Altria: Not This Again (NYSE:MO)

Mario Tama

An old mentor of mine used to say “I’ve told you a million times not to exaggerate things.” I feel like I’ve already rebutted a million articles about Altria Group, Inc.’s (NYSE:MO) dividend safety. Hence, if my readers feel like they’ve heard (or read) this from me before, they are not mistaken. But this article by SA contributor DT Analysis is a bit unique because the author correctly points out the declining volume of cigarette sales is concerning. The author also states the company cannot keep increasing prices forever to offset the volume decline. Fair enough again. But where I disagree is the conclusion that the dividend is at risk and MO stock is a sell.

I strongly believe that Altria’s dividend is safe and the stock is a buy with its yield approaching 10-year highs. Before that, let’s address the elephant in the room. Is Altria’s declining sales volume an immediate concern? I don’t believe so. I am going to use three charts to prove this point. All three charts point to data from continental United States and are not Altria-specific, although Altria still holds close to 50% of the retail share.

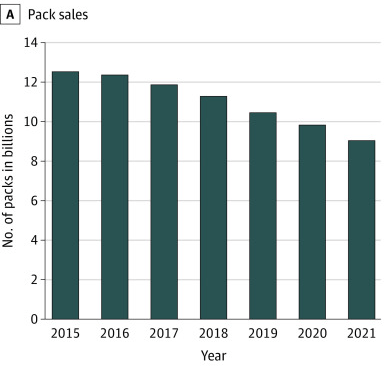

- Chart A below shows the undeniable decline in the total number of packs sold. From 12 Billion in 2015 to $9 Billion in 2021, the decline in number of pack sold is about 25%, which definitely sounds concerning.

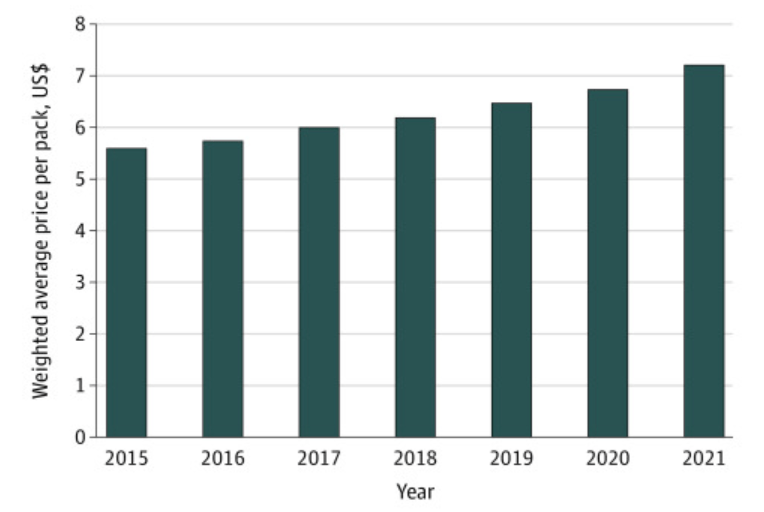

- Chart B shows the increase in price per pack in the same time period. From $5.57 in 2015 to $7.22 in 2021, the price increase was a cumulative 29%.

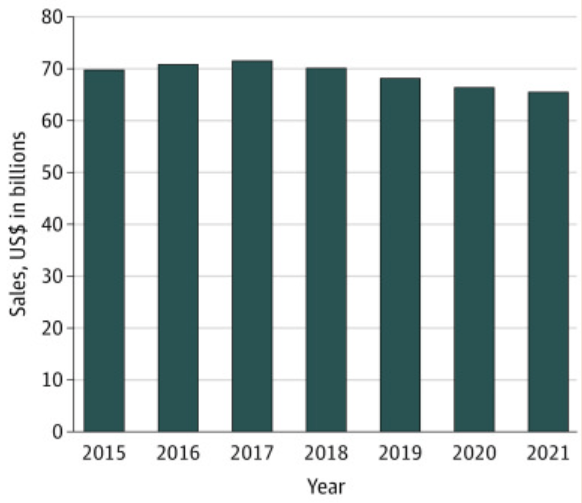

- As a result, Chart C alleviates the concerns raised in Chart A, as the total sales in USD has declined by a cumulative 6% over a full 7 year period.

Pack Sales (www.ncbi.nlm.nih.gov) Price per pack (ncbi.nlm.nih.gov/) Sales in USD (www.ncbi.nlm.nih.gov)

What do these three charts show us?

Nothing staggeringly new, but the following points that need to be reiterated to calm the nerves of Altria investors:

- On an annual basis, the decline in cigarette sales (in USD) is less than 1% per year between 2015 and 2021. At that rate, Altria investors can rest easy for many years, if not multiple decades, that the company can sustain and improve its returns to shareholders (see the “What do these three charts not show us?” section below).

- All three charts shown above have a gradual increase or decrease over the 7-year period. There is nothing to indicate this “old model” is breaking down. This is akin to a runner climbing or descending an incline. When you stare ahead or look back at it, you wonder “Geez, how is/was that possible?” but while doing it, you only look at the next incremental step up or down. In other words, YoY, neither Altria nor the consumers seem to be feeling much of a pinch at the end of the day.

- Lastly, take a look at the list of the fastest-declining industries in the U.S. by revenue growth in 2023 and see where tobacco ranks in the top 10. Hint: you won’t find it in the list. Why? Because it has never seen the dizzying heights to worry about falling off the face of the earth in a year or two or even 20 years from now. I’d be much more worried about some of my high tech stocks (I do hold some) losing 50% of their revenue for three consecutive years (happens many times) and gaining 100% the next three years (happens rarely) than worrying about a gradual <1% YoY decline with Altria. If you are quick with numbers, do this math yourself. Let’s say you are a high tech company and start at a revenue of $100. Go through three YoY declines of 50%. Then go through three YoY increase of 100%. See where you end up. Hint: you did not make much progress but were huffing and puffing to end up where you started.

What do these three charts not show us?

Plenty. Outside of price increases, Altria has a few salient characteristics that sets it apart.

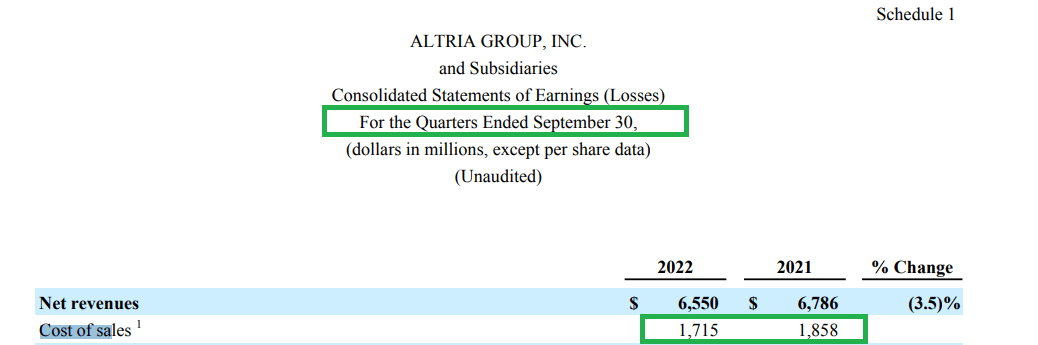

- Price increases are just one (albeit big) part of the company’s ability to offset decline in volume. The other unspoken part is their ability to keep costs low and to keep seeking improvement in this area. As a staggering example, on a YoY basis, the third quarter in 2022 showed a $143 Million decline in Cost of Sales.

Altria Cost of Sales (Altria.Com)

- Altria’s stated dividend policy of sending 80% of its earnings per share (“EPS”) to shareholders is so sacred that it proudly and confidently lists it on its website. But actions speak louder than words, right. The current annual dividend per share is $3.76, which represents 78% of the expected forward EPS of $4.81. The payout ratio based on Free Cash Flow (“FCF”) is also close to 80% as covered in this article.

- The management is almost never in the news. This is great news for investors because they are likely busy doing what the shareholders expect them to do: not to over indulge and do what you do best. These things have a ripple effect as cost stays down, prices go up strategically to offset volume decline, and shareholders get 53 years (and counting) years of pay increase. If that is not a hallmark of a trustworthy management, I don’t know what is.

- Altria’s dividend is always spoken about, but the buyback program is not to be forgotten. As recently as the third quarter of FY 2022, the company bought back 8.5 million shares. This once again shows their alignment with shareholder returns.

Conclusion

I continue reinvesting my Altria Group, Inc. dividends as explained in this article and find it baffling that the stock got a “Sell” rating when it nearly yields the highest it has in the last ten years (barring COVID lows when the yield was 10.40%). Not to forget the fact that the dividend is well-covered as explained above.

At the end of the day, investment returns are guided by the difference between expectations and reality. The lower the expectations, the better for Altria investors. Just ask those who held technology stocks in 2022 (myself included). Altria Group, Inc. investors should welcome the doubters and critics because, while the size of the Altria pie may be shrinking, the ones leaving the scene increase the share of those who stay in the long run. So, you are welcome to leave Altria, but please do not leave this article without posting a comment.