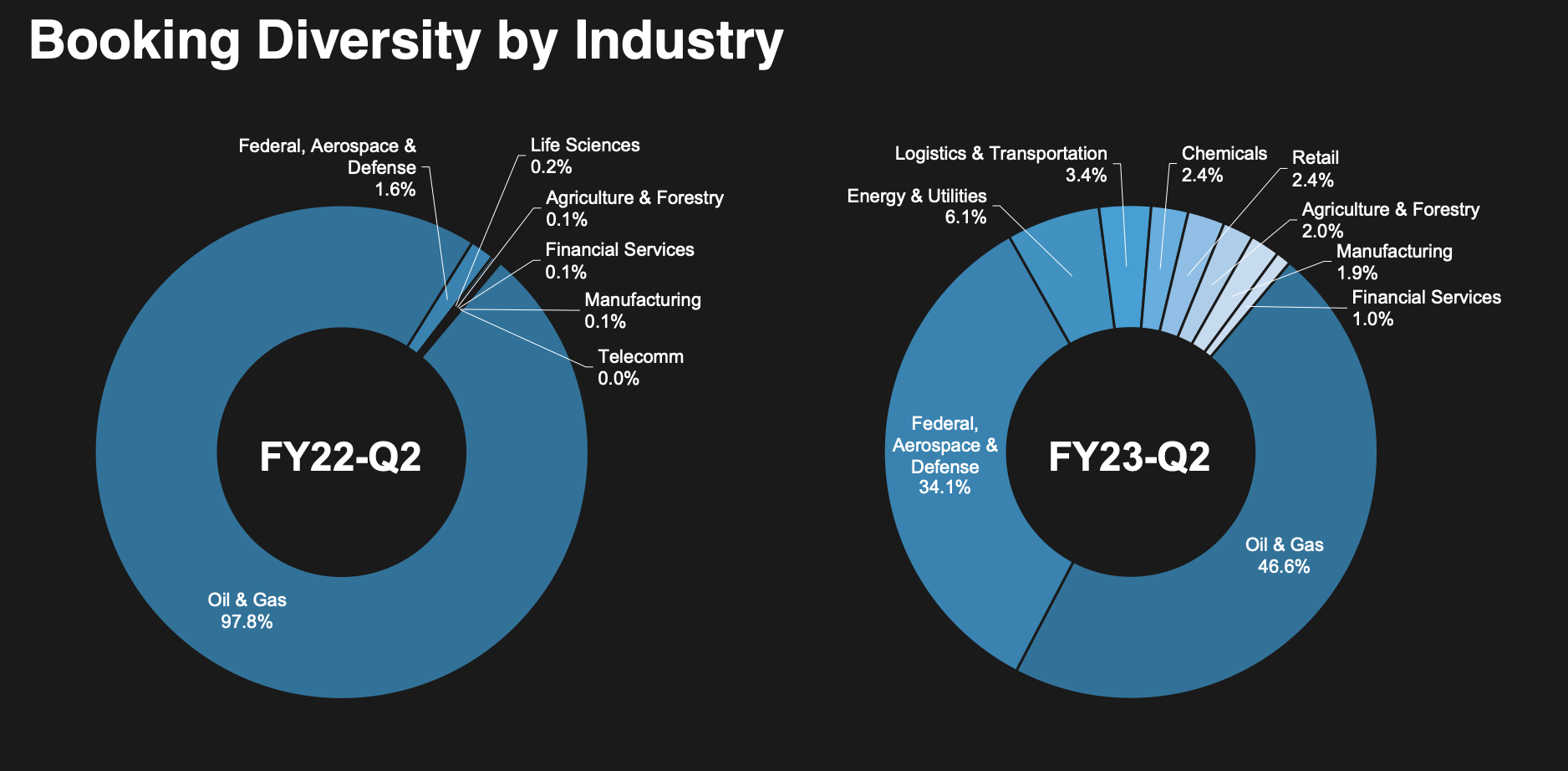

C3.ai has also done a good job diversifying its customer pool. As shown in the chart below, oil and gas bookings (driven largely through the company’s partnership with Baker Hughes) now make up less than half of overall revenue: versus the overwhelming majority in the prior-year quarter.

C3.ai Q2 bookings mix by industry (C3.ai Q2 earnings release)

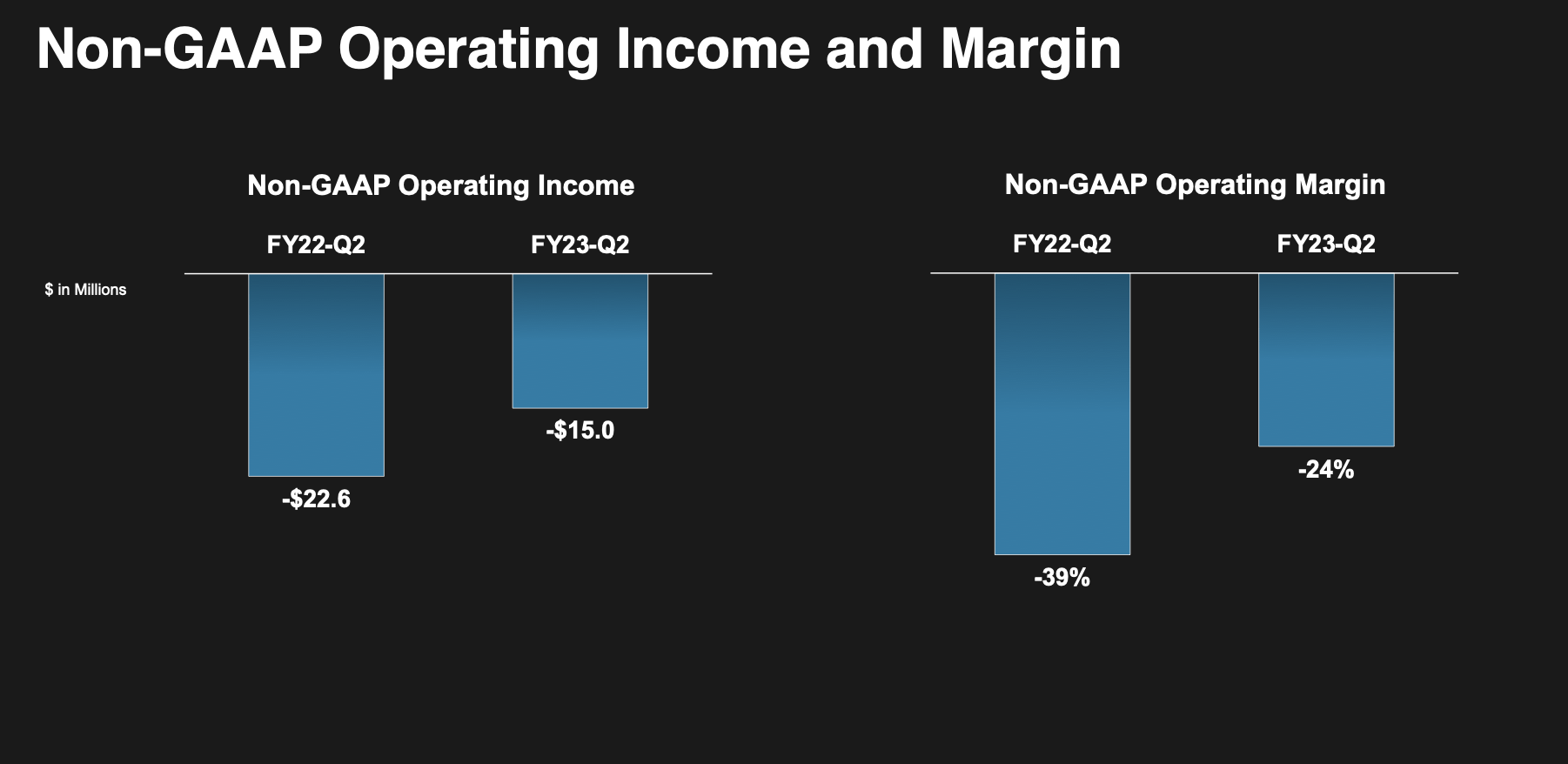

It’s worth noting as well that the company substantially improved pro forma operating margins to -24%, a fifteen-point boost versus -39% in the year-ago Q2. Reminder that the company expects to be above breakeven by the end of FY24, or April 2024.

C3.ai Q2 pro forma margins (C3.ai Q2 earnings release)

Key takeaways

In my view, C3.ai is effectively trading next to free. Yes, there is uncertainty as the company faces optical deceleration from its business model transition, but I think there are plenty of green shoots coming from the company’s uptick in deals closed plus its improvement in margins. Stay long here.