XPeng (XPEV): Navigating A Rocky Quarter With Potential For A Strong Comeback

SouthWorks

XPeng (NYSE:XPEV) is a top 10 automaker in China, which has recently reported a rough quarter for Q4,22, with both a decline in revenue and deliveries. However, I believe this is a “speed bump” on the road to success as there are a lot of changes happening both outside and inside the company. XPeng has recently (Jan 30th, 2023) had a new President appointed (Ms. Wang) and its vehicle sales for February 2023 increased by 15% over the prior month to 6,225 Smart EVs. China’s GDP is also forecast to increase by 5.2% in 2023, which would be up substantially from 3% in 2022. In addition, the company has new models on the horizon (P7i and G6) and even a “flying car”. In this post, I’m going to break down its financials, before revealing my valuation model and forecasts for XPEV stock; let’s dive in.

Rocky Financials

XPeng reported mixed financial results for the fourth quarter of 2022. Its revenue was $750 million (RMB 5.14B), which represented a decline of 39.9% year over year. This was mainly driven by 46.8% decline in vehicle deliveries to 22,204 from a solid 41,751 in the equivalent quarter of 2021. This vast decline was caused by a variety of factors, including the “hard lockdown” situation across China and internal problems relating to the company. However, I wouldn’t rule out XPeng just yet as if we zoom out, we discover its total vehicle deliveries for 2022 were actually up 23% year over year to 120,757. This makes XPeng the number 10 EV maker in China measured by insurance registrations. Given China is the largest and fastest-growing EV market in the world, there is huge potential still for XPeng, which does have a great product with new models launching.

New Models Launching (P7i and G6)

On March 10th, 2023, XPeng launched the P7i Sports Sedan, which is the upgraded version of its popular P7. Its P7i competes directly with the Tesla Model 3 (TSLA) and actually has a greater range with 436 miles vs 358 miles for Tesla.

I also personally think that P7i is a lot better looking than Tesla with more attractive styling, and I personally like its scissor doors. Of course, styling is subjective, so feel free to comment below your thoughts on the images below. The XPeng P7i is at the top and Tesla Model 3 is at the bottom.

XPeng P7i (XPeng) Tesla model 3 (Tesla)

The P7i also has XPeng’s “most advanced” driving assistance system yet. This includes intercity-assisted driving, lane-centering control, and even valet parking assist. It’s interesting to note that XPeng uses dual-LiDAR units for its assisted driving feature. This is a technology used commonly by other self-driving vehicle companies (Waymo by Google (GOOG, GOOGL) and Mobileye (MBLY)). However, Elon Musk has historically been against LiDAR, he called it a “crutch” and stated anyone relying on it would be “doomed”. But Tesla may now be backtracking to a certain extent, as the company was reportedly using LiDAR to train its camera systems. Either way, I believe LiDAR is a solid technology for self-driving, and although it is more expensive than standard cameras, the prices are likely to fall along with most technology. Therefore, XPeng may be ahead of the curve in this respect as it embraced LiDAR.

The initial order intake for its P7i has been positive with a 100% increase for February (pre-launch), with continued growth expected throughout March and April 2023 (post-launch).

XPeng also has plans to showcase its newest model, the G6, at the Shanghai Auto Show in April 2023 2q1, a formal launch in the second quarter of 2023.

The G6 will be the latest SUV in the market and management expects 2 times to 3 times the monthly sales target of its P7, which would be incredible. This product is also expected to include its state-of-the-art XNGP self-driving vehicle system, which is expected to be the final step before a fully autonomous vehicle. Given the self-driving vehicle market is forecast to be worth close to $98.98 billion by 2023, the company has huge potential in this space.

In an interesting turn of events, XPeng has rebranded itself as a “total mobility” company and recently showcased a “flying car” or EVTOL (electric vertical takeoff and landing vehicle). This was developed with its partner HT Aero and is very similar to vehicles under development by Archer Aviation (ACHR), Joby (JOBY), and EHang (EH). This is another disruptive market, which is forecast to grow at a rapid 23.13% compounded annual growth rate [CAGR], and be worth a solid $23 billion by 2028. In my mind, there are three main barriers to the adoption of the “flying car”, technology, psychology, and regulation. The first point looks to have been achieved by a few companies in the industry such as the aforementioned. However, I forecast regulation will be easier to negotiate in China and the country will be an early adopter. A proof of concept for this is China-based EHang, which has already completed trial flights across cities in China. Therefore, I believe XPeng may benefit from early adoption in this market, which is also an area where Tesla isn’t a competition. In fact, Elon Musk has previously discussed his dismay for EVTOLs in various interviews.

EVTOL XPeng (XPeng)

AI or Artificial Intelligence is also a hot topic recently and XPeng has announced plans to GPT technology (such as those by ChatGPT) in its business to improve efficiency. In fact, XPeng’s self-driving vehicle system called City Navigation Guided Pilot [NGP] uses deep learning algorithms to execute autonomous driving. There has already been footage of this in action on roads across China and according to XPeng’s internal data, its XNGP “outperformed peers” on-road performance even in the U.S.

Margins and Balance Sheet

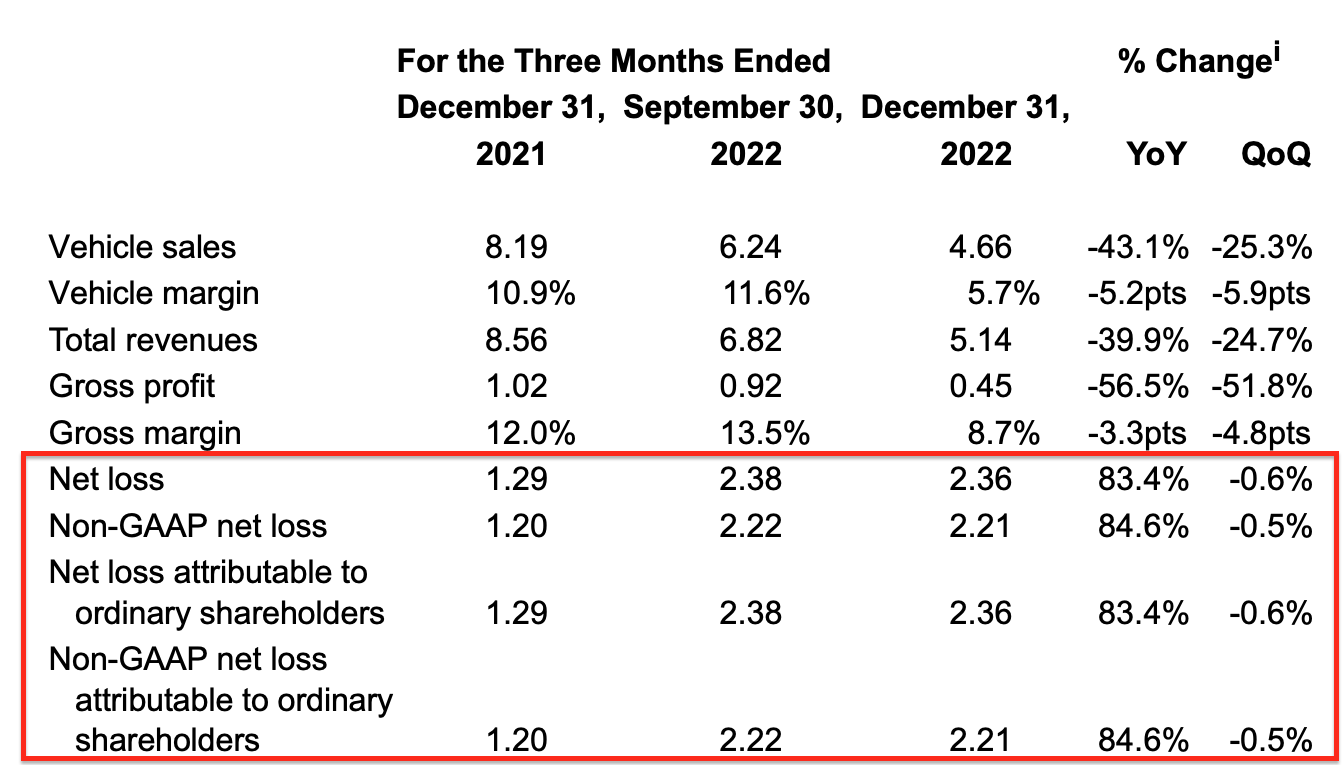

Moving onto margins, the company reported a squeeze of its margins on all its fronts. Its 12% gross margin in 2021 compressed to just 8.7% for Q4,22. In addition, its net loss expanded to $366 million (RMB 2.52B) in Q4,22 from $353 million (RMB 2.43) in Q4,21.

XPeng loss per share in RMB (Q4,22 report)

The only silver lining is its SG&A expenses declined by 12.9% year over year to $250 million (RMB 1.76B). In addition, its Research and Development expenses also declined by ~15.3% year over year to $180 million (RMB 1.23B). Therefore, the main margin impact looks to have been driven by the atrocious top-line sales decline, which has, of course, impacted the company across all aspects of its business.

XPeng also still has a strong balance sheet to weather any storm with cash, cash equivalents, restricted cash, time deposits, and short-term investments of ~$5.55 billion (RMB 38.25b). The company does have ~$1.967 billion in total debt, but a large portion of this ~$1 billion is long-term debt and thus manageable, given the strong cash position.

Valuation and Forecasts

In order to value XPeng, I have plugged its latest financial data into my discounted cash flow valuation model. I have forecast just 10% revenue growth for next year. This is based upon a tough first quarter of 2023, with 18,000 to 19,000 vehicle deliveries expected, followed by an improvement moving forward due to the new model releases. In addition, there are talks that China’s health board plans to recategorize CV19 from a Class A virus to a Class C virus. This is a major deal as it effectively would put the virus in the same category as influenza or the common winter flu. This should be positive for China and consumer demand as a whole. In years 2 to 5, I have forecast a faster growth rate of 20% per year, given the aforementioned tailwinds across China’s EV industry and new model traction. This is fairly conservative in my mind given the company grew its revenue by ~269% between 2020 and 2021.

XPeng stock valuation 1 (Created by author Deep Tech Insights)

To increase the accuracy of my model, I have capitalized R&D expenses, which has boosted net income. I have forecast a pretax operating margin of 13% over the next 5 years. I forecast this to be driven by a series of cost-cutting and efficiency initiatives management aims to put into place between 2023 and 2024. This includes reducing autonomous driving costs by 50% and reducing hardware costs (inc powertrain costs) by 25%. From a manufacturing standpoint, XPeng has finished its investments in its two main manufacturing hubs and thus CapEx is forecast to decline moving forward.

In addition, the company aims to improve its store network efficiency which is expected to deliver material improvements by the second half of 2023. XPeng also aims to split out its sales of hardware and software, which should help enhance margins through upsells.

XPeng stock valuation 2 (created by author Deep Tech Insights)

Given these factors, I get a fair value of $12.51 per share. XPEV stock is trading at $8.84 per share at the time of writing and thus it is ~29.35% undervalued. The stock also trades at a price-to-sales [P/S] ratio = 1.16, which is 82% cheaper than its 5-year average. This is also cheaper than many other competitors in the space, as you can see in the chart below.

Risks

Competition

As you can see in the previous chart above, there is plenty of competition in the EV market. We have extremely large players such as Tesla and BYD (OTCPK:BYDDY), which have both technology and huge scale advantages over the smaller players. Out of the smaller players in China, we have NIO (NIO), Li Auto (LI), and XPeng as well as a few other less well-known players which have popped up. Ultimately, competition tends to cause lower sales and can ultimately “eat” margins if companies compete on price.

Final Thoughts

XPeng has experienced a tough fourth quarter of 2022, but it’s not over for the company just yet. On a full-year basis, its results are still solid and with new models on the horizon coupled with strong growth so far in 2023, a turnaround looks likely. Given my valuation model and forecasts indicate the stock is undervalued intrinsically at the time of writing, I will label XPEV stock as a “hold”, as the company still needs to prove it can bounce back.