Varonis Systems: Cheap Cyber Security Play (NASDAQ:VRNS)

Just_Super

Cyber security software vendor Varonis Systems, Inc. (NASDAQ:VRNS) enjoys a target market growing at a double digit, and many large corporations appreciate its platforms. In my opinion, the SaaS strategy recently implemented may accelerate future sales growth. The target figures reported by VRNS appear quite optimistic, but if the system could achieve scalability, I believe that the guidance could make sense. I also identified several risks from the current dependence on a few vendors and lower growth, however the stock does not seem expensive.

Varonis

Varonis is a pioneer company in the protection and digital security systems and security for data and information. Since its foundation, the company has been oriented towards the development of software that facilitates the routing, monitoring, prevention, and analysis of any disruption in the security of its clients’ digital information infrastructures.

Varonis’ first service back in 2005 was Windows File Transfer Protection. From then until today, the company has managed to develop in line with market and industry trends, offering products and services such as online software services or software that is used for the rapid identification of sensitive material as well as other services related to the security of its clients’ databases. These customers are from a wide variety of different markets and industries, ranging from large corporations with many employees to small start-up organizations that make an early choice to protect their data entry and information systems. Varonis currently operates with clients in more than 90 countries, with its headquarters located in the United States.

Source: Corporate Website

Varonis understands that the data and information trend will continue to grow in the coming years as companies continue to digitize their databases. In the same way, other information and sensitive material monetization strategies are deepened and developed in this regard.

Regarding the SaaS that Varonis offers, it is divided into two product lines, which include Varonis Data Security Platform and DatAdvantage Cloud. Both are online data storage services primarily for the management of the security of the files as well as the general management, administration, and ordering of the same. Varonis also offers, for added fees, the maintenance and renewal of subscriptions to its licenses or technical advice and training for its use.

Sales for Varonis are done through its allied channels and independent vendors who identify potential customers and offer these services through contracts with annual terms between Varonis and the vendors. Contracts can be abandoned by either party with 30 days’ notice.

Products And Analysis Of Data

The number of products offered through the SaaS offering is quite significant, which, in my view, leads to a significant number of interested clients. With that, I believe that what makes the company very different is the ability to follow the activity of millions of users.

Source: Corporate Website

Clients receive a view of the activities of users, which include information about their name, IPs, devices numbers, geographic location, the files they create, and the information they share and download.

Source: Presentation March, 2033

Cybersecurity personnel receive alerts when users download a large amount of information, they share information with other domains, or they use suspicious IPs. They can approve the actions, or flag them, or report the activity.

Source: Presentation March, 2033 Source: Presentation March, 2033

With that, the most interesting thing is coming here. Varonis currently covers Windows (MSFT), Azure, or Azure Active directories. In the last quarterly report, the management announced its intention to attack larger target markets including Azure Blob, GitHub, Google Drive (GOOGL), and Salesforce (CRM). In my view, more applications will likely generate interest from many more clients, which could bring significant FCF in the future.

Source: Presentation March, 2033 Source: Presentation March, 2033

In line with the previous words, improvement of the SaaS model and scalability are expected to multiply future sales growth. The company offered very optimistic numbers in a recent presentation. The targets for 2023 and 2027 seem quite impressive. It is what made me conduct further research about Varonis.

Source: Presentation March, 2033 Source: Presentation March, 2033

Finally, I assumed that the global cyber security market will grow at a double digit as expected by most market experts. In my view, it will be easy for Varonis to report double digit sales growth if the market grows at a similar pace.

The global cyber security market was valued at USD 202.72 billion in 2022 and is projected to expand at a compound annual growth rate of 12.3% from 2023 to 2030. Source: Cyber Security Market Size

As per the report by Fortune Business Insights, the global cyber security market size is projected to reach USD 376.32 billion in 2029, at a CAGR of 13.4% during the forecast period, 2022-2029. Source: Cyber Security Market

Balance Sheet

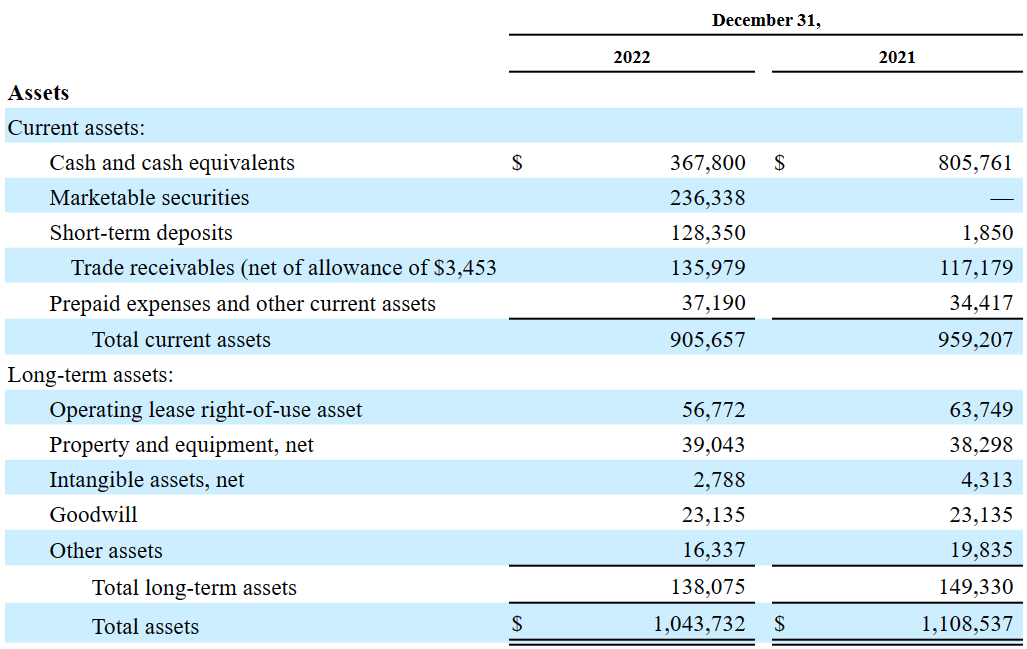

As of December 31, 2022, the company reported cash worth $367 million along with marketable securities of $236 million, short term deposits of $128 million, trade receivables of $135 million, and prepaid expenses and other current assets of $37 million. Finally, total current assets stand at $905 million.

Non-current assets include operating lease rights of use assets of $56 million, property and equipment of $39 million, intangible assets of $2 million, and goodwill worth $23 million. Total long term assets are equal to $138 million, and total assets stand at $1.043 billion. The asset/liability ratio is equal to around 1x. However, the company also reports some long term debt that investors should get to know.

Source: 10-k

With regards to the total amount of liabilities, management reported trade payables of $2 million accompanied by accrued expenses and other short term liabilities of $115 million, deferred revenue close to $110 million, and total current liabilities of $228 million.

Convertible senior notes stand at $248 million along with an operating lease liability of $57 million and deferred revenues of $1 million. Finally, total long-term liabilities are equal to $312 million.

Source: 10-k

90% Renewal Rate, More Innovation, More Classification, And Automatic Remediation

Under my cash flow model, I made several assumptions about the future of the business model. First, I assumed that management would be correct about its forecasts. Innovation and strategic transactions will likely lead to technological capabilities. Besides, new possible commercial relationships with large companies will lead to sales increase, and we will likely see 90% renewal rate based on existing subscriptions like in 2022.

I also assumed that classification and automatic remediation will most likely deepen the connections with other organizations. If Varonis successfully learns what new clients need, and redesigns software of existing clients using the new information about classification, we may even see larger revenue growth than expected.

DCF Model

I assumed 2032 net loss of -$16 million, a depreciation and amortization close to $22 million, and stock based compensation of $508 million. Also, with amortization of deferred commissions of $72 million, I anticipate 2032 non cash operating lease cost of $13 million, 2025 amortization of debt discount of -$3 million, and 2032 trade receivables of -$11 million.

With changes in 2032 other long term assets of -$3 million, changes in trade payables of -$20 million, and accrued expenses of -$138 million, I also assumed changes in 2032 deferred revenues of $288 million. Finally, I obtained CFO of $94 million combined with capex of -$18 million and 2032 FCF of $76 million.

Source: My DCF Model

If we assume an exit multiple of 90x, the 2032 residual value would stand at $6.898 billion. Besides, if we assume a WACC of 8.50%, the sum of future FCF would imply an enterprise value of $3.3 billion. Also, with cash, market securities, and short term deposits of $731 million and debt of $248 million, the expected target price would be close to $31 per share.

Source: My DCF Model

Risks

Varonis also depends on the continued expansion of the digital trend as well as the transformations of data infrastructures to online software systems or information storage in the cloud. Despite having growth results in recent years, Varonis is not in a position to make long-term projections due to its years in the market, youth, and variability of its results. In my view, lower growth will likely lower the expectations for future FCF, which may bring less demand for the stock. As a result, the stock price could decline.

It is also worth noting that Varonis suffers from great dependence on a small number of vendors, the only sales channel. If these vendors decide to renegotiate their terms or work with other competitors, I believe that the company may report sales growth declines.

Although Varonis, according to the company’s analysis, does not have competitors that offer integrated services as it does, it operates in a highly competitive market. In my view, in the future, if a more established company than Varonis tries to enter the market with more resources, years of operations, and development force, it may offer similar products at lower costs. Furthermore, any of the sales agents currently working with Varonis could at any time offer their workforce to new market entrants. As a result, Varonis could lose market share, or may become less competitive, which may lead to lower FCF growth.

My Takeaway

Varonis operates in the global cyber security market, which is expected to grow at a double digit in the coming years. Varonis also appears to offer significant innovative software that large corporations seem to appreciate quite a bit. With large clients, I believe that many other international large groups will be interested in the cyber protection offered by Varonis. Even considering the operating risks from the dependence on a small number of vendors or lower business growth, I believe that the company is not expensive.