AMN Healthcare: GARP Potential, Shares Bounce Off Support Ahead Of Earnings (NYSE:AMN)

FatCamera

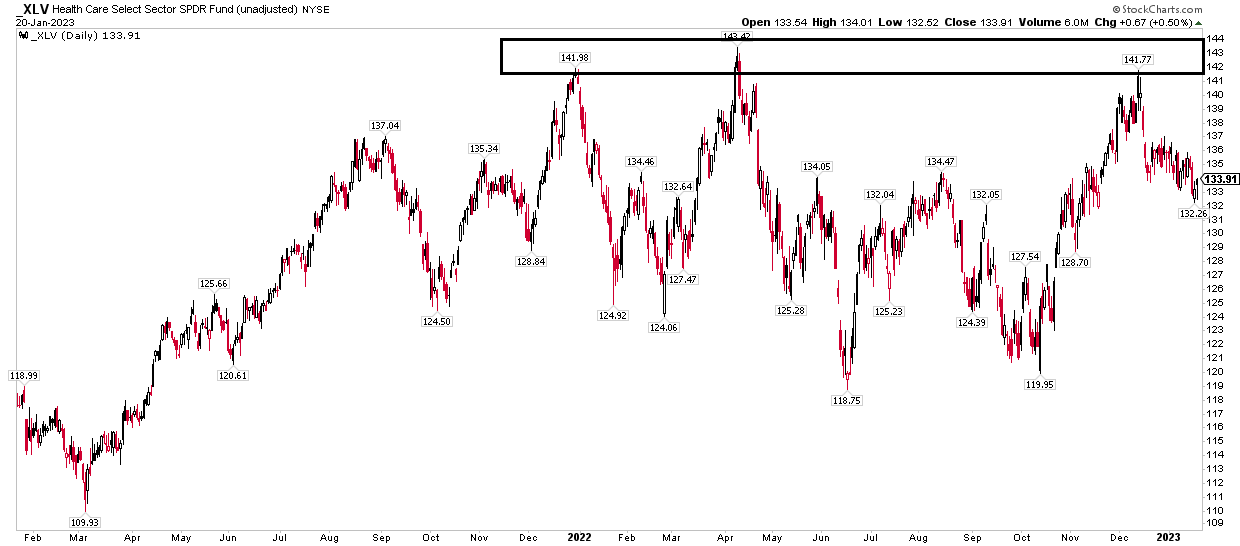

Healthcare sector stocks have been a safe place to hide out during bouts of market turmoil in the last 12 months. Many individual names within the broad space feature consolidation price patterns. It is a wait-and-see approach in many instances as defensive equities have underperformed so far in 2023 after last year’s alpha.

One example is AMN Healthcare (NYSE:AMN). But this staffing firm offers some earnings growth upside as labor challenges remain in place for healthcare firms. Let’s check out the fundamentals and technicals on AMN.

Healthcare Sector: Flat-Lining

Stockcharts.com

According to Bank of America Global Research, AMN Healthcare Services provides staffing services to healthcare facilities across the US. In addition to recruiting and staffing healthcare professionals, AMN offers consulting, scheduling, and other workforce management services.

The Texas-based $4.2 billion market cap Healthcare Providers & Services industry company within the Healthcare sector trades at a low 9.6 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal.

Back in November, AMN beat earnings estimates while raising its profit outlook for Q4 and 2023 as the jobs market within the healthcare space remains tight. We’ll know more about the fourth quarter in just a few weeks. The firm beat revenue forecasts across all its segments with improved margins, to boot. While profits might decline this year, there’s a focus on return on capital by its management team that could be beneficial for shareholders.

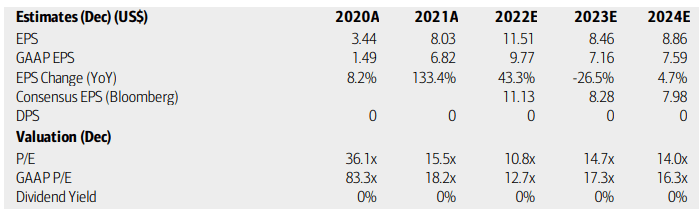

On valuation, analysts at BofA see earnings having risen sharply in 2022, but then dropping back by more than 26% to levels still above what was earned in 2021. By 2024, though, EPS growth normalized in the mid-single digits. Don’t expect dividends any time soon with this growing healthcare staffing firm, but both AMN’s operating and GAAP earnings multiples should stabilize in the mid-teens.

Ranked 5 out of 57 in its industry, per Seeking Alpha, shares sport a forward operating PEG ratio of just 0.57 – below the sector median of 1.98 and the stock’s 5-year average of 1.31. Overall, I like the valuation case and where AMN sits in a high-demand industry.

AMN Healthcare: Earnings, Valuation, Dividend Forecasts

BofA Global Research

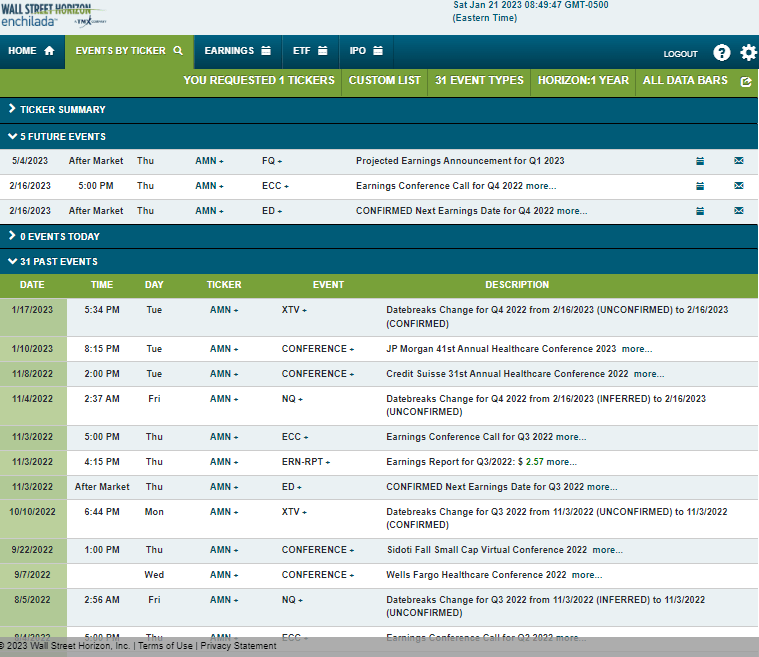

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q4 2022 earnings date of Thursday, February 16 AMC with a conference call immediately after the numbers cross the wires. You can listen live here.

Corporate Event Calendar

Wall Street Horizon

The Technical Take

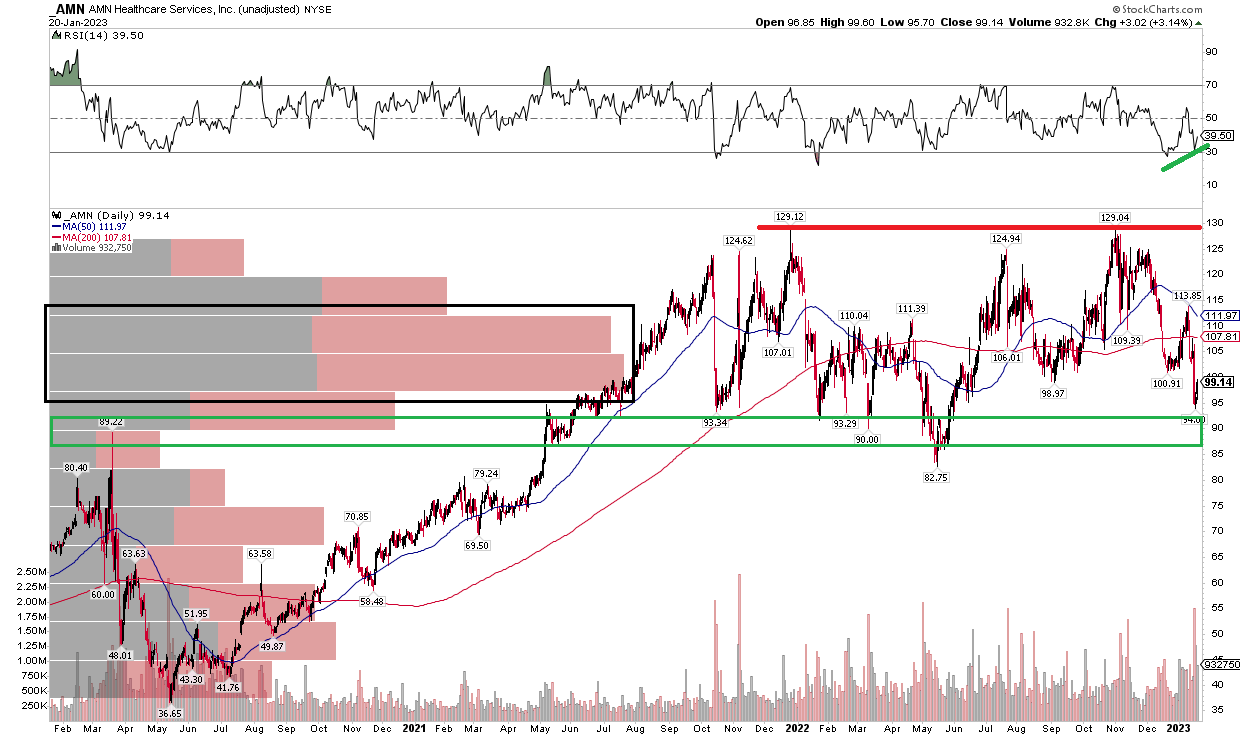

While AMN appears to be a GARP candidate for your portfolio, the technical situation is less exciting. Notice in the chart below that shares have simply been in consolidation mode since the middle of 2021. With obvious resistance near $129—a double top—the stock finds buyers in a broad range from the mid-$80s to the mid-$90s.

It’s currently working off another successful test of the lower end of that zone. With a flat 200-day moving average and significant supply of shares as measured by the volume-by-price indicator on the left, the onus is on the bulls to prove themselves. What is in their favor, however, is positive RSI divergence on its recent dip in price. So, I see shares eventually retesting the $125 to $129 high-end of the range before long.

A move above $130 would trigger a measured move price objective to near $175. This is one to keep on your idea list in 2023.

AMN: Shares Bounce Off Lower-End Of A Trading Range, Bullish Divergence

Stockcharts.com

The Bottom Line

AMN features a good valuation case considering its growth prospects. The technical chart, while exhibiting relative strength in the last year (and not being in a downtrend like the broad market), is stuck in a range. A near-term tactical buy is warranted, while a move above $130 would be long-term bullish. A breakdown below $80 would be bearish.