British American Tobacco: Huge Opportunities In New Products

AndreyPopov

Investment Thesis

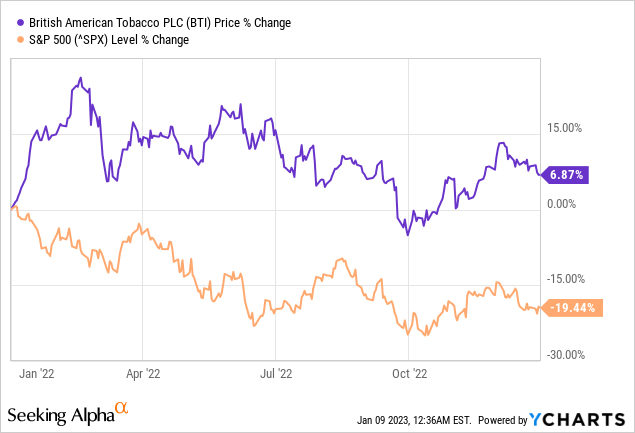

British American Tobacco (NYSE:BTI) has been underperforming the broader indexes since the massive drop in 2018. However, the company’s share price showed surprisingly strong resilience last year, up 18.4% compared to the S&P 500 Index which is down 19.4%. I believe the company’s strong momentum could continue this year.

As the inflation rate continues to be highly elevated with a recession potentially coming soon, tobacco companies like British American Tobacco may be a good place to hide due to their sticky customer base and strong pricing power. The company also has new product categories that are growing rapidly as the global adoption of non-combustible products continues to accelerate. This alongside resilient combustible product sales should allow British American Tobacco to see decent top-line growth in the near term. The company’s current valuation is also very compelling compared to peers, not to mention the high dividend yield investors can secure at the current price. Therefore I rate British American Tobacco as a buy at the current price.

New Product Growth

British American Tobacco is undergoing a pivotal transformation that will open up many more opportunities going forward. While the sales volume of combustible products is poised to slow down due to tighter regulatory environments across the globe, non-combustible products are gaining significant traction. I believe the company has a massive growth runway for its new category products, which currently include Vuse, an electronic cigarette brand, Glo, a heating tobacco brand, and Velo, a nicotine pouch brand.

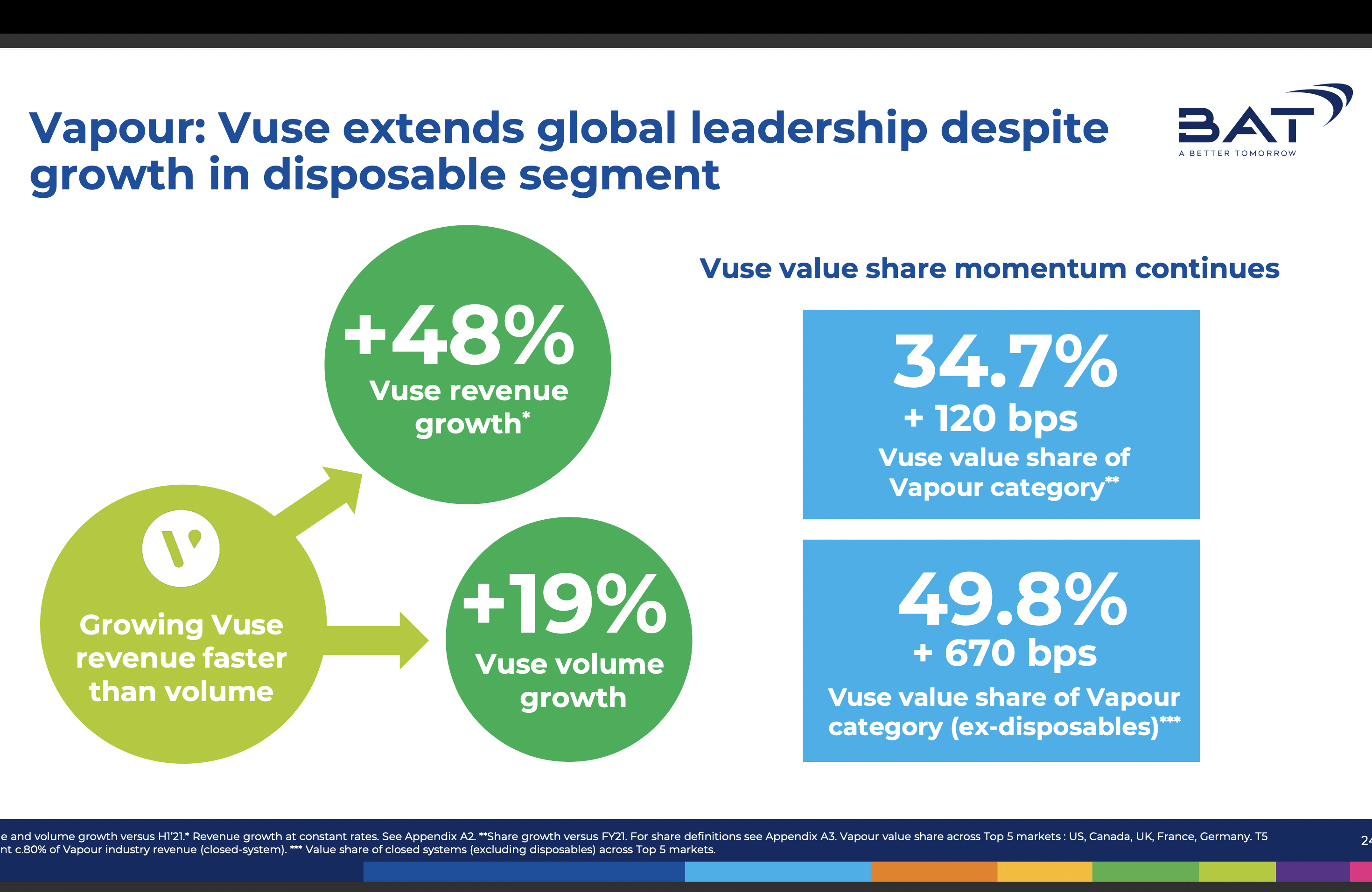

The total addressable market or TAM for non-combustible products is huge. According to Grand View Research, the global e-cigarette and vapor market size was approximately $22.5 billion in 2022 and is forecasted to grow to $182.8 billion in 2030, representing a CAGR (compounded annual growth rate) of 30.6%. In 2022, Vuse overtook Juul to become the US e-cigarette market leader with a 39.7% market share as Juul is now facing a potential retain ban from the FDA, which continues to benefit Vuse.

British American Tobacco

For heating tobacco products, the global addressable market is currently around $17.1 billion and is expected to grow at a CAGR of 32.8% to $68.3 billion in 2027. Glo is an emerging brand with a volume share of 19.6%. It has been steadily gaining market share in key markets such as Japan and Italy. Volume share was up 1.6 points in the latest quarter with revenue up 44%.

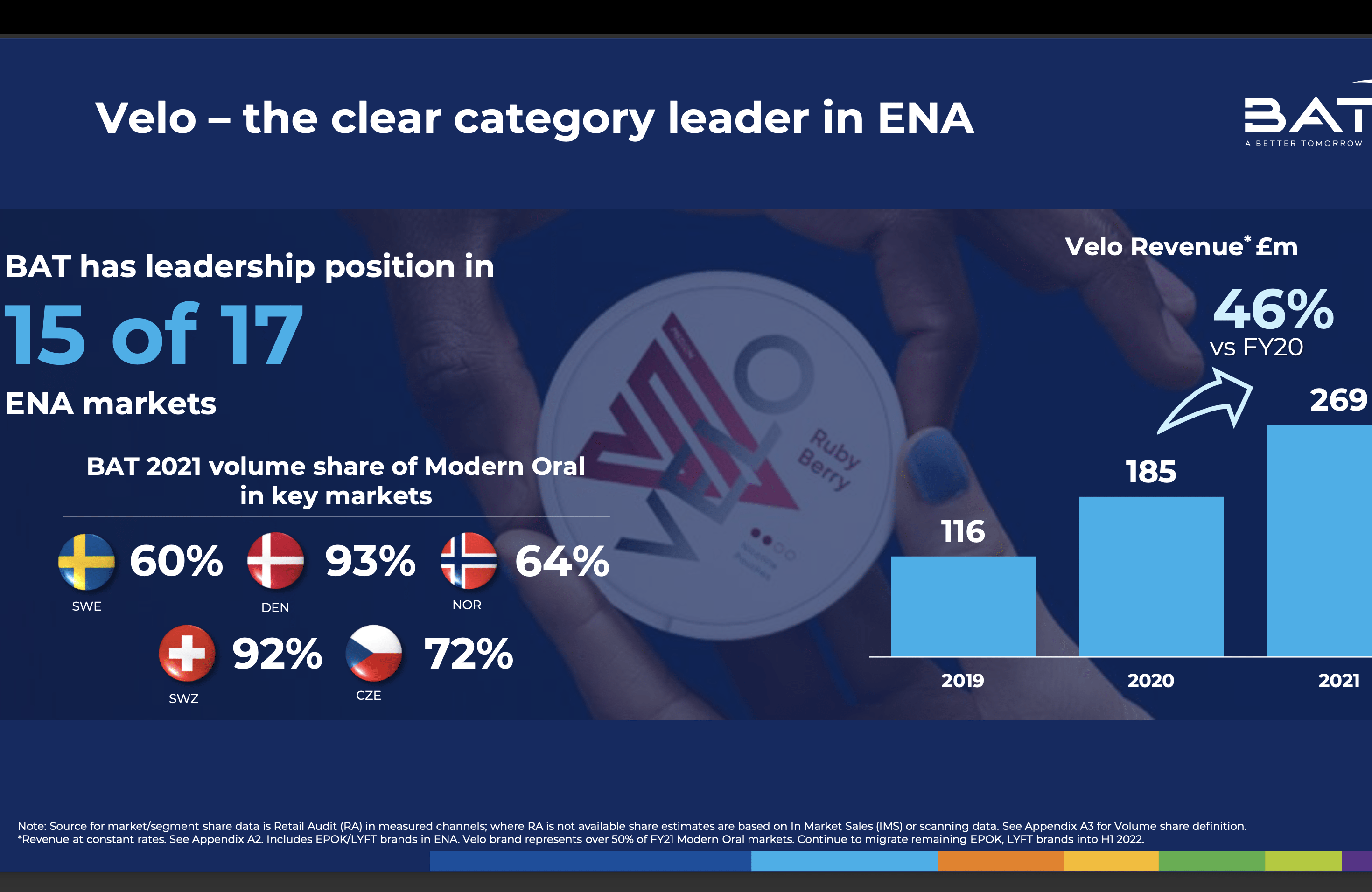

Last but not least, the current global addressable market for nicotine pouches is around $2 billion and is forecasted to expand to $23 billion in 2030, representing a CAGR of 35.7%. Velo is currently ranked third in the US with a 12.1% market share, therefore rather than targeting the US market, Velo now focuses mainly on the European market. It is the dominant leader in different countries such as Denmark, Sweden, and Switzerland. For example in Switzerland, the brand has a volume share of 92%, according to British American Tobacco.

British American Tobacco

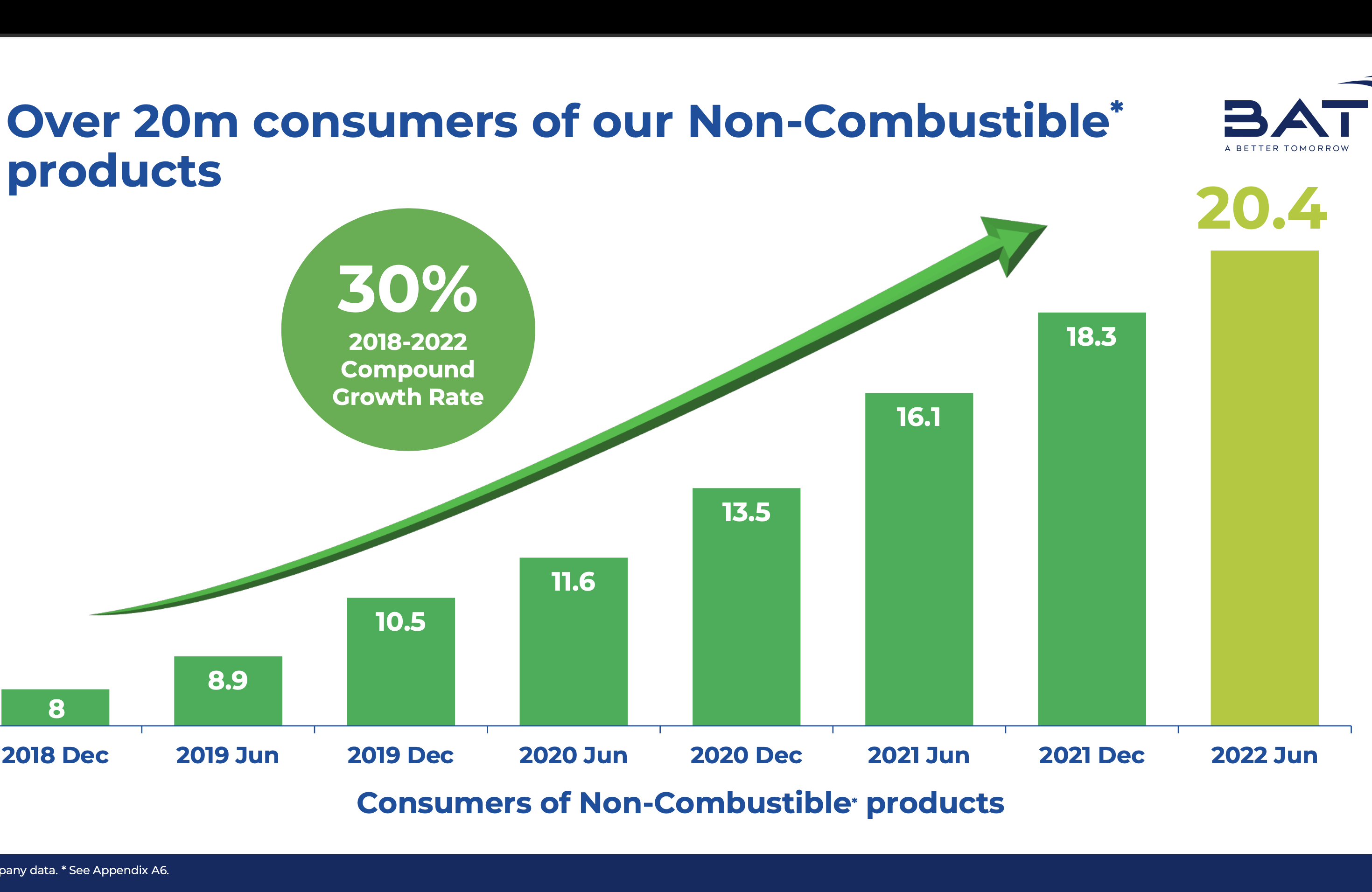

These products have been gaining popularity as they impose lower health risks and have less regulation in most countries. Most young adults are now inclined to choose non-combustible products while a decent portion of existing smokers also considers switching. In H1 2022, revenue for new products increased by 45% while consumers of these products increased to 20.4 million. The company expects new category revenue to grow to $6.1 billion in 2025 at a CAGR of 25%. I believe the actual growth rate could be higher as the market is also expanding rapidly, which will further lift British American Tobacco’s top-line growth in the coming years.

British American Tobacco

Valuation

British American Tobacco is seeing huge growth opportunities for its new product segment yet the market seems to be overlooking it. The company continues to trade at a discounted valuation when compared to peers like Altria (MO) and Philip Morris (PM), as shown in the chart below (I am using EV/EBITDA ratio as it takes the debt level into account). I believe the valuation gap is not justified as British American Tobacco is expected to post 3%–5% group revenue growth with a high single-digit EPS growth for the medium term, led by non-combustibles while Altria and Philip Morris are expected to grow both revenue and EPS at a low single-digit (according to Seeking Alpha’s analyst estimate). The company has also been actively de-leveraging to maintain a healthier balance sheet. The adjusted net debt / EBITDA ratio has dropped from 4x in 2018 to around 2.9 currently, driven by its strong cash flow. I believe British American Tobacco should at least be trading at levels similar to peers which will offer a 28%+ plus upside.

Risks

I believe regulation will continue to be the biggest risk here. British American Tobacco has operations in many countries each with different regulations and laws. As governments across the globe continue to emphasize the importance of health, ESG, and sustainability, I wouldn’t be surprised if some countries start to impose stricter regulations on products like e-cigarettes. Altria has also recently appealed the ban on its Juul product and if deemed successful, it could continue to be sold in the US which will significantly increase the competition for Vuse. While I do think the chances of these scenarios happening are low, it is still worth keeping an eye on as it could post unprecedented headwinds on the company.

Conclusion

In conclusion, I believe British American Tobacco is a good buy here. The combustible segment should hold up pretty well even if we enter a recession as it continues to be one of the stickiest consumer staples. Volume may drop a bit which is expected but price increases should be able to make up for it. The new product categories are likely to see strong momentum as the adoption of non-combustible continues. I believe the market will soon warrant the company with a higher multiple thanks to its new growth prospect. There are certainly regulatory risks as always but a lot of it has been priced in given the compressed multiple. The current valuation is very compelling and an upward revision back to peers’ level will already provide a decent upside. I rate the company as a buy.