Applied Materials Earnings: Not Perfect, But Far From Bad (NASDAQ:AMAT)

HQuality Video

Investment Thesis

Applied Materials (NASDAQ:AMAT) puts out a reassuring guide for fiscal Q3 2023. Given that investors had been charging hard into the semiconductor space in the past few several days, it’s fair to conclude that investors’ expectations were extremely high.

And while fiscal Q3 guidance didn’t blow investors away, the fact remains that the midpoint of its EPS guidance is certainly higher than analysts had expected.

While I believe that Applied Materials’ prospects for fiscal 2023 have plenty of potential to positively impress investors, there’s no doubt that Applied has its work cut out, as analysts’ expectations for the later parts of this year are indisputably negative.

Before we go further, keep in mind that Applied just reported its fiscal Q2 2023 results, meaning that its calendar year is misaligned.

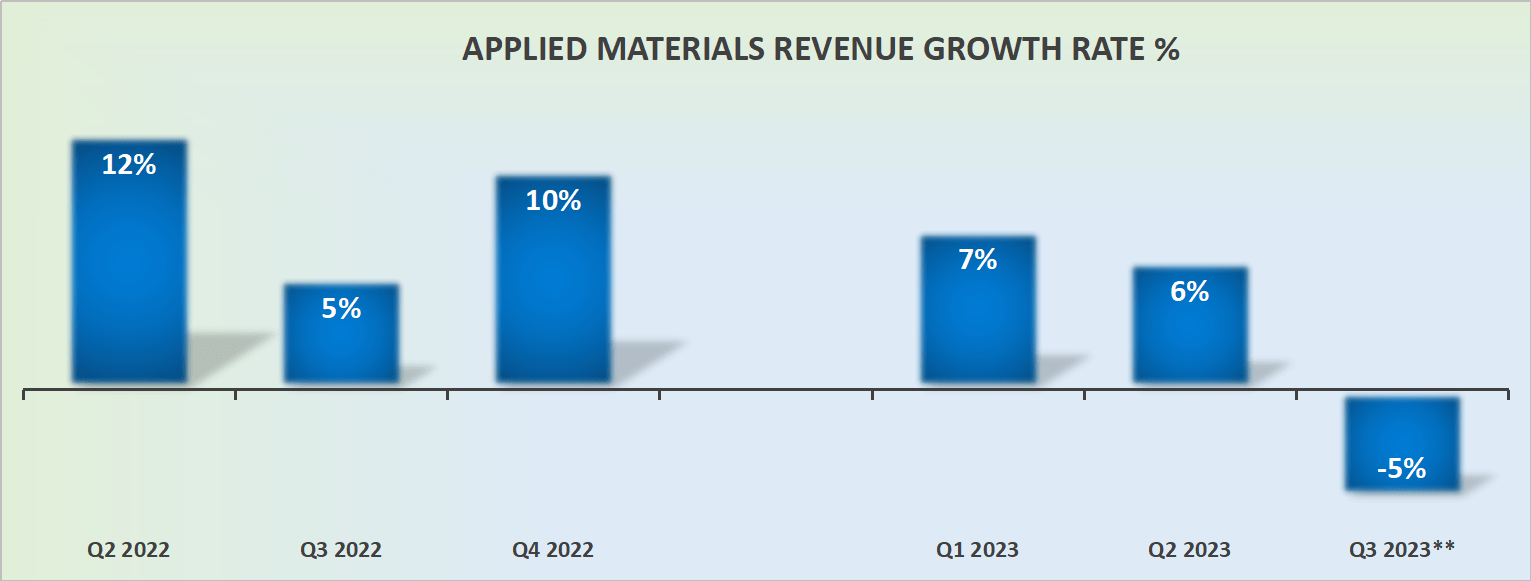

Revenue Growth Rates in H2 2023 Will Need to Improve

AMAT Q2 2023

Applied’s guidance for fiscal Q3 points to negative 5% y/y revenue growth rates. This was a slight improvement relative to what analysts had expected, but nothing truly remarkable.

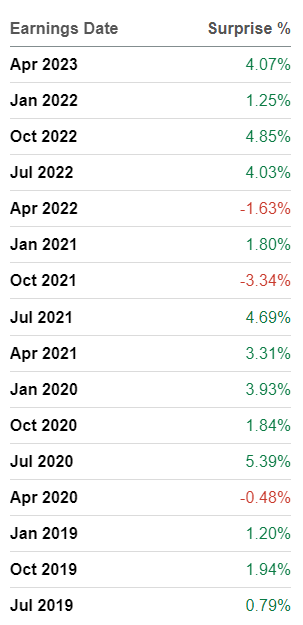

That said, note that Applied Materials typically beats revenue consensus estimates.

SA Premium

As you can see above, although there have been a few quarterly misses in the past 12 quarters, by and large, Applied Materials positively impresses against analysts’ consensus estimates.

Nevertheless, the big issue for investors is that they are hoping to see evidence that, in the back end of 2023 and early 2024, Applied’s revenue growth rates will be better than analysts presently predict (see below).

SA Premium

As it stands right now, analysts are expecting around negative mid-teens revenue growth rates for fiscal Q4 2023 and into fiscal H1 2024. Accordingly, given investors’ high expectations, either analysts are wrong on Applied Materials’ revenue growth trajectory, or the market is wrong.

Along these lines, consider what Applied Materials’ management said on the call:

Increasing complexity mans that wafer fab equipment can grow at a higher rate than semiconductor revenues and then, within equipment spending, major technology inflections are increasingly enabled by materials engineering, expanding the available market for Applied Materials.

Furthermore, Applied’s IoT, communications, automotive, power and sensors (“ICAPS”) continue to be strong, which is offsetting the weakness in Applied’s memory business.

In essence, this is the long-term vision for Applied Materials, how semiconductors are the foundation for a digital economy, and that the confluence of different technologies is at the point of inflection.

Profitability Profile Ebbs Slightly

Within its equipment business, foundry and logic performed strongly, while Applied Material’s DRAM and NAND flash memory business units left a lot to be desired.

Consequently, given the overall weakness in the memory market, I’m not entirely sure this was all that surprising for investors.

AMAT Q2 2023

Altogether, this led to Applied’s semiconductor systems’ non-GAAP operating margin to compress by 150 basis y/y from 37.1% to 35.1%.

That being said as we now look ahead to fiscal Q3 2023 EPS guidance, it points to around $1.75, which is at least 5% higher than analysts had as Applied headed into the earnings print.

The Bottom Line

I believe that it’s apt to finish with this quote from the earnings call:

We believe our free cash flow can continue to grow and support increasing the dividend at an accelerated rate over the next several years which would double our previous dividend per share. As our services business grows along with our installed base of equipment, it alone produces more than enough operating profit to pay the company’s dividend.

In conclusion, sometimes investors get too caught up thinking about the next quarter or two, but there’s no doubt that Applied Materials continues printing free cash flows and is eager to increase its capital returns to shareholders.