Ally Financial Is The Baby Being Thrown Out With The Bathwater (NYSE:ALLY)

courtneyk

Ally Financial (NYSE:ALLY) is a deeply undervalued and misunderstood bank that is built for the current era. I find myself regularly amazed at how often the company’s demise has been predicted by doomsday internet financial pundits. In this article, I’m going to discuss the current opportunity in ALLY stock, and address some of the false narratives surrounding the company. The market is currently in a panic and a lot of subscriptions are sold on the basis of promoting extreme fear. By a careful analysis of the facts and a strong stomach, fortunes can be made on the recovery of ALLY and other unfairly tarnished financial stocks.

ALLY’s 4th Quarter Investor Presentation

Over my years covering ALLY, I’ve seen the company’s death predicted from a variety of different causes. First it was supposed to be auto defaults. Then on multiple occasions, it has been projected declines in used auto prices. Now it is some ridiculous assumption that the company would face a bank run and have to liquidate everything, resulting in realized losses on its mortgage portfolio from mortgages originated at lower interest rates. ALLY is not Silicon Valley or Signature Bank. The company is poised to capitalize on the disruption as weaker competitors pull out of the auto finance industry.

ALLY originated $46B of consumer auto loans sourced from 23k active dealers in 2022, at an estimated yield of 8.24%, which was up 114 bps YoY. The company experienced 97bps full-year net charge-offs, and 166 bps of Q4 net charge-offs as credit normalization progressed throughout the year. ALLY also produced $1.1B of insurance written premiums sourced from 4.6K dealers. The bank has $137.7B of retail deposits from 2.7M retail depositors, all digitally acquired. In 2022, ALLY originated $3.3B of mortgages and has $19.4B in its held-for-investment portfolio, which is the primary cause of AOCI losses due to higher rates. ALLY Invest has $12.8B of net customer assets and 518K active accounts. ALLY Lending produced $2.1B gross originations and has 460K active borrowers from 3.4K active merchants. ALLY Credit Card is the newest business, finishing Q4 with $1.6B in credit card balances from 1M active cardholders. Lastly, the Corporate Finance portfolio stood at $10.1B in the held-for-investment portfolio, of which 100% is floating rate. The vast majority off ALLY’s loan book is secured, which tends to hold up far better in a recession than unsecured. ALLY is not a big player in the subprime market and higher yields are being passed on to consumers and corporations.

Credit quality has been extremely good for ALLY leading to the company over-earning, and while of course it will normalize, ALLY is likely to remain robustly profitable with projected trough 2023 earnings per share of $4.00. Used car prices rallied tremendously during the Covid lockdowns, and while they finally started coming down in late 2022, used car prices have now stabilized again and actually are moving up. This is the exact opposite of what the panic prognosticators were predicting over the last year. ALLY’s actual risks from declining used auto prices have always been overblown since the company shrank its leasing business. I saw one supposed bank analyst predicting doom for ALLY because the securitization market has frozen up, but fortunately ALLY has been comfortable originating loans for its own balance sheet funded by deposits. This is much more durable business model than non-bank originators that are completely reliant on capital markets.

ALLY’s profit margins have been greatly enhanced from its transition to deposits, from unsecured lending, which was much more expensive. Roughly 80% of deposits are retail, which are less prone to fleeing rapidly, as we saw with the VC funds and portfolio companies with Silicon Valley Bank. Just as importantly, only about 10% of deposits are uninsured, which could likely be replaced by other forms of borrowing if needed. Another big difference with ALLY is that the bank is known for paying extremely competitive deposit rates already, so they are less exposed to the shift towards higher yields than other banks that have gotten away with paying very little on deposits. ALLY has a plethora of options for liquidity including the FHLB bank, the Discount window, potential securitizations, etc., if needed. All of this adds up to ALLY being at very low risk for a bank run. ALLY offers mortgages to its customers and keeps them on the balance sheet. Higher rates have lowered the value of these mortgage causing temporary losses, but ultimately these mortgages are good credit quality, and should mature at par. ALLY will not have to liquidate them earlier, nor should banks be overly obsessed with mark to market accounting on held to maturity loans. If they were, access to credit which is the blood flow of a functional economy, would be dramatically constricted.

Another advantage ALLY has versus the regional banks that have been victimized by these bank runs is that their assets are much higher yielding, and many of them such as in Commercial Finance and Commercial Auto, adjust higher as rates have been increased. While retail auto loans are fixed rate, ALLY has been enhancing those rates rapidly and as other companies such as Capital One Financial (COF) and Santander (SAN) have backed away recently, ALLY has tremendous pricing power. These factors greatly mitigate the temporary net interest margin squeeze that ALLY’s rising deposit rates have caused. ALLY hasn’t had to change its funding business model as it has been growing based on competitive rates and great technology, so there wasn’t the expectation of paying incredibly low deposit rates forever, that seems to have been the case for some of the other regional banks.

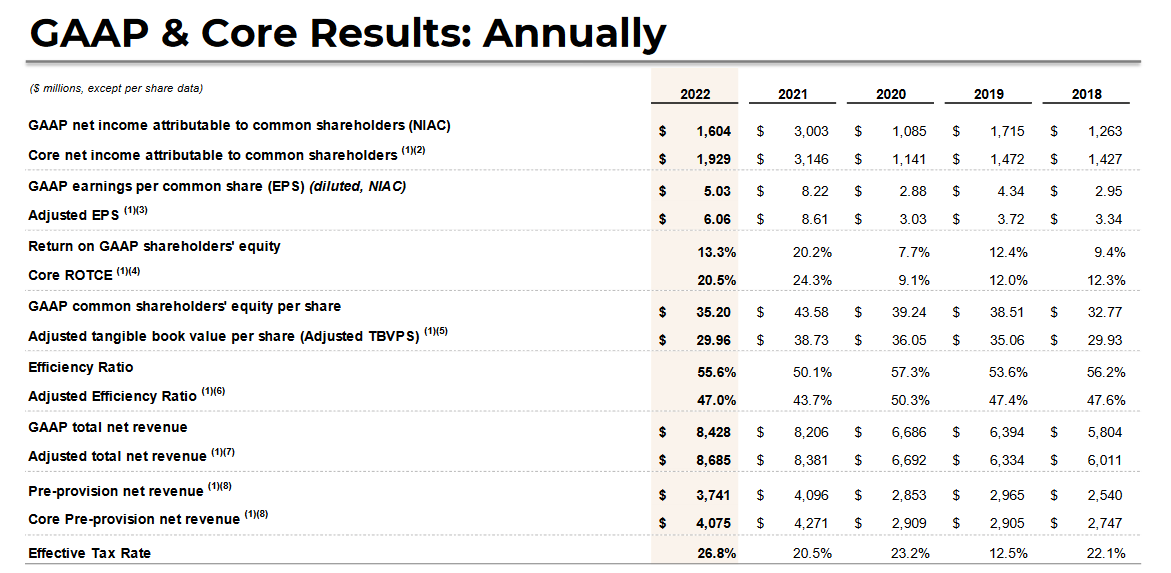

At a recent price of $24.22, ALLY trades at just 81% of its adjusted tangible book value per share of $29.96, which will likely increase quite a bit in Q1 due to the steep decline in bond yields. ALLY’s normalized ROTCE is in the mid-teens. This is a very profitable enterprise being treated as though it is likely to go out of business, when the company seems to be very well-suited for the current environment. The stock is trading for about 4x TTM earnings of $6.06 per share, and 6x trough 2023 earnings of $4.00 per share. The stock pays a quarterly dividend of $.30 per share, which equates to a whopping dividend yield of 4.95% at the current price. ALLY’s management indicated that it didn’t have plans to buy back stock earlier in the year, but I hope that they wise up and take advantage of this mammoth discount between price and value. I believe ALLY is worth $40-$45 per share conservatively in a normal environment, which is right around its tangible book value per share adjusted for AOCI losses.