Argan: A High Quality Pick For 2023 (NYSE:AGX)

Drazen_

Investment Thesis:

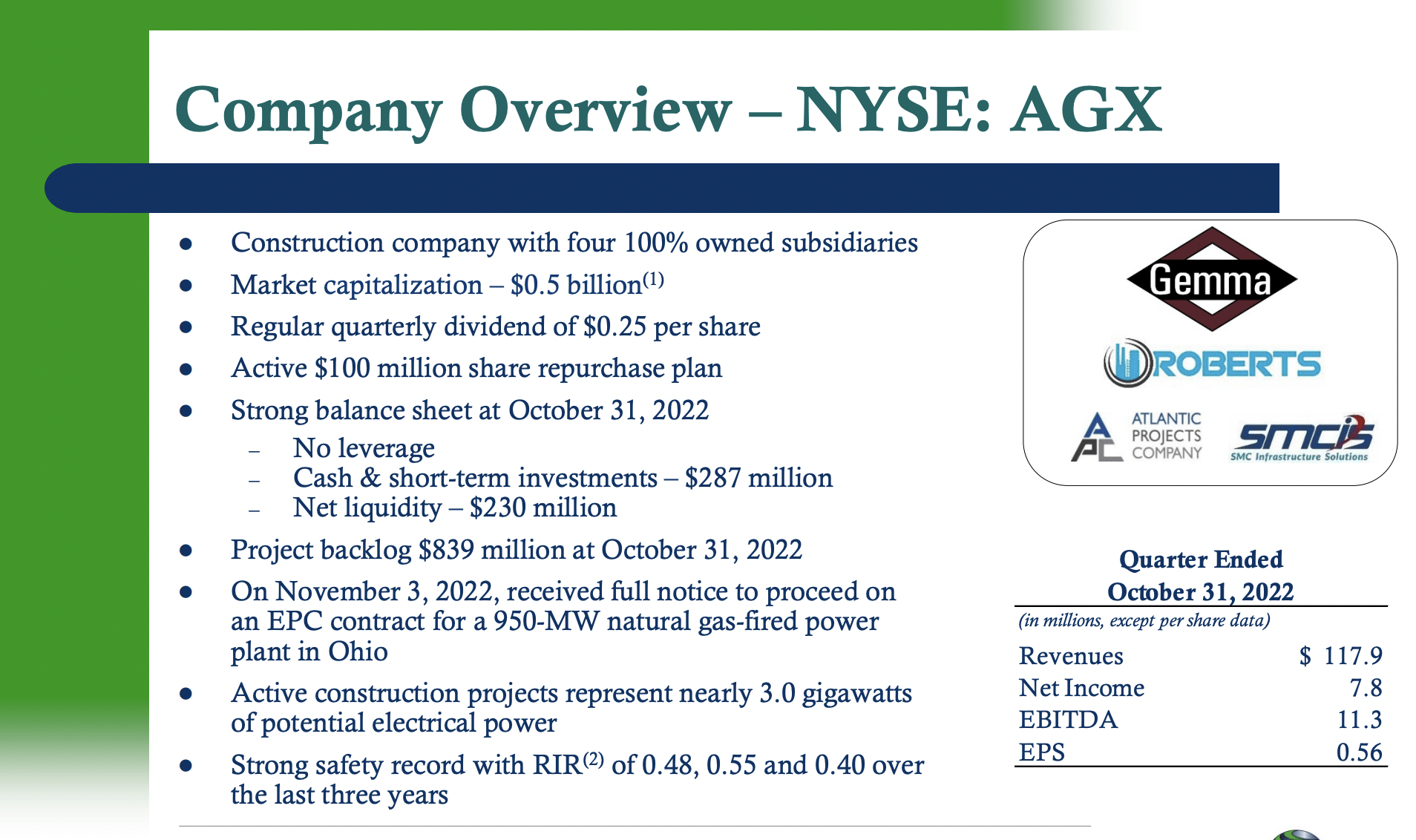

Argan (NYSE:AGX) is a $500 million company that conducts their operations through their subsidiaries Gemma Power Systems (GPS), Atlantic Projects Company (APC), The Roberts Company (TRC), and Southern Maryland Cable (SMC). Through these subsidiaries, Argan provides a range of construction and engineering services for the power generating market which includes the rapidly growing renewable energy sector. Their primary operations take place in the United States, Ireland, and the United Kingdom of which the large majority of the revenue comes from the United States. Moreover, GPS and APC who provide power industry services, accounted for 78% of their total revenues in fiscal 2022 while their other subsidiaries made up the rest.

I believe that Argan is significantly undervalued and will provide market beating returns due to a large discount from their intrinsic value when utilizing conservative assumptions. Argan has the ability to rapidly grow their revenues as they complete their project backlog and capitalize on the potential of the renewable energy sector, execute their tremendous share buyback program, and warrant a larger multiple regarding net income and free cash flow as a result of their high ROIC and forward EPS growth.

Argan Company Overview (Argan Investor Relations presentation)

Financial Breakdown:

Argan is in a phenomenal financial state as they have been able to maintain steady operating margins while possessing an extremely strong balance sheet that has excess capital nearing 50% of their market while rapidly diminishing share count. The primary negative component of their financials is that they have inconsistent free cash flow due to large fluctuations in contract assets and liabilities.

Income Statement:

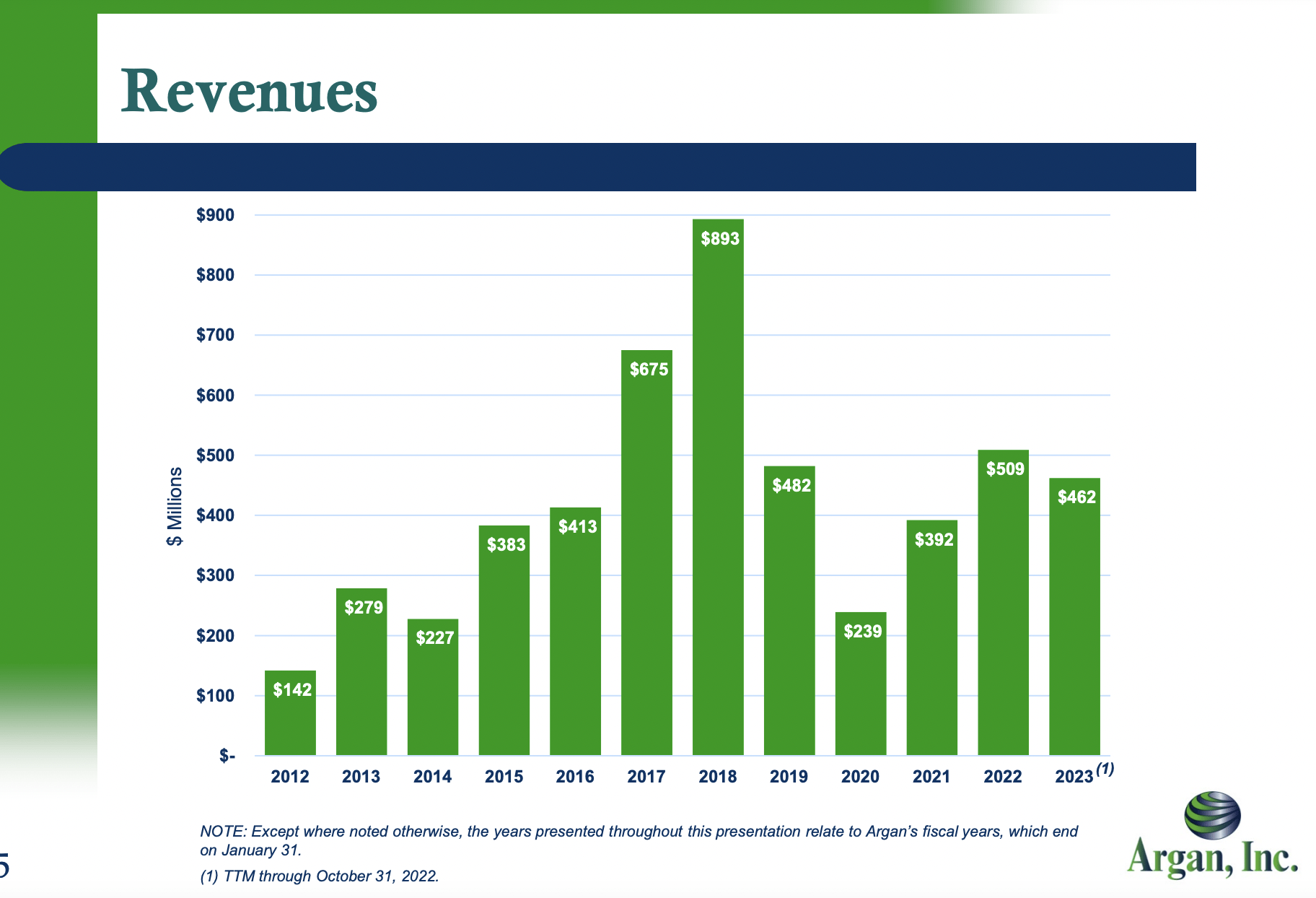

Argan’s revenues have heavily fluctuated over the past 5 years. In 2018, their revenues peaked at 892 million then drastically declined to 239 million during the depths of covid in 2020. Afterwards, their revenues rebounded to 509.4 million in 2022 and are projected to have a slight decline of 10% in FY 2023 to 458 million. Then, their average gross margins over the past 5 years have been approximately 15.4%, which may appear low at first glance but it is typical of the construction industry and virtually the same as their peer companies such as Expro Group (XPRO) and Granite Construction (GVA). Furthermore, they maintain steady operating margins of 8.4% in the TTM (38.8 million in operating income). Overall, although Argan’s revenues have heavily fluctuated over the past 5 years thus affecting other components of their income statement, they have normalized their operations recently and maintain in-line margins relative to their industry while positioning themselves for future growth.

Argan 10 year Revenues (Argan Investor Presentation)

Balance Sheet:

Argan’s balance sheet is phenomenal as it represents their strong fiscal state and ability to return capital to shareholders. The highlight of their balance sheet is that they have over $286 .6 million in cash & cash equivalents which accounts for 58% of their current market cap. Due to this massive cash position, the management team is following up on one of the primary goals laid out in their proxy statement which is to better allocate capital because they are observing a lack of acquisition opportunities and announced a $125 million share buyback program which would take approximately 25% of their total shares outstanding out of circulation. Not only have they authorized a tremendous share repurchase program recently, but over the past 5 years they have also reduced their shares outstanding from 15.6 million to 13.6 million which represents a 13% decrease. I am a huge proponent of share buyback programs when the stock of a company looks cheap, which Argan does. Furthermore, in this instance, by performing such large share repurchases it can significantly increase the ownership that shareholders possess which will also be paired with rapid bottom line growth and multiple expansion creating an optimal combination to produce large returns. Then, regarding other components of their balance sheet, Argan has a book value of $20 per share and notably has $0 long term debt. Their massive cash position paired with virtually zero debt ensures that there is a minimal chance of bankruptcy if the overlying macroeconomic environment were to deteriorate or their business faced other monumental challenges.

Cash flow Statement:

Lastly, their cash flow statement is difficult to understand from a surface level perspective and requires in-depth analysis to properly understand. The notable aspect of their cash flow statement is that their cash from operations was (86.9) million in the TTM while their net income was 21.7 million. Moreover, in 2018 and 2019 a similar trend followed where they had positive net income and free cash flow, and in 2020 they had a net income loss and positive free cash flow. Typically, net income and free cash flow can be different from each other, but differences this extreme are not common. The root of such fluctuations can be traced back to the contract assets and liabilities on their balance sheet. In their latest quarter, it was reported that contract liabilities decreased by 78 million while contract assets increased by 10 million. Both of these changes impaired the cash flows of the company which resulted in the heavy contrast between FCF and net income figures. The negative cash flows of the company does not jeopardize the investment thesis. Contract liabilities are simply a business obligation to transfer a good or service to their customer of which they’ve received payment for, essentially, it’s very similar to unearned revenue but possess a different name due to the role of contracts. Argan’s contract liabilities decreased from $127 million to $49 million, which reflects them completing projects they’ve already been paid for and not receiving many new contracts. Fortunately, Argan has a large project backlog that can help to offset these negative changes and position themselves for better cash flow in the future. Lastly, although they do have negative cash flow while paying a $13.5 million dividend and executing their share buyback program, the large cash position as previously discussed can secure these actions that require cash until cash flows return to a positive state.

Project Backlog:

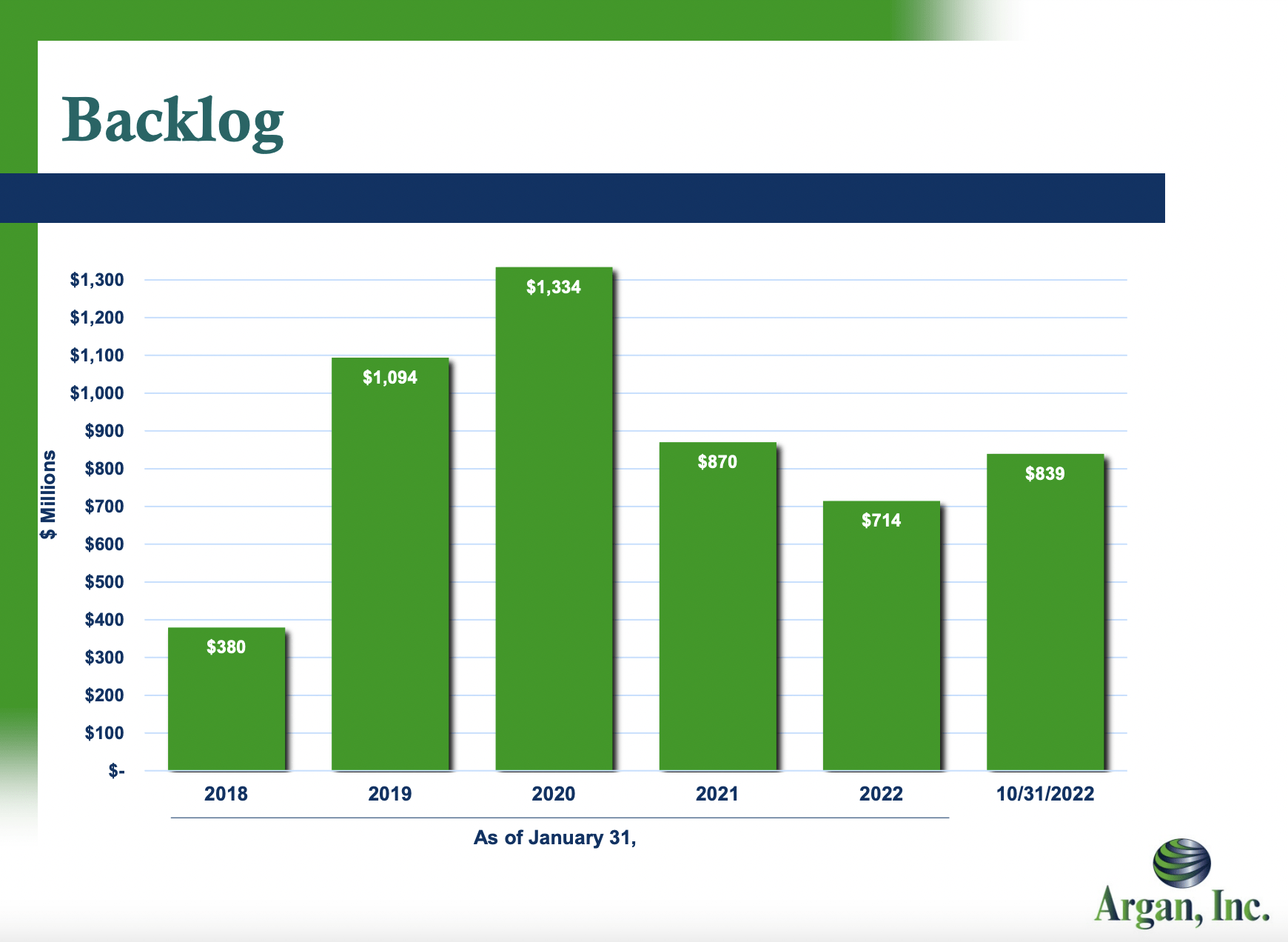

Within the construction industry, it’s crucial to a business’s project backlog in order to understand future revenue prospects and the degree of demand for their services at a particular point in time. Argan currently has a backlog of $800 million, comparable to $700 million in the prior year. A large majority of their backlog is composed of a few projects that are projected to be completed in fiscal 2023 and 2024 yet one of their newest and largest contracts to build the Trumbull Energy Center, a 950 MW natural gas-fired power plant in Ohio is projected to be completed in calendar year 2026, one of the furthest dates out. Overall, they have a large project backlog that reflects a continuous and growing demand for their services, primarily in the renewable energy sector.

Argan Historical Backlog (Argan Investor Presentation)

Growth:

The growth prospects of Argan are integral to the investment thesis and account for a large portion of where the upside for this business stems from. First, Argan maintains a phenomenal ROIC of 28% in their latest quarter and have maintained an average of 28% over the past 5 years excluding 2020 which was an anomaly due to covid. Their high rates of ROIC not only display how they invest their capital very well thus better stimulating growth, but consistently high ROIC numbers also warrant higher multiples thus contributing to the portion of the investment thesis regarding multiple expansion. Next, regarding future estimates for their top and bottom line, they are projected to grow substantially. For 2024, Argan is projected to grow their revenues over 27% YoY and then sustain a 20%+ growth rate through 2025. Moreover, these top line growth numbers will be exacerbated by their share buybacks as earnings will be growing among a smaller number of shares, thereby creating an optimal situation for investors. Overall, Argan is projected to rapidly grow over the next few years and their rapid top line growth combined with their share buybacks creates potential for substantial returns.

Argan Revenue Growth Estimates (Seeking Alpha)

Valuation:

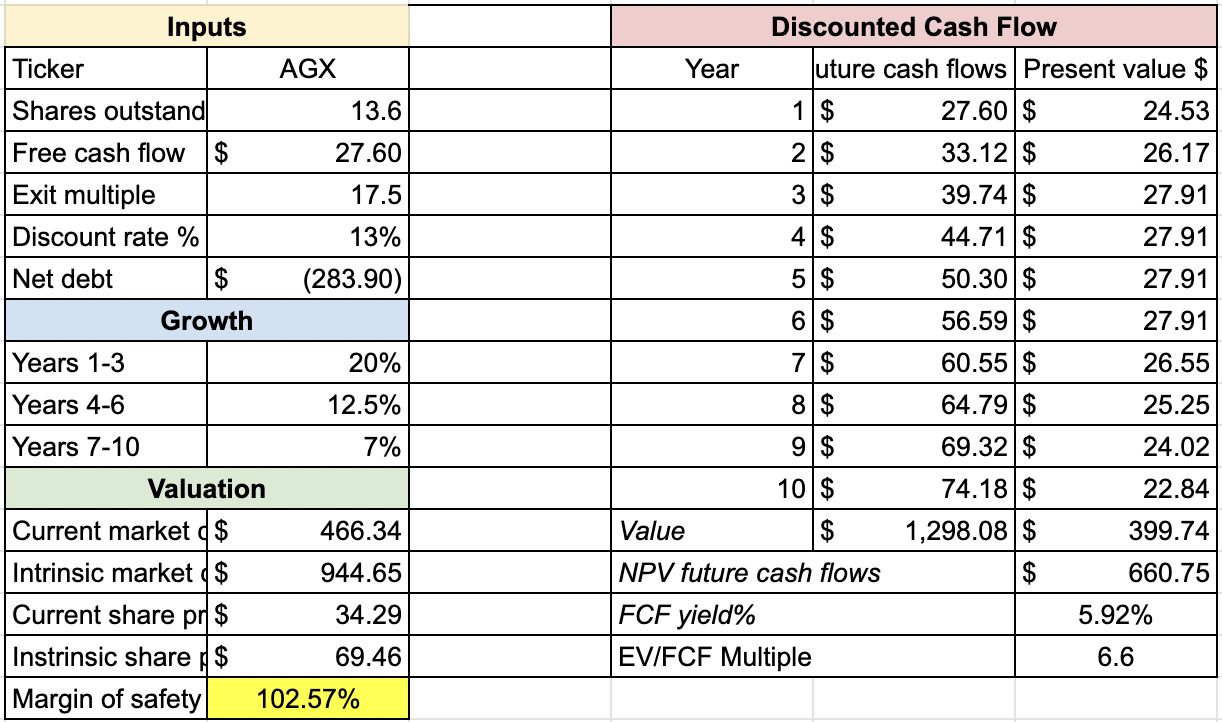

To value Argan I will be utilizing a simplified DCF model. For their profitability, I will be using FY 2023 EPS estimates of $2.03 which translates to $27.6 million in net income. I am using net income as a measure of their profitability instead of free cash flow due to the large fluctuations in contract assets and liabilities which impaired their cash flows to a larger extent than it typically has Furthermore, due to the large growth prospects of the business and high ROIC I believe Argan warrants a higher earnings multiple of 17.5 relative to the market average of 15. Then, I accounted for their excess capital yet did not address their share buybacks as the excess cash would decrease at a proportional rate to the shares outstanding decreasing because they are utilizing the cash already accounted for on their balance sheet to repurchase the shares. I then assumed a 20% growth rate for the next 3 years where it would drop off to 12.5% and 7% in the subsequent years. These growth numbers were reached as I utilized conservative analyst estimates for the next 3 years and assumed they could continue to grow their business, although at a slower rate due to their work in the renewable energy sector. Lastly, I am using a 13% discount rate as I want to produce a return that is going to beat the market and provides an additional margin of safety if my projections are incorrect.

Argan DCF model (Seeking Alpha Financials: Hossin Rasoli)

As we can see here, Argan appears substantially undervalued as they are trading at under have of their intrinsic value with conservative assumptions in order to receive market-beating returns.

Risk Factors:

Although Argan does appear significantly undervalued, there is one significant risk factor present that could heavily alter the demand for their services and jeopardize the investment thesis.

Macroeconomic Environment:

Argan’s business is heavily reliant on interest rates. In order for other entities to purchase their services and begin construction on large factories, they typically finance the costs through loans. As a result of the federal reserve’s recent interest rate hikes, the rates on loans have skyrocketed thereby disincentivizing businesses/government from utilizing their services due to how much more expensive it is. Furthermore, the high interest rates in today’s environment are propelling the United States into a recession, of which Argan conducts the large majority of their operations. In a recessionary environment, businesses typically are looking to reduce their capital expenditures and cut costs which would also negatively impact Argan. Overall, the risks outlined here are valid concerns yet Argan is projected to easily overcome these challenges and they are simply short-term headwinds that should not jeopardize the long-term operations of the business.

Final Thoughts:

Overall, Argan appears substantially undervalued with the potential to provide significant returns in the next 5-10 years. Their wholly owned subsidiaries that specialize in construction and engineering in the rapidly growing renewable energy space provide potential for rapid top line growth. Moreover, Argan returns tremendous amounts of capital back to their shareholders through their dividend and share buybacks thus bolstering shareholder value. Lastly, there are minimal long-term risk that can jeopardize the operations of Argan and the investment thesis as a whole.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!