Exelon: This Giant Electric Utility Is Worthy Of Investment Today (NASDAQ:EXC)

Artur Nichiporenko

Exelon Corporation (NASDAQ:EXC) is one of the largest regulated electric companies in the United States, boasting operations in five states. The company is obviously part of the utility sector, which has long been one of the favorite sectors for conservative income-focused investors. There are some good reasons for this, as utility companies tend to be among the best dividend stocks by virtue of their high yields and stable cash flows. Exelon is certainly no exception to this, and the company’s 3.25% dividend yield is among the highest in the utility sector. The company also boasts respectable growth potential and an attractive valuation, which sets it up well to be an excellent prospect for investment today.

About Exelon Corporation

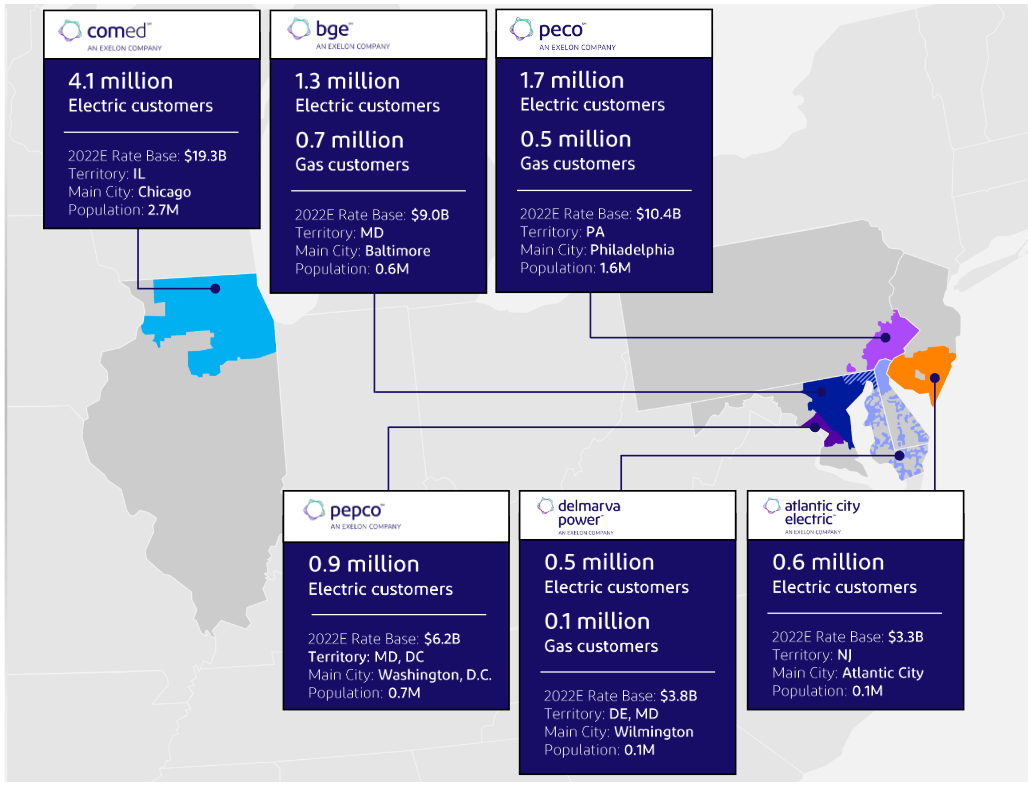

As stated in the introduction, Exelon Corporation is one of the largest regulated electric utilities in the United States. The company serves customers in five states, which are Illinois, Pennsylvania, Maryland, Delaware, and New Jersey:

Exelon Corporation

This service area includes both the Chicago and Philadelphia metropolitan areas, which are among the most populated areas of the United States. As such, Exelon serves 10.5 million customers despite not having as large of a service area as some other regions in terms of square mileage. As I have pointed out in various previous articles though, a utility’s size is somewhat irrelevant in terms of its characteristics. The most desirable of these characteristics is that the company enjoys relatively stable cash flows over time. We can see this by looking at Exelon’s trailing twelve-month operating cash flows in each of the past eleven quarters:

Seeking Alpha

As we can clearly see, with the exception of the period that included most of the pandemic period (the twelve-month period ending March 2021), Exelon’s operating cash flow is almost always around the same level. The reason for this is that electric service to a home is generally considered to be a necessity for our modern way of life. After all, I can pretty much guarantee that everyone seeing this has electric service in their homes and businesses. As such, most people will prioritize paying their electric bill over discretionary spending during times when money gets tight. This is exactly the characteristic that you want during tough economic times, like a recession. Nearly every economist is expecting a recession during 2023 and in fact, that is the goal of the Federal Reserve’s monetary tightening policy. As such, it may make sense to hold a company like Exelon in order to protect some of your assets in the event of a recession.

One thing that we do note above though is that Exelon’s operating cash flow did decline significantly during the twelve-month period that ended on March 31, 2021, although it did quickly recover. This was not exactly unexpected. As I discussed in a previous article, there were an enormous number of people that fell behind on their utility bills during the lockdowns and the worst of the pandemic. The total nationwide total of payments of arrears was $35 billion to $40 billion in March of 2021. This is something that likely created a drag on Exelon’s operating cash flows during that period. After all, Chicago and Philadelphia were both among the areas that had the strictest COVID-19 lockdown policies, and these cities both have a number of people whose finances cannot easily withstand a period of fewer hours at work. Thus, it is reasonable to assume that the company’s cash flows declined due to people falling behind on their electric bills. This is especially evident since the worst-affected quarters were the twelve-month periods that ended on March 31, 2021, and June 30, 2021, which would be around the time that people’s savings started running out in the latter half of 2020. The company’s operating cash flows did quickly recover from this, though, so we can see that the overall thesis of stability holds true.

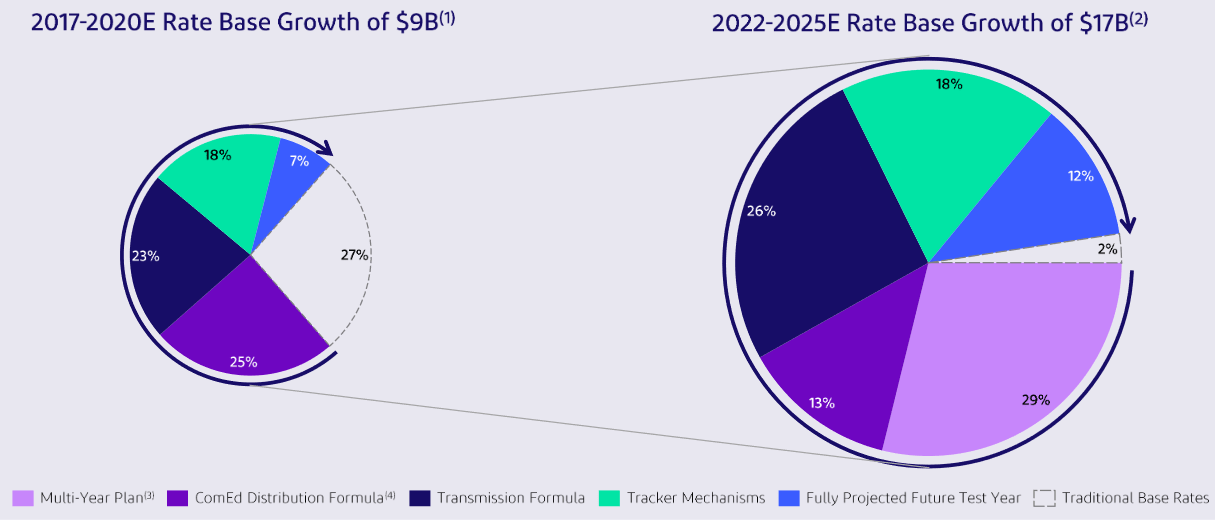

Naturally, as investors, we are not satisfied with mere stability. After all, we need to see growth from the companies that we are invested in. Fortunately, Exelon is well-positioned to deliver this growth. The primary way that the company will accomplish this is by growing its rate base. The rate base is the value of the company’s assets upon which regulators allow it to generate a specified return. As this rate of return is a percentage, any increase in its value allows the company to increase the price that it charges its customers in order to earn that specified rate of return. The usual way that a company will grow its rate base is by investing money into upgrading, modernizing, or possibly even expanding its utility-grade infrastructure. Exelon is doing exactly this as the company has unveiled a $29 billion investment plan for the 2022 to 2025 period. This plan will increase the company’s rate base by an estimated $17 billion:

Exelon Corporation

I will admit that it would be nice to get a bit more visibility than this. Some of the company’s peers have already announced their plans for 2026 and 2027. Hopefully, Exelon will provide this information at its next conference call, however, Exelon typically only makes investment plans for three-year periods as opposed to five-year periods like its peers. Thus, it seems unlikely that the company will provide any insight into its 2027 investment plans.

One thing that eagle-eyed readers will likely note is that the company’s rate base is projected to grow by a lesser amount than the money that Exelon is actually spending. This is not unusual as it is partly caused by depreciation. Depreciation is constantly reducing the value of the assets that the company places into service. As a result, something that is placed into service in 2022 will have a lower value in 2025 and thus a lesser impact on the rate base. As a result, the company’s spending needs to be sufficient to both overcome this effect and still grow the rate base. As we can see, it will accomplish this with the plan that has been laid forth. In total, the company’s rate base growth should be sufficient to grow its earnings per share at a 6% to 8% rate over the period. When we combine this with the current 3.25% dividend yield, Exelon should be able to deliver a 9% to 12% average annual total return, which is a bit higher than most utilities. This is something that should prove reasonably attractive to investors.

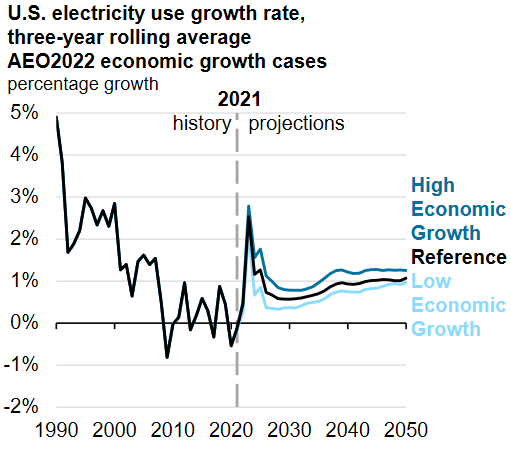

One of the dominant trends that we have been seeing across the utility is a growing commitment to environmental, social, and governance principles. This is particularly prevalent among electric utilities and may be driven by the electrification trend that we have all heard so much about in the media. Unfortunately, full electrification is likely to be a pipe dream, as I have pointed out numerous times. The U.S. Energy Information confirms this in the Annual Energy Outlook 2022, which projects that the national demand for electricity will only increase at a 1% to 2% rate over the next thirty years:

U.S. Energy Information Administration

That is nowhere close to the growth rate that would result if widespread sectors of the economy were to convert from fossil fuels to electricity. Nonetheless, it does make sense for an electric utility like Exelon to conform to environmental, social, and governance principles. After all, there have been a number of thematic funds that have emerged around this concept over the past several years and they have managed to attract an enormous amount of money. As I pointed out in a previous article, American funds had $357 billion and assets and foreign funds controlled a whopping $2.231 trillion at the end of 2021. While figures for year-end 2022 have not been released yet, we can expect that the amounts are higher now. After all, these funds even managed to grow their assets in 2020 even when other funds were suffering massive outflows. That is a sufficiently large quantity of money to affect the stock price of just about any company. I suspect that this is one reason why fossil fuel companies have been trading at incredibly low valuations over the past year since investors in the environmental, social, and governance theme will generally avoid such companies.

As part of a likely effort to attract interest from these thematic investors, Exelon has been touting its environmental credentials. The company currently has the stated objective to cut its own Scope 1 and Scope 2 emissions by 50% by 2025 and achieve net-zero carbon emissions across its business by 2050. This is a similar ambition to what has been stated by most other electric utilities and in fact, it is less aggressive than some of them. After all, there are a few other companies in the industry that are attempting to achieve net-zero emissions by 2040 or even sooner. Exelon has unfortunately not really provided a way to achieve this goal, although it is pursuing efforts to get its customers to use less energy. That is hardly unique in the sector, though. It seems as though the company has a lot of work to do developing its sustainability program, which may explain why the company is somewhat cheaper than its peers. We will discuss this valuation in just a moment. Basically though, as the company continues to develop its plan, it may begin attracting more money from those investors that are interested simply in its environmental or sustainability initiatives, which could prove to have a beneficial impact on the stock price.

Financial Considerations

It is always important that we analyze the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid. This is usually accomplished by issuing new debt to repay the maturing debt as few companies can afford to simply pay off debt with cash as it matures. Thus, a company’s interest expenses may increase following the debt rollover depending on the conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a firm’s cash flows to decline could push it into financial distress if it has too much debt. Although an electric utility like Exelon tends to have remarkably stable cash flows, bankruptcies have occurred in the sector so this is still a risk that we should not ignore.

One metric that we can use to analyze a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well the company’s equity can cover its debt obligations in the event of a liquidation or bankruptcy. This second point is perhaps more important.

As of September 30, 2022, Exelon had a net debt of $38.217 billion compared to $24.582 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.55 today. Here is how that compares to some of Exelon’s peers:

|

Company |

Net Debt-to-Equity |

|

Exelon Corporation |

1.55 |

|

Entergy Corporation (ETR) |

2.14 |

|

DTE Energy (DTE) |

2.22 |

|

FirstEnergy Corporation (FE) |

1.87 |

|

American Electric Power Company (AEP) |

1.54 |

As we can see, Exelon generally compares pretty well to its peers here. The company is generally using less debt to finance its operations than its peers, which is a sign that the company is probably not using too much debt to finance itself. Overall, the risks here should be relatively minimal and investors should not have to worry too much about Exelon’s leverage.

Dividend Analysis

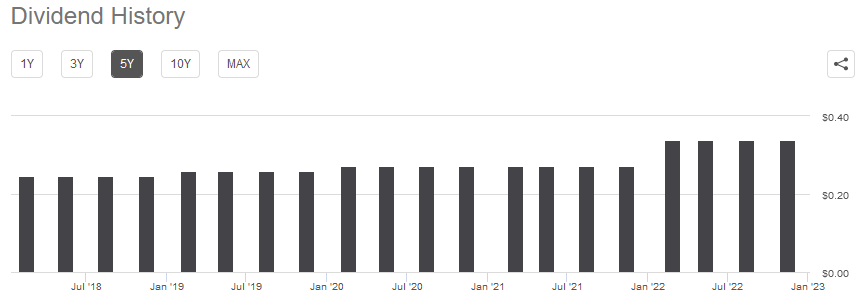

As stated in the introduction, one of the reasons why investors purchase utilities is because of the high dividend yields that they pay out. This is because of their relatively low growth rates, which cause the company to pay out a higher proportion of its cash flows than companies in many other industries. In addition to this, the low growth rates mean that the stock prices of these firms are not going to be affected by multiples as large as companies in other industries. Exelon is certainly no exception to the high yield characteristic as the stock yields 3.25% at the current price. The company also generally increases its dividend annually, although it has not been as reliable as some other utilities in this respect:

Seeking Alpha

With that said though, Exelon has committed to growing its dividend at a 6% to 8% compound annual growth rate going forward. This is something that is quite nice to see, particularly during inflationary times like the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel that we are getting poorer and poorer with the passage of time. The fact that Exelon increases the amount of money that it pays us each year helps to offset this effect and maintains the purchasing power of the dividend that we receive from the company.

Of course, it is still important that we verify the company’s ability to afford the dividend that it pays out. After all, we do not want the company to be forced to reverse course and cut the dividend since that would reduce our incomes and almost certainly cause the company’s stock price to decline.

The usual way that we judge a company’s ability to cover its dividend is by looking at its free cash flow. The free cash flow is the money that is generated by a company’s ordinary operations and is left over after it pays all of its bills and makes any necessary capital expenditures. This is therefore the money that is available to do things that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend. In the twelve-month period that ended September 30, 2022, Exelon reported a negative levered free cash flow of $1.6721 billion. This is obviously not enough to pay any dividend, let alone the $1.375 billion that the company actually paid out in dividends during the period. At first glance, this is likely to be somewhat concerning as it indicates that the company has the insufficient free cash flow to cover its dividend.

However, it is not unusual for a utility to finance its capital expenditures through the issuance of equity and especially debt. The company will then pay its dividend out of operating cash flow. This is due to the high costs of constructing and maintaining utility-grade infrastructure over a wide geographic area. During the twelve-month period that ended September 30, 2022, Exelon had an operating cash flow of $3.012 billion. That was more than sufficient to cover the $1.375 billion that was paid out in dividends with a great deal of money left over for other purposes. Overall, the company’s dividend does appear to be quite sustainable and we do not really need to worry about a cut.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of an electric utility like Exelon, one metric that we can use to value the company is the price-to-earnings growth ratio. This ratio is a modified version of the familiar price-to-earnings ratio that takes a company’s forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be underpriced relative to its earnings per share growth and vice versa. However, there are very few companies that have such a low growth ratio in today’s overheated market. This is especially true in the low-growth utility sector. As such, it makes the most sense to compare Exelon’s valuation to that of its peers in order to determine which stock has the lowest relative valuation.

According to Zacks Investment Research, Exelon will grow its earnings per share at a 6.63% rate over the next three to five years. This is relatively in line with the growth rate that we calculated based on the company’s rate base growth so it seems to be a reasonable estimate. This gives the company a price-to-earnings growth ratio of 2.66 at the current stock price. Here is how that compares to the company’s peers:

|

Company |

PEG Ratio |

|

Exelon Corporation |

2.66 |

|

Entergy Corporation |

2.70 |

|

DTE Energy |

3.03 |

|

FirstEnergy Corporation |

2.62 |

|

American Electric Power Company |

2.84 |

As we can clearly see, Exelon Corporation compares quite well to its peers on this valuation metric. It is admittedly not the cheapest company on the list, but it is pretty close. As we can see above, FirstEnergy, which is the only company here with a lower ratio, has a much higher debt burden and many people could argue that the company has other concerns that reduce its potential as an investment. Thus, Exelon seems to offer a pretty good combination of low risk and an attractive valuation. This is something that is quite nice to see.

Conclusion

In conclusion, Exelon Corporation is a large regulated electric utility that may have a lot of investment potential today. Exelon Corporation boasts very stable cash flows that should position it well to weather any economic trouble that may come in 2023 while still delivering the growth that investors have come to appreciate. The company also boasts a reasonably high and sustainable dividend yield and an attractive valuation. Overall, there is a lot to like here, and Exelon Corporation may be worth considering for investment today.