Allianz Q4 Results: Significant Headwinds Resolved (OTCMKTS:ALIZF)

Marco_Bonfanti

2022 was a complicated year for Allianz (OTCPK:ALIZF, OTCPK:ALIZY) and was also emphasized by the company itself in the following slide.

Allianz 2022 Headwinds

Source: Allianz Q4 and FY results presentation

Here at the Lab, we well covered the German insurer, providing key company insight and confirming our long-standing buy rating.

- 17/02/2022 – we published the Allianz provision related to the AllianzGI U.S. Structured Alpha Funds;

- 11/05/2022 – we reported Allianz new provision in Q1 2022;

- 17/05/2022 – we analyzed Allianz’s U.S. resolution government investigations concerning Structured Alpha.

Allianz proved to be a resilient player and we are not surprised. Indeed, it is an insurance company with a proven track record dating back to 1890. Before commenting on the company’s Q4 results, we recommend that our readers check up on our previous article called a Long-Term Opportunity in which we emphasized 1) the company’s 10-year financial indicators (with a lower cost basis and an increase in its solvency requirements) 2) Allianz’s “attractive and predictable dividend“, 3) a compelling valuation, considering PIMCO Division, and the upside on reinvestment yield.

Mare Evidence Lab’s previous publication

Q4 and FY 2022 results

Allianz was back to profit compared to the previous year’s end quarter. In specific, the German company was supported by the Life and Health insurance strength, while the wealth management division reported lower revenues and fees.

With our record results for both revenue and operating profit in 2022, Allianz has consolidated its position as one of the world’s largest, most resilient, and trusted global financial institutions. – Oliver Bäte, Allianz’s CEO.

Looking at the key numbers, the total company’s revenues increased by 2.8% to €152.7 billion on a yearly basis, but in Q4, sales were down by 4.5%. EBIT profit reached €14.2 billion thanks to excellent performance in L/H and P&C business and strongly accelerated in the last quarter (up by 12.7%). Looking at the divisional level, the P&C business segment performed thanks to strong pricing power, higher volume, and lower expenses. These positive performances were partially offset by lower AuM and as a consequence lower fee generation in the Asset Management division. In detail, the lower assets under management were due to the Voya transaction and the debt/equity market turmoil. Top-line sales also decreased in the L/H division for a decrease in statutory premiums, especially in the German market, and a lower turnover of unit-linked products in the Italian geography. Net income attributable to shareholders reached €2 billion, reversing the loss of €292 million in 2021. Analysts were pricing in a net income of €2.03 billion. Regarding the aggregate level, profits reached €7.18 billion and were up by 1.1% versus the 2021 end.

Allianz financials in a Snap

Conclusion and Valuation

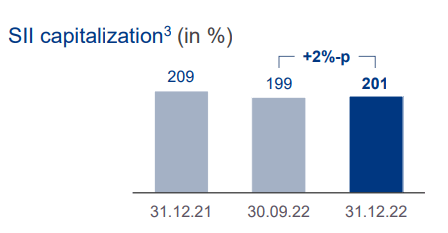

Despite the positive accounts just released, Allianz is currently losing 2.5% in stock price. Overall, fourth-quarter results proved to be quite solid; however, the consensus is already looking to 2023 operating profit pressure and further evidence suggests a limited upside on the P&C combined ratio target of 94% for 2024. This is why we are maintaining our buy rating target at €220 per share ($23.4 in ADR); however, the target is more skewed on a neutral valuation. Earnings per share also increased, rising to €16.35 from €15.96 in 2021 (+2.4%). These positive results allowed Allianz to propose a dividend distribution of €11.4 per share in 2022 with an increase of 5.6% compared to 2021 (which fully confirmed their shareholder remuneration strategy). This is also coupled with an ongoing buyback of €1 billion started in November last year. The solvency ratio reached 201% vs the 199% recorded in Q3 and was lower than the 209% achieved by last year’s end. As already mentioned, the 2023 guidance was not the greatest so we suggest our readers look at our latest publication called Assicurazioni Generali Is A Buy. Generali (OTCPK:ARZGF, OTCPK:ARZGY) with a lower P/E, a higher dividend yield, and a higher discount on net intrinsic value worth a consideration.

Allianz Solvency Ratio evolution

Allianz 2023 guidance

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.