American Public Education Stock: Undervalued, Losses May Widen (APEI)

LaylaBird/E+ via Getty Images

In November, I wrote an article on the deteriorating conditions of American Public Education, Inc. (NASDAQ:APEI); since then, APEI stock price has lost over 67% of its value and has been trading for about $4.2 per share.

In the last two years, the company has come up with the acquisition of Rasmussen university and GSUSA; as a result, the companies’ expenses to market these universities have increased.

Although the core business is intact, the acquired businesses are bringing a higher cost of operation which has been putting significant pressure on the operating margins.

APEI is suffering from expensive decisions of the senior management and inadequate governance of Rasmussen university; I expect in the upcoming year, the losses might widen due to higher spending on promotions and lower enrollments.

Backdrops

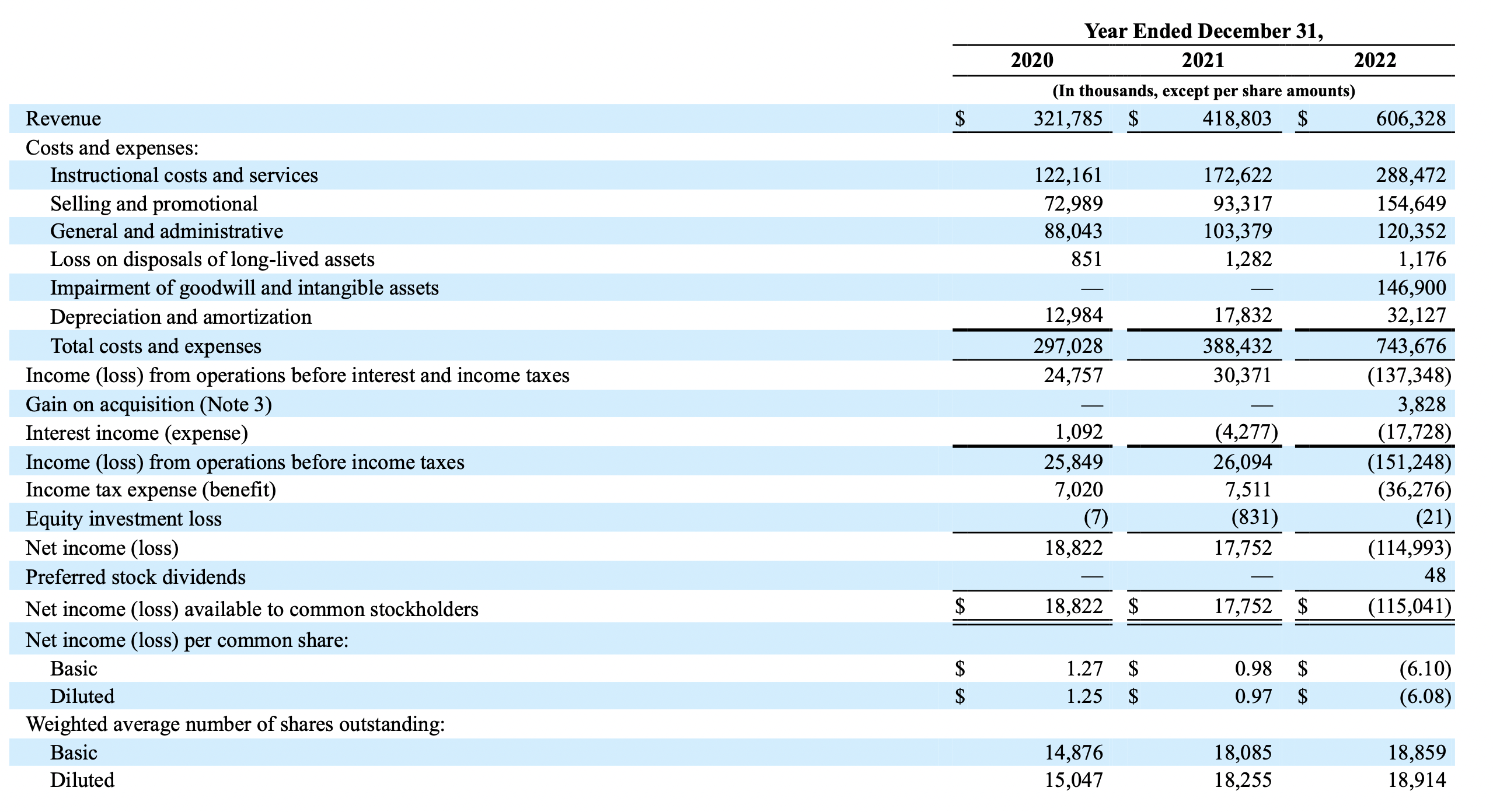

For the year ended December 31, 2022, costs and expenses were $743.7 million, an increase of $355.3 million, or 91.5%, compared to $388.4 million in 2021. The increase in costs and expenses as compared to the prior year period was primarily due to the inclusion of 12 months of RU Segment expenses in 2022 as compared to four months in 2021, the inclusion of GSUSA in Corporate and other expenses in 2022, and a non-cash impairment charge of $146.9 million to reduce the carrying value of RU Segment goodwill and intangible assets, and to reflect the corresponding tax impact for the year ended December 31, 2022. For the year ended December 31, 2022, the increase in RU Segment and GSUSA costs and expenses were $184.9 million and $22.8 million, respectively, excluding the goodwill and intangible assets impairment charge in the RU Segment.

Annual report 2022

During the year 2022, the company’s expenses have skyrocketed with an increase of a whopping 91%, resulting from higher expenditures on RU and GSUSA business; these businesses are putting significant pressure on the company’s operating results.

For the year 2023, management expects nursing enrollments to decline for Rasmussen university, which is expected to affect overall net margins. The primary reason behind such a drop in performance is the unexpected departure of key management; I believe that the company has been suffering from improper governance and expensive capital allocation decisions.

We have completed the transition of RU marketing in-house to our centralized marketing team and plan to transition all of the information technology services currently outsourced to Collegis back to our operations or to one or more other third-party vendors.

Annual report 2022

Although the management is extensively working on the transition of RU, the result doesn’t seem attractive; I expect in the next two years, RU might bring losses to the company due to improper governance and higher operating expenses.

Financial performance

income statement (annual report )

In the year 2022, the revenue has increased to $606 million, led by higher enrollment and acquisitions; as the Rasmussen business is consuming a significant amount of money, the operating margins have turned negative, which has resulted in huge losses.

Also, due to the higher price paid to purchase Rasmussen and HCN, the company has incurred goodwill impairment charges of over $217 million and $38 million, respectively; which might show that the capital allocation decision of the management is not effective, and the decision has led to huge losses for shareholders.

However, the positive thing is debt has gone down from $151 million in FY 2021 to $93 million by now. Also, the company holds $186 million in current assets and over $349 million in shareholders’ equity. Such a financial position provides significant stability to the business model.

Conclusion

The core business has been intact and can produce consistent returns, as seen in the historical levels. As per the management, APUS will remain a steady cash generator for the company.

Currently, the company is trading for about $76 million, whereas it has over $186 million in current assets and a core business that produces consistent returns. It seems that the APEI is trading for 0.4 times its current assets, which is a substantial bargain. But there are various concerns about the operating results, which can bring huge losses to the company.

The main reason behind a substantial drop in net profits is the recently acquired companies producing huge losses; therefore, the company could turn around from losses and become profitable again by restructuring Rasmussen’s business or disposing of the businesses.

Therefore, investors must consider that these losses might hurt the financial position of the business significantly and can bring a lot of trouble. The loss may widen in the future due to the huge amount of cash the acquired entity consumes. I assign a Hold rating to APEI stock, as due to significantly dropped prices, the stock has become substantially undervalued, but losses are expected to remain in the upcoming years.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.